All posts by Laura Burrows

Credit reports and conventional credit scores give lenders a strong starting point for evaluating applicants and managing risk. But today's competitive environment often requires deeper insights. Experian develops industry-leading credit attributes and models using traditional methods, as well as the latest techniques in machine learning, advanced analytics and Alternative credit data — or expanded Fair Credit Reporting Act (FCRA)-regulated data)1 to unlock valuable consumer spending and payment information so businesses can drive better outcomes, optimize risk management and better serve consumers READ MORE: What is Alternative Credit Data? Turning credit data into digestible credit attributes Lenders rely on credit attributes — specific characteristics or variables based on the underlying data — to better understand the potentially overwhelming flow of data from traditional and non-traditional sources. However, choosing, testing, monitoring, maintaining and updating attributes can be a time- and resource-intensive process. Experian has over 45 years of experience with data analytics, modeling and helping clients develop and manage credit attributes and risk management. Currently, we offer over 4,500 attributes to lenders, including core attributes and subsets for specific industries. These are continually monitored, and new attributes are released based on consumer trends and regulatory requirements.2 Lenders can use these credit attributes to develop precise and explainable scoring models and strategies. As a result, they can more consistently identify qualified prospects that might otherwise be missed, set initial limits, manage credit lines, improve loyalty by applying appropriate treatments and limit credit losses. Using expanded credit data effectively Leveraging credit attributes is critical for portfolio growth, and businesses can use their expanding access to credit data and insights to improve their credit decisioning. A few examples: Spot trends in consumer behavior: Going beyond a snapshot of a credit report, Trended 3DTM attributes reveal and make it easier to understand customers' behavioral patterns. Use these insights to determine when a customer will likely revolve, transact, transfer a balance or fall into distress. Dig deeper into credit data: Making sense of vast amounts of credit report data can be difficult, but Premier AttributesSM aggregates and summarizes findings. Lenders use the 2,100-plus attributes to segment populations and define policy rules. From prospecting to collections, businesses can save time and make more informed decisions across the customer lifecycle. Get a clear and complete picture: Businesses may be able to more accurately assess and approve applicants, simply by incorporating attributes overlooked by traditional credit bureau reports into their decisioning process. Clear View AttributesTM uses data from the largest alternative financial services specialty bureau, Clarity Services, to show how customers have used non-traditional lenders, including auto title lenders, rent-to-own and small-dollar credit lenders. The additional credit attributes and analysis help lenders make more strategic approval and credit limit decisions, leading to increased customer loyalty, reduced risk and business growth. Additionally, many organizations find that using credit attributes and customized strategies can be important for measuring and reaching financial inclusion goals. About 25 percent of U.S. consumers have a thin credit file (fewer than five credit accounts). And about 19 percent of consumers either don’t have a credit file or don’t have information for conventional scoring models to score them.3 Expanded credit data and attributes can help lenders accurately evaluate many of these consumers and remove barriers that keep them from accessing mainstream financial services. READ MORE: How Expanded FCRA Data Is Revolutionizing the Credit Universe There's no time to wait Businesses can expand their customer base while reducing risk by looking beyond traditional credit bureau data and scores. About 60 percent of U.S. financial institutions are already using or plan to use alternative data, machine learning, AI and advanced analytics in their credit decisioning.3 Download our latest e-book on credit attributes to learn more about what Experian offers and how we can help you stay ahead of the competition. Download e-book Learn more 1When we refer to “Alternative Credit Data," this refers to the use of alternative data and its appropriate use in consumer credit lending decisions, as regulated by the Fair Credit Reporting Act. Hence, the term “Expanded FCRA Data" may also apply in this instance and both can be used interchangeably. 2Experian (May 2021) Experian Credit Attributes. 3Oliver Wyman (12, January 2022) Financial Inclusion and Access to Credit. 4 Forrester (April 2022) Opportunity Snapshot: A Custom Study Commissioned by Experian.

Nearly 28 million American consumers are credit invisible, and another 21 million are unscorable.1 Without a credit report, lenders can’t verify their identity, making it hard for them to obtain mortgages, credit cards and other financial products and services. To top it off, these consumers are sometimes caught in cycles of predatory lending; they have trouble covering emergency expenses, are stuck with higher interest rates and must put down larger deposits. To further our mission of helping consumers gain access to fair and affordable credit, Experian recently launched Experian GOTM, a first-of-its-kind program aimed at helping credit invisibles take charge of their financial health. Supporting the underserved Experian Go makes it easy for credit invisibles and those with limited credit histories to establish, use and grow credit responsibly. After authenticating their identity, users will have their Experian credit report created and will receive educational guidance on improving their financial health, including adding bill payments (phone, utilities and streaming services) through Experian BoostTM. As of January 2022, U.S. consumers have raised their scores by over 87M total points with Boost.2 From there, they’ll receive personalized recommendations and can accept instant card offers. By leveraging Experian Go, disadvantaged consumers can quickly build credit and become scorable. Expanding your lending portfolio So, what does this mean for lenders? With the ability to increase their credit score (and access to financial literacy resources), thin-file consumers can more easily meet lending eligibility requirements. Applicants on the cusp of approval can move to higher score bands and qualify for better loan terms and conditions. The addition of expanded data can help you make a more accurate assessment of marginal consumers whose ability and willingness to pay aren’t wholly recognized by traditional data and scores. With a more holistic customer view, you can gain greater visibility and transparency around inquiry and payment behaviors to mitigate risk and improve profitability. Learn more Download white paper 1Data based on Oliver Wyman analysis using a random sample of consumers with Experian credit bureau records as of September 2020. Consumers are considered ‘credit invisible’ when they have no mainstream credit file at the credit bureaus and ‘unscorable’ when they have partial information in their mainstream credit file, but not enough to generate a conventional credit score. 2https://www.experian.com/consumer-products/score-boost.html

