Uncategorized

This is a very short blog post. Buttons because I love buttons

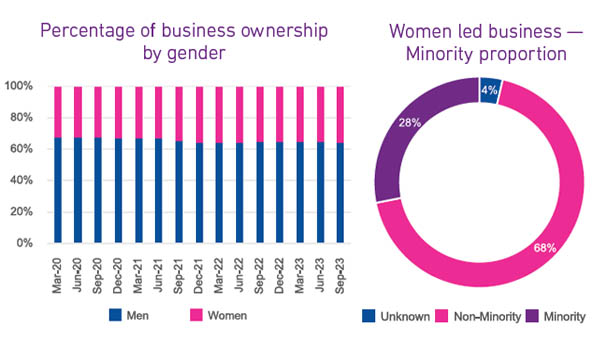

As of recent years, women-owned businesses in the United States have experienced significant growth and have become a substantial force in the economy. It is estimated that there are more than fourteen million women owned business generating over two trillion dollars in annual revenue. The growth in women owned businesses has been fueled by a myriad of reasons, is occurring across all age groups and serves a diverse number of industries. Even with the growth in the number of women owned businesses and the economic impact these business have, women owned businesses are still underserved in the commercial credit markets. Female business owners tend to operate in industries that have a greater need for continuous working capital, thus women owned businesses tend to rely on revolving credit lines. Even with this demand for capital, women business owners are hesitant to apply for financing, and when they do, they are receiving a growing proportion of commercial credit, but the amount of credit granted still trails that of men. The recent growth in women owned businesses could be a driving factor in this disparity. New business have limited to no commercial credit history forcing lenders to evaluate the guarantor’s personal credit. On average, female business owners have a lower consumer credit score, which could be because they are carrying more personal debt to fund their businesses, ultimately decreasing their access to commercial credit. There are a number of factors that when combined, are limiting equal access to commercial credit for female business owners. The good news is that the number of successful women owned businesses continues to climb, and more grants and loans are available to women business owners. What I am watching While inflation in the U.S. is easing, it is still above the Fed’s 2% target. It is widely expected that the Federal Reserve will begin to lower interest rates later this year. It appears that the anticipated recession which led lenders to tighten credit will not occur. Therefore, lenders will likely begin to loosen credit criteria and potentially provide more opportunities for women-owned businesses to obtain the credit they need to operate and expand.

Experian and Oxford Economics Main Street Report for Q3 shows signs of slowdown despite strong Q3 expansion and changing credit conditions.

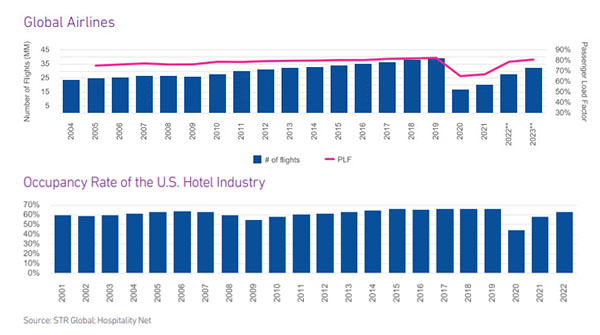

Now that most worldwide travel restrictions have been lifted, the industry is rebounding. It appears that travel businesses relied on more commercial credit to weather the storm of the pandemic and raised prices to help recove

