Financial Services

Time – it’s the only resource we can’t get more of, which is why we tend to obsess over saving it. Despite this obsession, it can be hard for us to identify time-wasting activities. From morning habits to credit decisioning, processes and routines that seem, well, routine, can get in the way of maximizing how we use our time. Identifying the Problem Every morning, I used to turn on my coffee maker, walk to the bathroom to take my multivitamin, then walk back into the kitchen to finish making my coffee. This required maybe twenty steps to the bathroom and twenty steps back, and while this isn’t a huge amount of time—half a minute at best—it’s not insignificant, especially in the morning when time feels particularly precious. One day, I realized I could eliminate the waste by moving my multivitamin to the cabinet above my coffeemaker. What if we could all make minor changes to enhance our efficiency both at home and at work? Imagine how much time we could save by cutting out unnecessary steps. And how saving that time could help drive significant revenue increases. Time Equals Money When businesses waste time with unnecessary steps, that’s money from their bottom line, and out of the pockets of people who are connected to them. Over the last several years, a new time saver has emerged – Application Programming Interface (API). APIs allow application programs to communicate with other operating systems or control programs through a series of server requests or API calls, enabling seamless interaction, data sharing and decisioning. Experian’s partners utilize our ever-growing suite of APIs to quickly access better data, making existing processes more effective and routines more efficient. In the past, banks and other partners had to send files back and forth to Experian when they needed decisioning on a customer’s credit-worthiness prior to approving a new loan or extending a credit limit increase. Now, partners can have their origination system call an Experian API and send their data through that. Our system processes it and sends it back in milliseconds, giving the lenders real-time decisioning rather than shuttling information back and forth unnecessarily. Instead of effectively walking away from one process (assisting the customer/making coffee) to start another (retrieving credit info/walking down the hall to take the multivitamin), our partners are able to link these processes up and save time, allowing them to capitalize on the presence and interest of their customer. The Proof When Washington State Employees Credit Union, the second-largest credit union in the state, realized they needed to make a change to keep pace with increasing competition, they turned to Experian. With our solution, the credit union is now able to provide its members with instant credit decisioning through their online banking platform. This real-time decisioning at the point of member-initiated contact increased the credit union’s loan and credit applications by 25%. Additionally, member satisfaction increased, with 90% of members finding the simplified prequalification process to be more efficient. By accessing Experian’s decisioning services through your existing connection, lenders can to save time and match consumers with the products that match their credit profile before they apply – increasing approval rates once the application is submitted. Best of all, the entire process with the consumers is completed within seconds. Find out how Experian’s solutions can help you improve your existing processes and cut out unnecessary steps. Get started

Fintech is quickly changing. The word itself is synonymous with constant innovation, agile technology structures and being on the cusp of the future of finance. The rapid rate at which fintech challengers are becoming established, is in turn, allowing for greater consumer awareness and adoption of fintech platforms. It would be easy to assume that fintech adoption is predominately driven by millennials. However, according to a recent market trend analysis by Experian, adoption is happening across multiple generational segments. That said, it’s important to note the generational segments that represent the largest adoption rates and growth opportunities for fintechs. Here are a few key stats: Members of Gen Y (between 24-37 years old) account for 34.9% of all fintech personal loans, compared to just 24.9% for traditional financial institutions. A similar trend is seen for Gen Z (between 18-23 years old). This group accounts for 5% of all fintech personal loans as compared to 3.1% for traditional Let’s take a closer look at these generational segments… Gen Y represents approximately 19% of the U.S. population. These consumers, often referred to as “millennials,” can be described as digital-centric, raised on the web and luxury shoppers. In total, millennials spend about $600 billion a year. This group has shown a strong desire to improve their credit standing and are continuously increasing their credit utilization. Gen Z represents approximately 26% of the U.S. population. These consumers can be described as digital centric, raised on the social web and frugal. The Gen Z credit universe is growing, presenting a large opportunity to lenders, as the youngest Gen Zers become credit eligible and the oldest start to enter homeownership. What about the underbanked as a fintech opportunity? The CFPB estimates that up to 45 million people, or 24.2 million households, are “thin-filed” or underbanked, meaning they manage their finances through cash transactions and not through financial services such as checking and savings accounts, credit cards or loans. According to Angela Strange, a general partner at Andreessen Horowitz, traditional financial institutions have done a poor job at serving underbanked consumers affordable products. This has, in turn, created a trillion-dollar market opportunity for fintechs offering low-cost, high-tech financial services. Why does all this matter? Fintechs have a unique opportunity to engage, nurture and grow these market segments early on. As the fintech marketplace heats up and the overall economy begins to soften, diversifying revenue streams, building loyalty and tapping into new markets is a strategic move. But what are the best practices for fintechs looking to build trust, engage and retain these unique consumer groups? Join us for a live webinar on November 12 at 10:00 a.m. PST to hear Experian experts discuss financial inclusion trends shaping the fintech industry and tactical tips to create, convert and extend the value of your ideal customers. Register now