Credit plays a vital role in the lives of consumers and helps them meet important milestones – like getting a car and buying their own home. Unfortunately, not every creditworthy individual has equal access to financial services. In fact, 28 million adult Americans are credit invisible and another 21 million are considered unscorable.1 By leveraging expanded data sources, you can gain a more complete view of creditworthiness, make better decisions and empower consumers to more easily access financial opportunities. The state of credit access Credit is part of your financial power and helps you get the things you need. So, why are certain consumers excluded from the credit economy? There’s a host of reasons. They might have limited or no credit history, have dated or negative information within their credit file or be part of a historically disadvantaged group. For example, almost 30% of consumers in low-income neighborhoods are credit invisible and African and Hispanic Americans are less likely than White Americans to have access to mainstream financial services.2 By gaining further insight into consumer risk, you can facilitate first and second chances for borrowers who are increasingly being shut out of traditional credit offerings. Greater data, greater insights, greater growth Expanding access to credit benefits consumers and lenders alike. With a bigger pool of qualified applicants, you can grow your portfolio and help your community. The trick is doing so while continuing to mitigate risk – enter expanded data. Expanded data includes non-credit payments, demand deposit account (DDA) transactions, professional certifications, and foreign credit history, among other things. Using these data sources can drive greater visibility and transparency around inquiry and payment behaviors, enrich decisions across the entire customer lifecycle and allow lenders to better meet the financial needs of their current and future customers. Read our latest white paper for more insight into the vital role credit plays within our society and how you can increase financial access and opportunities in the communities you serve. Download now 1Data based on Oliver Wyman analysis using a random sample of consumers with Experian credit bureau records as of September 2020. Consumers are considered ‘credit invisible’ when they have no mainstream credit file at the credit bureaus and ‘unscorable’ when they have partial information in their mainstream credit file, but not enough to generate a conventional credit score. 2Credit Invisibles, The CFPB Office of Research, May 2015.

The ongoing COVID-19 pandemic has facilitated an increase in information collection among consumers and organizations, creating a prosperous climate for cybercriminals. As businesses and customers adjust to the “new normal,” hackers are honing in on their targets and finding new, more sophisticated ways to access their sensitive data. As part of our recently launched Q&A perspective series, Michael Bruemmer, Experian’s Vice President of Data Breach Resolution and Consumer Protection, provided insight on emerging fraud schemes related to the COVID-19 vaccines and how increased use of digital home technologies could lead to an upsurge in identity theft and ransomware attacks. Check out what he had to say: Q: How did Experian determine the top data breach trends for 2021? MB: As part of our initiative to help organizations prevent data breaches and protect their information, we release an annual Data Breach Forecast. Prior to the launch of the report, we analyze market and consumer trends. We then come up with a list of potential predictions based off the current climate and opportunities for data breaches that may arise in the coming year. Closer to publication, we pick the top five ‘trends’ and craft our supporting rationale. Q: When it comes to data, what is the most immediate threat to organizations today? MB: Most data breaches that we service have a root cause in employee errors – and working remotely intensifies this issue. Often, it’s through negligence; clicking on a phishing link, reusing a common password for multiple accounts, not using two-factor authentication, etc. Organizations must continue to educate their employees to be more aware of the dangers of an internal breach and the steps they can take to prevent it. Q: How should an organization begin to put together a comprehensive threat and response review? MB: Organizations that excel in cybersecurity often are backed by executives that make comprehensive threats and response reviews a top corporate priority. When the rest of the organization sees higher-ups emphasizing the importance of fraud prevention, it’s easier to invest time and money in threat assessments and data breach preparedness. Q: What fraud schemes should consumers be looking out for? MB: The two top fraud schemes that consumers should be wary of are scams related to the COVID-19 vaccine rollout and home devices being held for ransom. Fraudsters have been leveraging social media to spread harmful false rumors and misinformation about the vaccines, their effectiveness and the distribution process. These mistruths can bring harm to supply chains and delay government response efforts. And while ransomware attacks aren’t new, they are getting smarter and easier with people working, going to school and hosting gatherings entirely on their connected devices. With control over home devices, doors, windows, and security systems, cybercriminals have the potential to hold an entire house hostage in exchange for money or information. For more insight on how to safeguard your organization and consumers from emerging fraud threats, watch our Experian Symposium Series event on-demand and download our 2021 Data Breach Industry Forecast. Watch now Access forecast About Our Expert: Michael Bruemmer, Experian VP of Data Breach Resolution and Consumer Protection, North America Michael manages Experian’s dedicated Data Breach Resolution and Consumer Protection group, which aims to help businesses better prepare for a data breach and mitigate associated consumer risks following breach incidents. With over 25 years in the industry, he has guided organizations of all sizes and sectors through pre-breach response planning and delivery.

