Apply CIS Tag

To combat the threat of synthetic identity fraud, Experian recently announced the launch of Sure Profile a revolutionary change to the credit profile.

The housing sector, in particular, looks poised to regain momentum and perhaps lead the path towards stabilization in the second half of 2020.

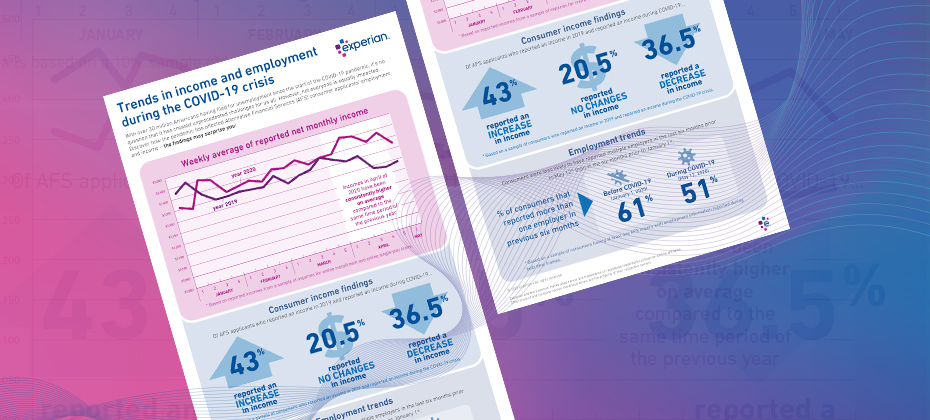

COVID-19 has had far-reaching economic consequences. When it comes to your consumers' finances, are you seeing the full picture?

Experian experts provide insight on how utility providers can evolve amidst COVID-19 and refine their collections and recovery processes.

Many marketing budgets were already small prior to the global pandemic, so coming out of it, to say every marketing dollar counts is an understatement.

While some businesses will look to loss forecasting to potentially reduce the severity of impact from COVID-19, for many, it is the key to survival.

The economic impact of the COVID-19 health crisis is ever-evolving and requires great flexibility and planning from lenders.

Some segments of the financial markets are beginning to bet that the Federal Reserve will take interest rates negative for the first time in U.S. history.

COVID-19 will affect the way financial institutions lend and provide credit. See what Shawn Rife, Experian’s Director of Product Scoring, had to say.

Here's a brief FCRA-related compliance overview to refresh your memory on various FCRA requirements when requesting and using consumer credit reports.

To get a better picture of labor market health in the coming months, there are three components reported in BLS's employment release that require attention.

This week, Experian released a new version of our CrossCore® digital identity and fraud risk platform, adding new tools and functionality.

With a recession on the horizon, economists are using different scenarios to predict economic recovery. Learn more about the 4 potential outcomes.

Credit reporting companies and data furnishers have been put in the spotlight to provide consumers with assistance that they need during COVID-19.

The Federal Open Market Committee closed their latest meeting on April 29 and provided a look into how long rates may remain at their current levels.