Retailers are already starting to display their Christmas decorations in stores and it’s only early November. Some might think they are putting the cart ahead of the horse, but as I see this happening, I’m reminded of the quote by the New York Yankee’s Yogi Berra who famously said, “It gets late early out there.” It may never be too early to get ready for the next big thing, especially when what’s coming might set the course for years to come. As 2019 comes to an end and we prepare for the excitement and challenges of a new decade, the same can be true for all of us working in the lending and credit space, especially when it comes to how we will approach the use of alternative data in the next decade. Over the last year, alternative data has been a hot topic of discussion. If you typed “alternative data and credit” into a Google search today, you would get more than 200 million results. That’s a lot of conversations, but while nearly everyone seems to be talking about alternative data, we may not have a clear view of how alternative data will be used in the credit economy. How we approach the use of alternative data in the coming decade is going to be one of the most important decisions the lending industry makes. Inaction is not an option, and the time for testing new approaches is starting to run out – as Yogi said, it’s getting late early. And here’s why: millennials. We already know that millennials tend to make up a significant percentage of consumers with so-called “thin-file” credit reports. They “grew up” during the Great Recession and that has had a profound impact on their financial behavior. Unlike their parents, they tend to have only one or two credit cards, they keep a majority of their savings in cash and, in general, they distrust financial institutions. However, they currently account for more than 21 percent of discretionary spend in the U.S. economy, and that percentage is going to expand exponentially in the coming decade. The recession fundamentally changed how lending happens, resulting in more regulation and a snowball effect of other economic challenges. As a result, millennials must work harder to catch up financially and are putting off major life milestones that past generations have historically done earlier in life, such as homeownership. They more often choose to rent and, while they pay their bills, rent and other factors such as utility and phone bill payments are traditionally not calculated in credit scores, ultimately leaving this generation thin-filed or worse, credit invisible. This is not a sustainable scenario as we enter the next decade. One of the biggest market dynamics we can expect to see over the next decade is consumer control. Consumers, especially millennials, want to be in the driver’s seat of their “credit journey” and play an active role in improving their financial situations. We are seeing a greater openness to providing data, which in turn enables lenders to make more informed decisions. This change is disrupting the status quo and bringing new, innovative solutions to the table. At Experian, we have been testing how advanced analytics and machine learning can help accelerate the use of alternative data in credit and lending decisions. And we continue to work to make the process of analyzing this data as simple as possible, making it available to all lenders in all verticals. To help credit invisible and thin-file consumers gain access to fair and affordable credit, we’ve recently announced Experian Lift, a new suite of credit score products that combines exclusive traditional credit, alternative credit and trended data assets to create a more holistic picture of consumer creditworthiness that will be available to lenders in early 2020. This new Experian credit score may improve access to credit for more than 40 million credit invisibles. There are more than 100 million consumers who are restricted by the traditional scoring methods used today. Experian Lift is another step in our commitment to helping improve financial health of consumers everywhere and empowers lenders to identify consumers who may otherwise be excluded from the traditional credit ecosystem. This isn’t just a trend in the United States. Brazil is using positive data to help drive financial inclusion, as are others around the world. As I said, it’s getting late early. Things are moving fast. Already we are seeing technology companies playing a bigger role in the push for alternative data – often powered by fintech startups. At the same time, there also has been a strong uptick in tech companies entering the banking space. Have you signed up for your Apple credit card yet? It will take all of 15 seconds to apply, and that’s expected to continue over the next decade. All of this is changing how the lending and credit industry must approach decision making, while also creating real-time frictionless experiences that empower the consumer. We saw this with the launch of Experian Boost earlier this year. The results speak for themselves: hundreds of thousands of previously thin-file consumers have seen their credit scores instantly increase. We have also empowered millions of consumers to get more control of their credit by using Experian Boost to contribute new, positive phone, cable and utility payment histories. Through Experian Boost, we’re empowering consumers to play an active role in building their credit histories. And, with Experian Lift, we’re empowering lenders to identify consumers who may otherwise be excluded from the traditional credit ecosystem. That’s game-changing. Disruptions like Experian Boost and newly announced Experian Lift are going to define the coming decade in credit and lending. Our industry needs to be ready because while it may seem early, it’s getting late.