The ongoing COVID-19 crisis and the associated rise in online transactions have made it more important than ever to keep customer information accurate and company databases up to date. By ensuring your organization’s data quality, you can allocate resources more effectively, minimize costs and safely serve your customers. As part of our recently launched Q&A perspective series, Suzanne Pomposello, Experian’s Strategic Account Director for CEM vertical markets, and William Palmer, Senior Sales Engineer, provided insight on how utility providers can manage and maintain accurate client data during system migrations and modernizations, achieve a single customer view and implement an operational data quality program. Check out what they had to say: Q: What are the best practices for effective data quality management that utility providers should follow? SP: To ensure data quality, we advise starting with a detailed understanding of the data your organization is currently maintaining and how new data entering your systems is being utilized. Conducting a baseline assessment and being able to properly validate the accuracy of your data is key to identifying areas that require cleansing and enrichment. Once you know what improvements and corrections need to be made, you can establish a strategy that will empower your organization to unlock the full potential of your data. Q: How does Experian help clients improve their data hygiene? SP: Experian has over 30 years of expertise in data cleansing, which is tapped to help clients deploy tactics and strategies to ensure an acceptable level of data integrity. First, we obtain a complete picture of each organizations objectives and challenges. We then assess the quality of their data and identify sources that require remediation. Armed with insight, we work alongside organizations to develop a phased action plan to standardize and enhance their data. Our data management solutions satisfy a wide range of needs and can be consumed in real-time, bulk and batch form. Q: Are there any protection regulations to be aware of when obtaining updated data? WP: Unlike Experian’s regulated divisions, most Experian Data Quality data elements are not burdened by complex regulations and restrictions. Our focus is on organizations’ main customer data points (e.g., address, email address and phone). We reference this data against unregulated source systems to validate, append and complete customer profiles. Experian’s data quality management tools can serve as a foundation for many regulatory, compliance and governance requirements, including, Metro 2 reporting, TCPA and CCPA. Q: Are demos of Experian’s data management solutions available? If so, where can they be accessed? WP: Yes, you can visit our website to view product functionality clips and recorded demonstrations. Additionally, we welcome the opportunity to explore our comprehensive data quality management tools via tests and live demonstrations using actual client data to gain a better understanding of how our solutions can be used to improve operational efficiency and the customer experience. For more insight on how to cleanse, standardize, and enhance your data to make sure you get the most out of your information, watch our Experian Symposium Series event on-demand. Watch now Learn more About Our Experts: Suzanne Pomposello, Strategic Account Director, Experian Data Quality, North America Suzanne manages the energy vertical for Experian’s Data Quality division, supporting North America. She brings innovative solutions to her clients by leveraging technology to deliver accurate and validated contact data that is fit for purpose. William Palmer, Senior Sales Engineer, Experian Data Quality, North America William is a Senior Sales Engineer for Experian’s Data Quality division, supporting North America. As an expert in the data quality space, he advises utility clients on strategies for immediate and long-term data hygiene practices, migrations and reporting accuracy.