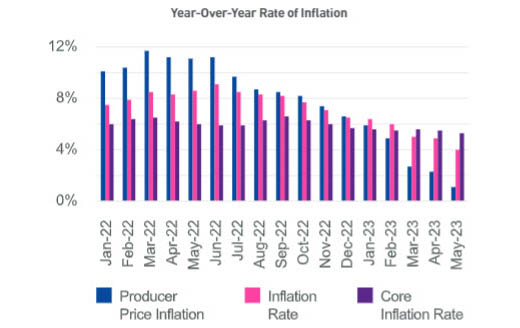

The annual inflation rate continued to decline with May coming in at 4% which was the eleventh consecutive monthly decrease and the lowest level since March 2021. Lower inflation is driven primarily by lower energy costs which decreased 11.7% year over year. Core inflation, which excludes volatile energy and food, slowed to 5.3%. Despite inflation still much higher than the Fed’s 2% target, the Fed paused interest rate hikes after 10 consecutive rate increases in the last 15 months. The Fed indicated that additional hikes may come later this year. New businesses continue to open at a high rate. Despite that these newer, and specifically smaller, businesses are making up a larger and larger portion of commercial credit, they have additional funding needs. According to the Federal Reserve’s 2023 Small Business Credit Survey, almost 70% of businesses with zero employees use personal funding sources for their business while only 27% of them obtain funding from financial institutions or lenders. Since the non-employer businesses reported on 36% had a decline in revenue in 2022 (vs. 38% of employer businesses’ revenue declined in 2022), there is a huge opportunity for financial institutions to tap into this market and support small business growth. What I am watching Small businesses with very few or no employees flourished coming out of the pandemic. It will be interesting to see how many of these micro-businesses will survive the headwinds of inflation, higher interest rates and less access to credit. With an economic slowdown on the horizon, the Fed actions in the coming months will be critical to the outcome. It is yet to be determined if the U.S. economy will achieve the hoped-for soft landing rather than a recession. Download your copy of Experian's Commercial Pulse Report today. Better yet, subscribe so you'll always know when the latest Pulse Report comes out. Subscribe Today

Experian is excited to attend National Equipment Financing Association's 2022 Funding Symposium at the OMNI Nashville, Wednesday, November 2nd through Thursday, November 4th. Dennis Jordahl will be on hand in booth #41 to chat and answer questions about the solutions Experian has to help you grow your business profitably! See you in Nashville! Dennis Jordahl, Account Executive

Gary Stockton: Experian has just released the Q4 2017 Main Street Report. We partner with Moody's Analytics on this report each quarter, and Derrek Grunfelder-McCrank is the economist who works on the report. We asked him a few questions about the trends that we're seeing in this quarter's data. Gary Stockton: The latest Main Street Report states that small business credit conditions remain positive. Is there a primary factor that's driving this stability? Derrek G. McCrank: Yeah there certainly is Gary. The primary factor that's driving stability in small business credit is the broader U.S. economy. Right now we have the labor market that's tight. This is resulting in wage increases for consumers as a result. Consumer spending has been reliable. Inflation is starting to pick up in a slow steady manner. On top of it all at the end of last year we just got tax reform. Right now the outlook for small business credit is positive. And that doesn't look set to change anytime soon. Gary Stockton: and are you seeing greater numbers of small businesses investing in that business by borrowing for equipment purchases? Derrek G. McCrank: Well Gary while we can't say for certain. The data seems to suggest that this isn't happening to the extent it could just yet. One of the questions in the NFIB's monthly survey is about whether firms are planning capital expenditures in the next three to six months. Since the end of the last recession. We've seen the positive response rate to this question steadily increasing. However it still sits below its long term average. Couple this with tax reform coming so late at the end of last year, and a decent number of firms are likely to have waited until the new year when they could invest in their business with a little more certainty. Gary Stockton: Well historically small businesses been keeping bankruptcy in check, but this quarter we saw it up slightly. Is this a major concern? Derrek G. McCrank: This isn't a cause for concern yet. Though it is something to monitor going forward. In the first quarter of 2017 the small business bankruptcy rate bottomed out, it hi its floor. As the year progressed, the bankruptcy rate moved off of that floor and that appears to be all that happened. In fact I'm hopeful that this might indicate a return to a more dynamic environment for small businesses which I look forward to discussing in a little more detail and our upcoming webinar. But for now, given the state of the economy, I'm optimistic for the state of small business credit. Gary Stockton: On the flip side, the Northeast saw a steep decline in business bankruptcies in Q4. Can you share some insight on what might be driving that? Derrek G. McCrank: Sure, so in the fourth quarter. the Northeast saw declines in its severely delinquent or 90 days past due rate coupled with a slight uptick in its business bankruptcy rate. What happened with business bankruptcies mirrored the trend nationally, so it shouldn't be a cause for concern this year, the declines in the severely delinquent rate were driven by two primary factors - geography and industry, from a geographic point of view, Connecticut, New Hampshire and Maine were the driving forces behind the reductions in severe delinquency, and from an industrial point of view financial services, public administration and the manufacturing industries are credited with declines in severe delinquency. Download the latest report