It seems like artificial intelligence (AI) has been scaring the general public for years – think Terminator and SkyNet. It’s been a topic that’s all the more confounding and downright worrisome to financial institutions. But for the 30% of financial institutions that have successfully deployed AI into their operations, according to Deloitte, the results have been anything but intimidating. Not only are they seeing improved performance but also a more enhanced, positive customer experience and ultimately strong financial returns. For the 70% of financial institutions who haven’t started, are just beginning their journey or are in the middle of implementing AI into their operations, the task can be daunting. AI, machine learning, deep learning, neural networks—what do they all mean? How do they apply to you and how can they be useful to your business? It’s important to demystify the technology and explain how it can present opportunities to the financial industry as a whole. While AI seems to have only crept into mainstream culture and business vernacular in the last decade, it was first coined by John McCarthy in 1956. A researcher at Dartmouth, McCarthy thought that any aspect of learning or intelligence could be taught to a machine. Broadly, AI can be defined as a machine’s ability to perform cognitive functions we associate with humans, i.e. interacting with an environment, perceiving, learning and solving problems. Machine learning vs. AI Machine learning is not the same thing as AI. Machine learning is the application of systems or algorithms to AI to complete various tasks or solve problems. Machine learning algorithms can process data inputs and new experiences to detect patterns and learn how to make the best predictions and recommendations based on that learning, without explicit programming or directives. Moreover, the algorithms can take that learning and adapt and evolve responses and recommendations based on new inputs to improve performance over time. These algorithms provide organizations with a more efficient path to leveraging advanced analytics. Descriptive, predictive, and prescriptive analytics vary in complexity, sophistication, and their resulting capability. In simplistic terms, descriptive algorithms describe what happened, predictive algorithms anticipate what will happen, and prescriptive algorithms can provide recommendations on what to do based on set goals. The last two are the focus of machine learning initiatives used today. Machine learning components - supervised, unsupervised and reinforcement learning Machine learning can be broken down further into three main categories, in order of complexity: supervised, unsupervised and reinforcement learning. As the name might suggest, supervised learning involves human interaction, where data is loaded and defined and the relationship to inputs and outputs is defined. The algorithm is trained to find the relationship of the input data to the output variable. Once it delivers accurately, training is complete, and the algorithm is then applied to new data. In financial services, supervised learning algorithms have a litany of uses, from predicting likelihood of loan repayment to detecting customer churn. With unsupervised learning, there is no human engagement or defined output variable. The algorithm takes the input data and structures it by grouping it based on similar characteristics or behaviors, without a defined output variable. Unsupervised learning models (like K-means and hierarchical clustering) can be used to better segment or group customers by common characteristics, i.e. age, annual income or card loyalty program. Reinforcement learning allows the algorithm more autonomy in the environment. The algorithm learns to perform a task, i.e. optimizing a credit portfolio strategy, by trying to maximize available rewards. It makes decisions and receives a reward if those actions bring the machine closer to achieving the total available rewards, i.e. the highest acquisition rate in a customer category. Over time, the algorithm optimizes itself by correcting actions for the best outcomes. Even more sophisticated, deep learning is a category of machine learning that involves much more complex architecture where software-based calculators (called neurons) are layered together in a network, called a neural network. This framework allows for much broader, complex data ingestion where each layer of the neural network can learn progressively more complex elements of the data. Object classification is a classic example, where the machine ‘learns’ what a duck looks like and then is able to automatically identify and group images of ducks. As you might imagine, deep learning models have proved to be much more efficient and accurate at facial and voice recognition than traditional machine learning methods. Whether your financial institution is already seeing the returns for its AI transformation or is one of the 61% of companies investing in this data initiative in 2019, having a clear picture of what is available and how it can impact your business is imperative. How do you see AI and machine learning impacting your customer acquisition, underwriting and overall customer experience?