New challenges created by the COVID-19 pandemic have made it imperative for utility providers to adapt strategies and processes that preserve positive customer relationships. At the same time, they must ensure proper individualized customer treatment by using industry-specific risk scores and modeled income options at the time of onboarding As part of our ongoing Q&A perspective series, Shawn Rife, Experian’s Director of Risk Scoring, sat down with us to discuss consumer trends and their potential impact on the onboarding process. Q: Several utility providers use credit scoring to identify which customers are required to pay a deposit. How does the credit scoring process work and do traditional credit scores differ from industry-specific scores? The goal for utility providers is to onboard as many consumers as possible without having to obtain security deposits. The use of traditional credit scoring can be key to maximizing consumer opportunities. To that end, credit can be used even for consumers with little or no past-payment history in order to prove their financial ability to take on utility payments. Q: How can the utilities industry use consumer income information to help identify consumers who are eligible for income assistance programs? Typically, income information is used to promote inclusion and maximize onboarding, rather than to decline/exclude consumers. A key use of income data within the utility space is to identify the eligibility for need-based financial aid programs and provide relief to the consumers who need it most. Q: Many utility providers stop the onboarding process and apply a larger deposit when they do not get a “hit” on a certain customer. Is there additional data available to score these “no hit” customers and turn a deposit into an approval? Yes, various additional data sources that can be leveraged to drive first or second chances that would otherwise be unattainable. These sources include, but are not limited to, alternative payment data, full-file public record information and other forms of consumer-permissioned payment data. Q: Have you noticed any employment trends due to the COVID-19 pandemic? How can those be applied at the time of onboarding? According to Experian’s latest State of the Economy Report, the U.S. labor market continues to have a slow recovery amidst the current COVID-19 crisis, with the unemployment rate at 7.9% in September. While the ongoing effects on unemployment are still unknown, there’s a good chance that several job/employment categories will be disproportionately affected long-term, which could have ramifications on employment rates and earnings. To that end, Experian has developed exclusive capabilities to help utility providers identify impacted consumers and target programs aimed at providing financial assistance. Ultimately, the usage of income and employment/unemployment data should increase in the future as it can be highly predictive of a consumer’s ability to pay For more insight on how to enhance your collection processes and capabilities, watch our Experian Symposium Series event on-demand. Watch now Learn more About our Experts: Shawn Rife, Director of Risk Scoring, Experian Consumer Information Services, North America Shawn manages Experian’s credit risk scoring models while empowering clients to maximize the scope and influence of their lending universe. He leads the implementation of alternative credit data within the lending environment, as well as key product implementation initiatives.

Consumer behavior and payment trends are constantly evolving, particularly in a rapidly changing economic environment. Faced with changing demands, including an accelerated shift to digital communications, and new regulatory rules, debt collectors must adapt to advance in the new collections landscape. According to Experian research, as of August, the U.S. unemployment rate was at 8.4%, with numerous states still having employment declines over 10%. These triggers, along with other recent statistics, signal a greater likelihood of consumers falling delinquent on loans and credit card payments. The issue for debt collectors? Many debt collection departments and agencies are not equipped to properly handle the uptick in collection volumes. By refining your process and capabilities to meet today’s demands, you can increase the success rate of your debt collection efforts. Join Denise McKendall, Experian’s Director of Collection Solutions, and Craig Wilson, Senior Director of Decision Analytics, during our live webinar, "Adapting to the New Collections Landscape," on October 21 at 10:00 a.m. PT. Our expert speakers will provide a view of the current collections environment and share insights on how to best adapt. The agenda includes: Meeting today’s collections challenges A Look at the state of the market Devising strategies and solving collections problems across the debt lifecycle Register now

Big data is bringing changes to the way credit scores are reported and making it easier for lenders to find creditworthy consumers, and for consumers to qualify for the financing they need. Since last year’s annual report, alternative credit data1 has continued to gain in popularity. In Experian’s latest 2020 State of Alternative Credit Data report, we take a closer look at why alternative credit data is supplemental and essential to consumer lending and how it’s being adopted by both consumers and financial institutions. While the topic of alternative credit data has become more well known, its capabilities and benefits are still not widely discussed. For instance, did you know that … 89% of lenders agree that alternative credit data allows them to extend credit to more consumers. 96% of lenders agree that in times of economic stress, alternative credit data allows them to more closely evaluate consumer’s creditworthiness and reduce their credit risk exposure. 3 out of 4 consumers believe they are a better borrower than their credit score represents. Not only do consumers believe they’re more financially astute than their credit score depicts – but they’re happy to prove it, with 80% saying they would share various types of financial information with lenders if it meant increased chances for approval or improved interest rates. This year’s report provides a deeper look into lenders’ and consumers’ perceptions of alternative credit data, as well as an overview of the regulatory landscape and how alternative credit data is being used across the lending marketplace. Lenders who incorporate alternative credit data and machine learning techniques into their current processes can harness the data to unlock their portfolio’s growth potential, make smarter lending decisions and mitigate risk. Learn more in the 2020 State of Alternative Credit Data white paper. Download now

