All posts by Stefani Wendel

In today’s evolving and competitive market, the stakes are high to deliver both quantity and quality. That is, to deliver growth goals while increasing customer satisfaction. OneAZ Credit Union is the second largest credit union in Arizona, serving over 157,000 members across 21 branches. Wanting to fund more loans faster and offer a better member experience through their existing loan origination system (LOS), OneAZ looked to improve their decisioning system and long-standing underwriting criteria. They partnered with Experian to create an automated underwriting strategy to meet their aggressive approval rate and loss rate goals. By implementing an integrated decisioning system, OneAZ had flexible access to data credit attributes and scores, resulting in increased automation through their existing LOS – meaning they didn’t have to completely overhaul their decisioning systems. Additionally, they leveraged software that enabled champion/challenger strategies and the flexibility to manage their decision criteria. Within one month of implementation, OneAZ saw a 26% increase in loan funding rates and a 25% decrease in manual reviews. They can now pivot quickly to respond to continuously evolving conditions. “The speed at which we can return a decision and our better understanding of future performance has really propelled us in being able to better serve our members,” said John Schooner, VP Credit Risk Management at OneAZ. Read our case study for more insight on how automation and PowerCurve Originations Essentials can move the needle for your organization, including: Streamlined strategy development and execution to minimize costly customizations and coding Comprehensive data assets across multiple sources to ensure ID verification and a holistic view of your prospect Proactive monitoring and real-time visibility to challenge and rapidly adjust strategies as needed Download the full case study

Whether looking to increase resources or focus on artificial intelligence and machine learning, growth is the name of the game.

Consumers continue to manage credit well and the average credit score climbed seven points since 2020 to 695, the highest point in more than 13 years.

As financial institutions navigate COVID-19’s economic impact, the best credit portfolio management practices are fundamental.

Last year’s predictions of a new set of Roaring 20’s may not have panned out the way we imagine, but many did evolve. Here are six trends to watch in 2021.

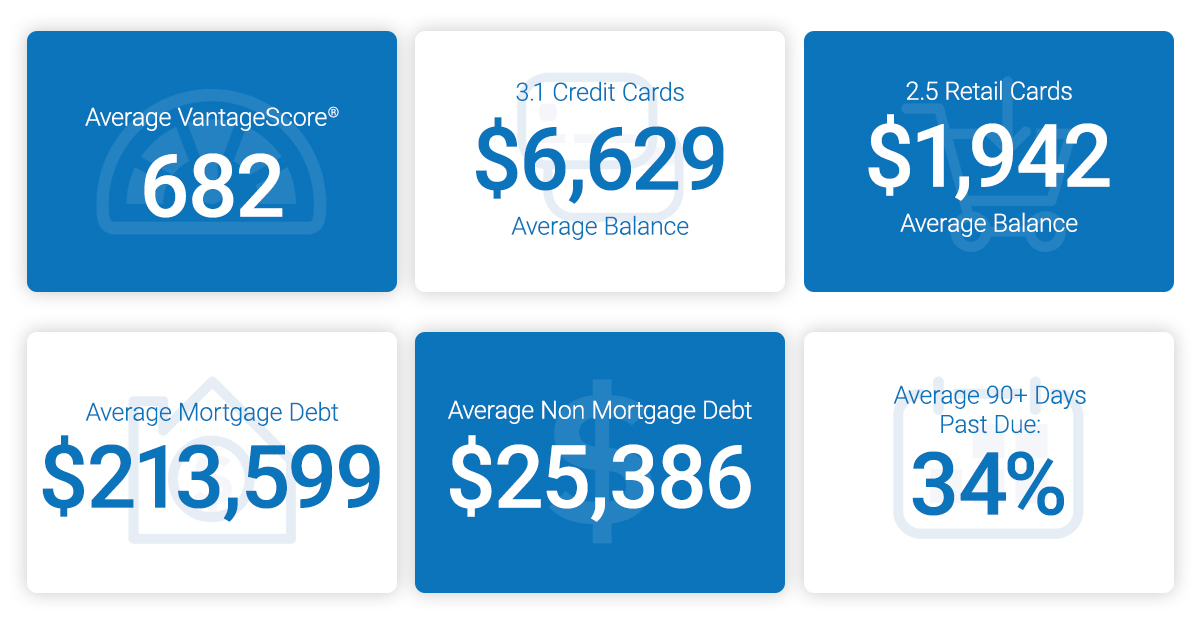

Experian released the 11th annual state of credit report, which provides a comprehensive look at the credit performance of consumers across America.

Account management is a critical strategy during any type of economy (pro-cycle, counter-cycle, cycle neutral), but especially now.

We’ve entered a new era of loss forecasting. Previously built models are no longer sufficient for the changes in economic conditions due to COVID-19.

Many marketing budgets were already small prior to the global pandemic, so coming out of it, to say every marketing dollar counts is an understatement.

While some businesses will look to loss forecasting to potentially reduce the severity of impact from COVID-19, for many, it is the key to survival.

If you're looking for a competitive edge in 2020, Vision is your ticket into differentiating your organization with the latest insights and innovation.

Exploring some of the top trends for the financial services industry going into the new decade from data and decisioning to fraud and customer experience.

As look forward to the next decade, things are looking up. The 10th annual State of Credit Report highlights consumer credit scores and borrowing behavior.

Experian and Oliver Wyman have joined forces to launch Ascend CECL Forecaster to help financial institutions of all sizes forecast lifetime credit losses.

The next recession is a matter of when, not if. As the economy shifts, so will the priorities for your portfolio, so now is the time to strategize.