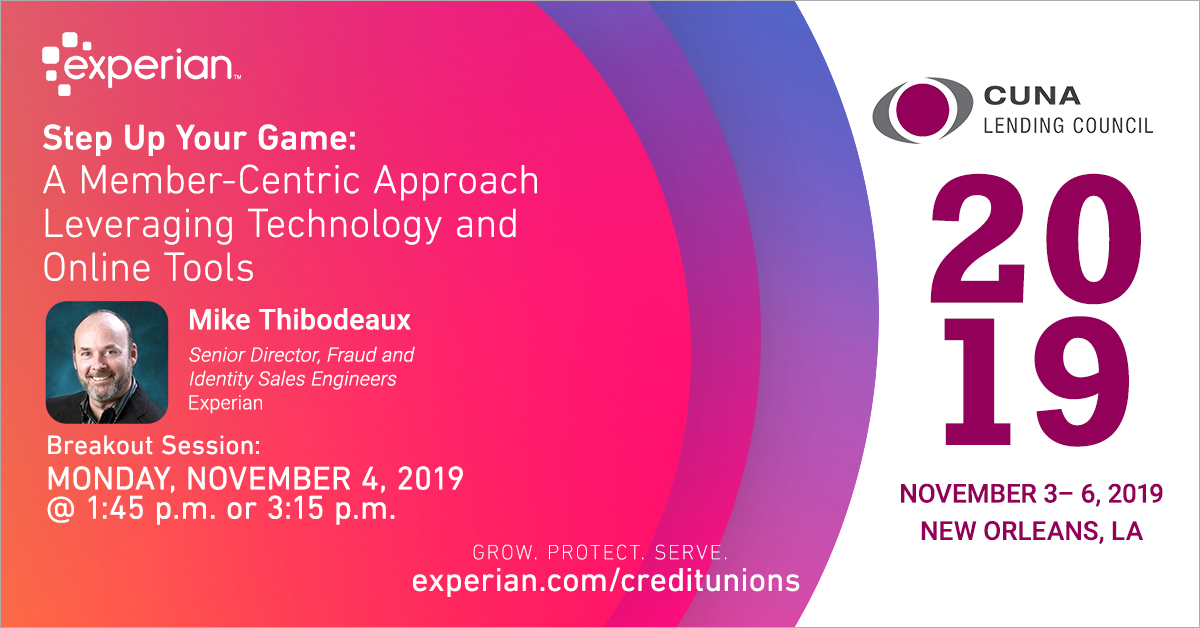

As credit unions look to grow their loan portfolios and acquire new members, improving the member experience is critical to the process and remains a primary focus. In order to compete in the lending universe, financial tools that empower and enable a positive experience are critical to meeting these requirements. That being said, an Experian study reveals that 90% of executives agree that embracing a digital transformation is critical to providing excellent experiences. In this connected, data-driven world, digital transformations are opening the door for better and greater opportunities. With data and analytics, credit unions will be able to gain data-driven insights, to identify key channels of member engagement, create complete member views and further maximize growth and lending strategies. Data-driven organizations that can anticipate their members’ needs and preferences will be able to deepen relationships and maintain relevance – gaining an edge in a highly-competitive environment. The digital revolution is happening now – and it’s time for future-focused credit unions to adapt to changing expectations. However, according to an Experian report, 39% of organizations lack the customer insight and data required to provide these member experiences. That’s where Experian comes in. Join Mike Thibodeaux, Experian’s Senior Director, Fraud and Identity Sales Engineers, for a breakout session at CUNA Lending 2019 on Monday, Nov. 4 at 1:45 p.m. or 3:15 p.m. He will take a closer look at best practices and digital tools that credit unions can use to maximize credit union membership growth, while managing and mitigating fraud. The discussion will revolve around multiple topics, critical to the member experience conversation, including: Increasing profitable loan growth Lending deeper to the underserved Levering digital services and tools for your credit union Minimizing fraud activity (specifically synthetic identity fraud) and credit losses Enhancing and maintaining positive member experiences Experian is excited to once again take part in the 2019 CUNA Lending Council Conference, an event that brings together the credit union movement’s best and brightest in lending. If you’re attending, make sure to engage and connect with our thought leaders at our booth and learn how we’re dedicated to helping credit unions of all sizes advance their decisioning and services. Our team is committed to being a trusted partner – providing solutions that enable you to further grow, protect and serve within your field of membership. Learn More

To provide consumers with clear-cut protections against disturbance by debt collectors, the Consumer Financial Protection Bureau (CFPB) issued a Notice of Proposed Rulemaking (NPRM) to implement the Fair Debt Collection Practices Act (FDCPA) earlier this year. Among many other things, the proposal would set strict limits on the number of calls debt collectors may place to reach consumers weekly and clarify requirements for consumer-facing debt collection disclosures. A bigger discussion Deliberation of the debt collection proposal was originally scheduled to begin on August 18, 2019. However, to allow commenters to further consider the issues raised in the NPRM and gather data, the comment period was extended by 20 days to September 18, 2019. It is currently still being debated, as many argue that the proposed rule does not account for modern consumer preferences and hinders the free flow of information used to help consumers access credit and services. The Association of Credit and Collection Professionals (ACA International) and US House lawmakers continue to challenge the proposal, stating that it doesn’t ensure that debt collectors’ calls to consumers are warranted, nor does it do enough to protect consumers’ privacy. Many consumer advocates have expressed doubts about how effective the proposed measures will be in protecting debtors from debt collector harassment and see