New challenges created by the COVID-19 pandemic have made it imperative for utility providers to adapt strategies and processes that preserve positive customer relationships while continuing to collect delinquent balances during an unpredictable and unprecedented time. As part of our ongoing Q&A perspective series, Beth Bayer, Experian’s Vice President of Energy Sales, and Danielle Grigaliunas, Product Manager of Collection Solutions, discuss the changing collections landscape and how the utility industry can best adapt. Check out what they had to say: Q: How are the COVID-19 crisis and today’s economic environment impacting consumer behavior? Particularly as it relates to delinquencies and payments? BB: Typically, when we experience recessions, delinquency goes up. In this recession, delinquency is declining. Stimulus money and increased unemployment benefits, coupled with stay at home orders, appear to be leading to more dollars available for consumers to repay obligations and debts. Another factor is related to special accommodations, forbearances, and payment holidays or extensions, that provide consumers with flexible options in making their regularly scheduled payments. Once an accommodation is granted, the lender or bank puts a code on the account when it’s reported to the bureaus and the account does not continue to age. Q: As a result of the pandemic, many regulatory bodies are recommending or imposing changes to involuntary disconnect policies. How can utility providers effectively collect, even if they can’t disconnect? BB: The public utility commissions in many areas have suspended disconnects due to non-payment, further increasing balances, delinquency and delaying final bill generation. Without the fear of being disconnected for non-payment in some regions of the country, customers are not paying delinquent utility bills. Utility providers should continue to provide payment reminders and delinquency notices and offer payment plans in exchange for partial payments to continue to engage customers. Identifying which customers can pay and are actively paying other creditors and institutions helps prioritize proactive outreach. Q: For utility providers who offer in-house collection services, what strategies and credit data do you find most valuable? DG: Current and accurate data is key when looking to provide stronger and more strategic collections. This data is built into efficient scoring models to articulate which debts are most collectible and how much money will be recovered from each consumer. Without the overlay of credit data, it’s harder for utility providers to predict how consumers prioritize utility debt during times of economic stress. By better understanding the current state of the consumer, utility providers can focus on consumers who are most likely to pay. Investing in monitoring solutions allows utility providers to receive notifications when their consumers are beginning to cure and pay off other obligations and take a more proactive approach. Q: What are the best methods for utility providers to reach collection consumers? What do they need to know as they begin to utilize omnichannel communications? DG: Regular data hygiene checks and skipping are the first line of defense in collections. Confirming contact information is correct and up to date throughout the entire consumer lifecycle helps to establish a strong relationship. Those who are successful in collections invest in omnichannel messaging and self-service payment options, so consumers have a choice on how they’d like to settle their obligations. Q: What current collection trends/challenges are we seeing within the utility space? BB: Utility providers do not traditionally report active customer payments and delinquencies to the credit bureaus. Anecdotally, our utility partners tell us that delinquencies are up and balances are growing. Many customers know that they cannot currently be disconnected if they fall behind on their utility payments and are using this opportunity to prioritize other debts. We also know that some utilities have reduced collection activities during the pandemic due to office closures and have cut back on communication efforts. Additionally, we’re hearing from some of our utility partners that collections and recoveries of final billed or charged-off accounts are increasing, despite many agencies closing and limited to no collection activities occurring. We assume this is because these balances are typically reported to the credit reporting agencies, triggering a payment and interest in clearing that balance first. Constant communication, flexibility, and empathizing with your customers by offering payment plans and accommodations will lead to an increase in dollars collected. DG: There’s been a large misunderstanding that because utility providers can’t disconnect, they can’t attempt to collect. The success of collections has been seen within first parties, as they are still maintaining strong relationships by reaching out at optical times and remaining top-of-mind with consumers. The utility industry needs to take a proactive approach to ensure they are focusing on the right consumers through the right channels at the right time. Credit data that matches the consumer’s credit health (i.e. credit usage and payments) is needed insight when trying to understand a consumer’s overall financial standing. For more insight on how to enhance your collection processes and capabilities, watch our Experian Symposium Series event on-demand. Watch now About our Experts: Beth Bayer, Vice President of Sales, Experian Energy, North America Beth leads the Energy Vertical at Experian, supporting regulated, deregulated and alternative energy companies throughout the United States. She strives to bring innovative solutions to her clients by leveraging technology, data and advanced analytics across the customer lifecycle, from credit risk and identity verification through collections. Danielle Grigaliunas, Product Manager of Collections Solutions, Experian Consumer Information Services, North America Danielle has dedicated her career to the collections space and has spent the last five years with Experian, enhancing and developing collections solutions for various industries and debt stages. Danielle’s focus is ensuring that clients have efficient, compliant and innovative collection and contact strategies.

In today’s uncertain economic environment, the question of how to reduce portfolio volatility while still meeting consumers’ needs is on every lender’s mind. With more than 100 million consumers already restricted by traditional scoring methods used today, lenders need to look beyond traditional credit information to make more informed decisions. By leveraging alternative credit data, you can continue to support your borrowers and expand your lending universe. In our most recent podcast, Experian’s Shawn Rife, Director of Risk Scoring and Alpa Lally, Vice President of Data Business, discuss how to enhance your portfolio analysis after an economic downturn, respond to the changing lending marketplace and drive greater access to credit for financially distressed consumers. Topics discussed, include: Making strategic, data-driven decisions across the credit lifecycle Better managing and responding to portfolio risk Predicting consumer behavior in times of extreme uncertainty Listen in on the discussion to learn more. Experian · Effective Lending in the Age of COVID-19