the seven-calls-a-week limit on phone contact as being too high. In fact, it’s difficult to find a group of people in full support of the proposal, despite the CFPB stating that it will help clarify the FDCPA, protect lenders from litigation and bring consumer protection regulation into the 21st century. What does this mean? Although we don’t know when, or if, the proposed rule will go into effect, it’s important to prepare. According to the Federal Register, there are key ways that the new regulation would affect debt collection through the use of newer technologies, required disclosures and limited consumer contact. Not only will the proposed rules apply to debt collectors, but its provisions will also impact creditors and servicers, making it imperative for everyone in the financial services space to keep watch on the regulation’s status and carefully analyze its proposed rules. At Experian, our debt collection solutions automate and moderate dialogues and negotiations between consumers and collectors, making it easier for collection agencies to connect with consumers while staying compliant. Our best-in-class data and analytics will play a key role in helping you reach the right consumer, in the right place, at the right time. Learn more

Experian is excited to have been chosen as one of the first data and analytics companies that will enable access to Social Security Administration (SSA) data for the purposes of verifying identity against the Federal Agency’s records. The agency’s involvement in the wake of Congressional interest and successful legislation will create a seismic shift in the landscape of identity verification. Ultimately, the ability to leverage SSA data will reduce the impact of identity fraud and synthetic identity and put real dollars back into the pockets of people and businesses that absorb the costs of fraud today. As this era of government and private sector collaboration begins, many of our clients and partners are breathing a sigh of relief. We see this in a common question our customers ask every day, “Do I still need an analytical solution for synthetic ID now that eCBSV is on the horizon?” The common assumption is that help is on the way and this long tempest of rising losses and identity uncertainty is about to leave us. Or is it? We don’t believe it’s the end of the synthetic ID storm. This is the eye. Rather than basking in the calm light of this moment, we should be thinking ahead and assessing our vulnerabilities because the second half of this storm will be worse than the first. Consider this: The people who develop and exploit synthetic IDs are playing a long game. It takes time, research, planning and careful execution to create an identity that facilitates fraud. The bigger the investment, the bigger the spoils will be. Synthetic ID are being used to purchase luxury automobiles. They’re passing lender marketing criteria and being offered credit. The criminals have made their investment, and it’s unlikely they will walk away from it. So, what does SSA’s pending involvement mean to them? How will they prepare? These aren’t hard questions. They’ll do what you would do in the eye of a storm — maximize the value of the preparations that are in place. Gather what you can quickly and brace yourself for the uncertainty that’s coming. In short, there’s a rush to monetize synthetic IDs on the horizon, and this is no time to declare ourselves safe. It’s doubtful that the eCBSV process will be the silver bullet that ends synthetic ID fraud — and certainly not on day one. It’s more likely that the physical demands of the data exchange, volume constraints, response times and the actionability of the results will take time to optimize. In the meantime, the criminals aren’t going to sit by and watch as their schemes unravel and lose value. We should take some comfort that we’ve made it through the first half of the storm, but recognize and prepare for what still needs to be faced.

A few months ago, I got a letter from the DMV reminding me that it was finally time to replace my driver’s license. I’ve had it since I was 21 and I’ve been dreading having to get a new one. I was especially apprehensive because this time around I’m not just getting a regular old driver’s license, I’m getting a REAL ID. For those of you who haven’t had this wonderful experience yet, a REAL ID is the new form of driver’s license (or state ID) that you’ll need to board a domestic flight starting October 1, 2020. Some states already offered compliant IDs, but others—like California, where I’m from—didn’t. This means that if I want to fly within the U.S. using my driver’s license next year, I can’t renew by mail. It’s Easier Than It Looks Imagine my surprise when I started the process to schedule my appointment, and the California DMV website made things really easy! There’s an online application you can fill out before you get to the DMV and they walk you through the documents to bring to the appointment (which I was able to schedule online). Despite common thought that the DMV and agencies like it are slow to adopt technology, the ease of this process may indicate a shift toward a digital-first mindset. As financial institutions embrace a similar shift, they’ll be better positioned to meet the needs of customers. Case in point, the electronic checklist the DMV provided to prepare me for my appointment. I sailed through the first two parts of the checklist, confirming that I’ll bring my proof of identity and social security number, but I paused when I got to the “Two Proofs of Residency” screen. Like many people my age—read: 85% of the millennial population, according to a recent Experian study—I don’t have a mortgage or any other documents relating to property ownership. I also don’t have my name on my utilities (thanks, roomie) or my cell phone bill (thanks Mom). I do however have a signed lease with my name on it, plus my renter’s insurance, both of which are acceptable as proof of residency. And just like that, I’m all set to get my REAL ID, even though I don’t have some of the basic adulting documents you might expect, because the DMV took into account the fact that not all REAL ID applicants are alike. Imagine if lenders could adopt that same flexibility and create opportunities for the more than 45 million U.S. consumers1 who lack a credit report or have too little information to generate a credit score. The Bigger Picture By removing some of the usual barriers to entry, the DMV made the process of getting my REAL ID much easier than it might have been and corrected my assumptions about how difficult the process would be. Experian has the same line of thought when it comes to helping you determine whether a borrower is credit-worthy. Just because someone doesn’t have a credit card, auto loan or other traditional credit score contributor doesn’t mean they should be written off. That’s why we created Experian BoostTM, a product that lets consumers give read-only access to their bank accounts and add in positive utility and telecommunications bill payments to their credit file to change their scores in real time and demonstrate their stability, ability and willingness to repay. It’s a win-win for lenders and consumers. 2 out of 3 users of Experian Boost see an increase in their FICO Score and of those who saw an increase, 13% moved up a credit tier. This gives lenders a wider pool to market to, and thanks to their improved credit scores, those borrowers are eligible for more attractive rates. Increasing your flexibility and removing barriers to entry can greatly expand your potential pool of borrowers without increasing your exposure to risk. Learn more about how Experian can help you leverage alternative credit data and expand your customer base in our 2019 State of Alternative Data Whitepaper. Read Full Report 1Kenneth P. Brevoort, Philipp Grimm, Michelle Kambara. “Data Point: Credit Invisibles.” The Consumer Financial Protection Bureau Office of Research. May 2015.