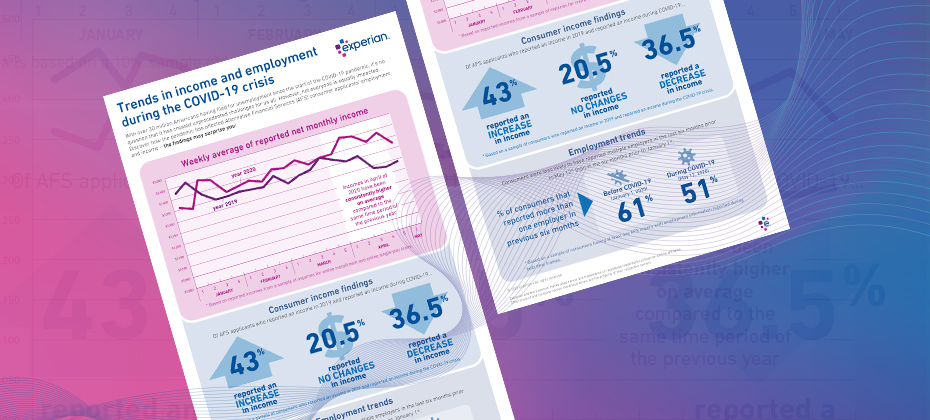

With many individuals finding themselves in increasingly vulnerable positions due to COVID-19, lenders must refine their policies based on their consumers’ current financial situations. Alternative Financial Services (AFS) data helps you gain a more comprehensive view of today's consumer. The COVID-19 pandemic has had far-reaching economic consequences, leading to drastic changes in consumers’ financial habits and behavior. When it comes to your consumers, are you seeing the full picture? See if you qualify for a complimentary hit rate analysis Download AFS Trends Report

The COVID-19 pandemic has created unprecedented challenges for the utilities industry. This includes the need to plan for – and be prepared to respond to – changing behaviors and a sudden uptick in collections activities. As part of our recently launched Q&A perspective series, Mark Soffietti, Experian’s Senior Manager of Analytics Consulting and Tom Hanson, Senior Energy Consultant, provided insight on how utility providers can evolve and refine their collections and recovery processes. Check out what they had to say: Q: How has COVID-19 impacted payment behavior and debt collections? TH: Consumer payment behavior is changing. For example, those who paid as agreed, may not currently have the means to pay and are now distressed borrowers. Or those who were sloppy payers before the pandemic may now be defaulting on a more consistent basis. MS: As we saw with the last recession when faced with economic stress, consumer and commercial payment behavior changes based on their needs and current cash flow. For example, people prioritize their car, as they need it to get to and from work, so they’ll likely pay their auto bills on time. The same goes for their credit cards, which they need to make ends meet. We expect this will also be true with COVID-19. The commercial segment will face more dramatic and challenging circumstances, where complete or partial business closures and lack of federal relief could have severe ramifications. Q: What new restrictions have been put in place surrounding debt collection efforts and outbound calls? TH: To protect consumers who may be experiencing financial distress, most states have imposed new, stringent restrictions to prevent utilities from engaging in certain collections activities. Utilities are currently not charging any late payment fees and are instead structuring payment plans. Additionally, all outbound collections efforts have been suspended and there is fieldwork being executed of services for both commercial and consumer properties. As of now, consumer and commercial fieldwork will likely not commence until after the first year or when the winter moratorium concludes. MS: The new restrictions imposed upon collections activities will likely drive consumer payment behavior. If consumers know that their utilities (i.e. energy and water) will not be shut off if they miss a payment, they will make these bills less of a priority. This will dramatically increase the amount owed when these restrictions are lifted next year. Q: Can we predict how the utilities industry will fare post-COVID-19? TH: The volume of accounts in collections and eligible for disconnect will be overwhelming. Many utility providers fear the unpaid balances consumers and commercial entities accumulate will be nearly impossible to fit into a repayment schedule. Both analyzing internal payment segments and overlaying external factors may be the best way to optimize the most critical go-forward plan. MS: The amount of people who fall into collections is going to greatly increase and utility providers need to start planning for it now to weather the storm. They will need to use data, analytics and tools to help them optimize their tasks, so they can be more efficient with their resources. Like many other industries, the utilities sector will look to increasing digitalization of their processes and having less social interaction where possible. This could mean the need and drive for expediting current smart meter programs where possible to enable remote fieldwork to assist in managing this unprecedented level of activity that is sure to overwhelm field operations (where allowed by state regulators). Q: What should utility providers be doing to plan for an uptick in collections activities post-COVID-19? TH: With regulatory mandated suspensions of collections activities for utility providers and self-selected reductions due to stay at home orders and staff protection, the backlog of payments, calls and inquiries once business resumes as normal is set to overwhelm existing capacity. More than ever, self-service options (text/web), Q&A and alternative communication methods will be needed to shepherd consumers through the collections process and minimize the strain on call center agents. Many utility providers are asking for external data points to segment their consumers by industry or by those whose employment would have been adversely impacted by COVID-19. MS: Utility providers should be monitoring consumer data in order to prepare for when they are able to collect. This will help them strategize the number of resources they will need in their call centers and out in the field performing shut off activities. Given that the rise in cases will be more volume than their call centers can handle, they will need to use their resources wisely and plan to use them efficiently when they are able to resume collections. Q: How can Experian help utility providers reduce collections costs and maximize recovery? TH: Experian can help revise collections tactics and segmentation strategies by providing insight on how consumers are paying other creditors and identifying new segmentation opportunities as we emerge from the freeze on collections activities. Collections cases will be complex, and many factors and constraints will need to balanced against changing goals, making optimization key. MS: Utilizing Experian’s credit data and models can help ensure that resources are being used efficiently (i.e. making successful calls). There is also a need to leverage ability to pay models as well as prioritization models. By using these models and tools, utility providers can optimize their treatment strategies, reduce costs and maximize dollars collected. Learn more About our Experts: Tom Hanson, Senior Energy Consultant, Experian CEM, North America Tom is a Senior Consultant within the Energy Vertical at Experian, supporting regulated energy companies throughout the U.S. He brings over 25 years of experience in the energy field and supports his clients throughout the customer lifecycle, providing expertise in ID verification, account treatment, fraud solutions, analytics, consulting and final bill/field optimization strategies and techniques. Mark Soffietti, Analytics Consulting Senior Manager, Experian Decision Analytics, North America Mark has over 15 years of experience transforming data into actionable knowledge for effective decision management. Mark’s expertise includes solution development for consumer and commercial lending across the credit spectrum – from marketing to collections.

When running a credit report on a new applicant, you must ensure Fair Credit Reporting Act (FCRA) compliance before accessing, using and sharing the collected data. The Coronavirus Aid, Relief, and Economic Security (CARES) Act has impacted credit reporting under the FCRA, as has new guidance from the Consumer Financial Protection Bureau (CFPB). Recent updates include: The CARES Act amended the FCRA to require furnishers who agree to an “accommodation,”1 to report the account as current, although it is permitted to continue to report the account as delinquent if the account was delinquent before the accommodation was made. Although not legally obligated, data furnishers should continue furnishing information to the credit reporting agencies (CRAs) during the COVID-19 crisis, and make sure that information reported is complete and accurate. Below is a brief FCRA-related compliance overview2 covering various FCRA requirements3 when requesting and using consumer credit reports for an extension of credit permissible purpose. For more information regarding your responsibilities under the FCRA as a user of consumer reports, please consult your Legal Counsel and the Notice to Users of Consumer Reports: Obligations of Users Under the FCRA handbook located on our website. Before obtaining a consumer report you have… Reviewed your federal and state regulations and laws related to consumer reports, scores, decisions, etc. Made sure you have a valid permissible purpose for pulling the consumer report. Certified compliance to the CRA from which you are getting the consumer report. You have certified that you complied with all the federal and state requirements. After you take an adverse action based on a consumer report you… Provide the consumer with an oral, written or electronic notice of the adverse action. Provide written or electronic disclosure of the numerical credit score used to take the adverse action, or when providing a “risk-based pricing” notice. Provide the consumer with an oral, written or electronic notice, which includes the below information: Name, address and telephone number of CRA that supplied the report, if nationwide. A statement that the CRA did not make the adverse decision and therefore can’t explain why the decision was made. Notice of the consumer’s right to a free copy of their report from the CRA, if requested within 60 days. Notice of the consumer’s right to dispute with the CRA the accuracy or completeness of any information in a consumer report provided by the CRA. Provide the consumer with a “risk-based pricing” notice if credit was granted but on less favorable terms based on information in their consumer report. We understand how challenging it is to understand and meet all your obligations as a data furnisher – we’re here to make it a little easier. Click below to speak with a representative and gain more insight on how the CARES Act impacts FCRA reporting. Download overview Speak with a representative 1An “accommodation” is defined as “an agreement to defer one or more payments, make a partial payment, forbear any delinquent amounts, modify a loan or contract, or any other assistance or relief” granted to a consumer affected by COVID-19 during the covered period. 2This FCRA overview is not legal guidance and does not enumerate all your requirements under the FCRA as a user of consumer reports. Additionally, this FCRA Overview is not intended to provide legal advice or counsel you regarding your obligations under the FCRA or any other federal or state law or regulation. Should you have any questions about your institution’s specific obligations under the FCRA or any other federal or state law or regulation, you should consult with your Legal Counsel. 3This FCRA overview is intended to be used solely by financial service providers when extending credit to consumers and does not include all FCRA regulatory obligations. You are responsible for regulatory compliance when requesting and using consumer reports, which includes adhering to all applicable federal and state statutes and regulations and ensuring that you have the correct policies and procedures in place.

Today’s lending market has seen a significant increase in alternative business lending, with companies utilizing new data assets and technology. As the lending landscape becomes increasingly competitive, consumers have more choices than ever when it comes to lending products. To drive profitable growth, lenders must find new ways to help applicants gain access to the loans they need. How Spring EQ is leveraging Experian BoostTM Home equity lender Spring EQ turned to Experian’s first-of-its-kind financial tool that empowers consumers to add positive payments directly into their credit file to assist applicants with attaining the best loan opportunities and rates. By using Experian BoostTM, which captures the value of consumer’s utility and telecom trade lines, in their current lending process, Spring EQ can help applicants near approval or risk thresholds move to higher risk tiers and qualify for better loan terms and conditions. Driving growth with consumer-permissioned data Over 40 million consumers in the U.S. either have no credit file or have insufficient information in their files to generate a traditional credit score. Consumer-permissioned data empowers these individuals to leverage their online financial data and payment histories to gain better access to loans and other financial services while providing lenders with a more comprehensive view of their creditworthiness. According to Experian research, 70% of consumers see the benefits of sharing additional financial information and contributing positive payment history to their credit file if it increases their odds of approval and helps them access more favorable credit terms. Read our case study for more insight on using Experian Boost to: Make better lending decisions Offer or underwrite credit to more people Promote the right credit products Increase conversion and utilization rates Read case study Learn more about Experian Boost

The coronavirus (COVID-19) outbreak is causing widespread concern and economic hardship for consumers and businesses across the globe – including financial institutions, who have had to refine their lending and downturn response strategies while keeping up with compliance regulations and market changes. As part of our recently launched Q&A perspective series, Shannon Lois, Experian’s Head of DA Analytics and Consulting and Bryan Collins, Senior Product Manager, tackled some of the tough questions for lenders. Here’s what they had to say: Q: What trends and triggers should lenders be prepared to react to? BC: Lenders are still trying to figure out how to assess risk between the broader, longer-term impacts of the pandemic and the near-term Coronavirus Aid, Relief, and Economic Security (CARES) Act that extends relief funds and deferment to consumers and small businesses. Traditional lending processes are not possible, lenders will have to adjust underwriting strategies and workflows as they deploy hardship programs while complying with the Act. From a utilization perspective, lenders need to look for near-term trends on payments, balances and skipped payments. From an extension standpoint, they should review limits extended or reduced by other lenders. Critical trends to look for would be missed or late auto payments, non-traditional credit shopping and rental payment delinquencies. Q: What should lenders be doing to plan for an uptick in delinquencies? SL: First, lenders should make sure they have a complete picture of how credit risk and losses are evolving, as well as any changes to their consumers’ affordability status. This will allow a pointed refinement of their customer management strategies (I.e. payment holidays, changing customer to cheaper product, offering additional services, re-pricing, term amendment and forbearance management.) Second, given the increased stress on collection processes and regulations guidelines, they should ensure proper and prepared staffing to handle increased call volumes and that agency outsourcing and automation is enabled. Additionally, lenders should migrate to self-service and interactive communication channels whenever possible while adopting new segmentation schemas/scores/attributes based on fresh data triggers to queue lower risk accounts entering collections. Q: How can lenders best help their customers? SL: Lenders should understand customers’ profiles with vulnerability and affordability metrics allowing changes in both treatment and payment. Payment Holidays are common in credit card management, consider offering payment freezes on different types of credit like mortgage and secured loans, as well as short term workout programs with lower interest rates and fee suppression. Additionally, lenders should offer self-service and FAQ portals with information about programs that can help customers in times of need. BC: Lenders can help by complying with aspects of the CARES Act guidance; they must understand how to deploy payment relief and hardship programs effectively and efficiently. Data integrity and accuracy of loan reporting will be critical. Financial institutions should adjust their collection and risk strategies and processes. Additionally, lenders must determine a way to address the unbanked population with relief checks. We understand how challenging it is to navigate the changing economic tides and will continue to offer support to both businesses and consumers alike. Our advanced data and analytics can help you refine your lending processes and better understand regulatory changes. Learn more About Our Experts: Shannon Lois, Head of DA Analytics and Consulting, Experian Data Analytics, North America Shannon and her team of analysts, scientists, credit, fraud and marketing risk management experts provide results-driven consulting services and state-of-the-art advanced analytics, science and data products to clients in a wide range of businesses, including banking, auto, credit, utility, marketing and finance. Shannon has been a presenter at many credit scoring and risk management conferences and is currently leading the Experian Decision Analytics advisory board. Bryan Collins, Senior Product Manager, Experian Consumer Information Services, North America Bryan is a member of Experian's CIS product management team, focusing on the Acquisitions suite and our evolving Ascend Identity Services Platform. With more than 20 years of experience in the financial services and credit industries, Bryan has established strong partnerships and a thorough understanding of client needs. He was instrumental in the launch of CIS's segmentation suite and led product management for lender and credit-related initiatives in Auto. Prior to joining Experian, Bryan held marketing and consumer experience roles in consumer finance, business lending and card services.