Retail banking leaders in a variety of industries (including risk management, credit, information technology and other departments) want to incorporate more data into their business strategies. By doing so, consumer banks and other financial companies benefit by expanding their markets, controlling risk, improving compliance and the customer experience. However, many companies don’t know how or where to start. The challenges? There’s just too much data – and it’s overwhelming. Technical integration issues Maintaining regulatory data and attribute governance and compliance The slow speed of adoption Join Jim Bander, PhD, analytics and optimization leader at Experian, in an upcoming webinar with the Consumer Bankers Association on Tuesday, Oct. 1, 2019 at 9:00-10:00 a.m. PT. The webinar will discuss how some of the country’s best banks – big and small – are making better, faster and more profitable decisions by using the right set of data sources, while avoiding data overload. Key topics will include: Technology Trends: Discover how the latest technology, including the cloud and machine learning, makes it easier than ever to access data, define and manage attributes throughout the enterprise and perform complex calculations in real time. Time to Market: Discover how consumer banks and other financial companies that have mastered data and attribute management are able to integrate data and attributes quickly and seamlessly. Business Benefits: Understand how advanced analytics helps financial institutions of all sizes make better business decisions. This includes growing their portfolios, mitigating fraud and credit risk, controlling operating expenses, improving compliance and enhancing the customer experience. Critical Success Factors: Learn how to stay ahead of ever-evolving business and data requirements and continuously improve your lending operations. Join us as we unveil the secrets to avoiding data overload in consumer banking. Special Offer For non-current CBA members, this webinar costs $95 to attend. However, with special discount code: EX1001, non-CBA members can attend for FREE. Register Now

The future is, factually speaking, uncertain. We don't know if we'll find a cure for cancer, the economic outlook, if we'll be living in an algorithmic world or if our work cubical mate will soon be replaced by a robot. While futurists can dish out some exciting and downright scary visions for the future of technology and science, there are no future facts. However, the uncertainty presents opportunity. Technology in today's world From the moment you wake up, to the moment you go back to sleep, technology is everywhere. The highly digital life we live and the development of our technological world have become the new normal. According to The International Telecommunication Union (ITU), almost 50% of the world's population uses the internet, leading to over 3.5 billion daily searches on Google and more than 570 new websites being launched each minute. And even more mind-boggling? Over 90% of the world's data has been created in just the last couple of years. With data growing faster than ever before, the future of technology is even more interesting than what is happening now. We're just at the beginning of a revolution that will touch every business and every life on this planet. By 2020, at least a third of all data will pass through the cloud, and within five years, there will be over 50 billion smart connected devices in the world. Keeping pace with digital transformation At the rate at which data and our ability to analyze it are growing, businesses of all sizes will be forced to modify how they operate. Businesses that digitally transform, will be able to offer customers a seamless and frictionless experience, and as a result, claim a greater share of profit in their sectors. Take, for example, the financial services industry - specifically banking. Whereas most banking used to be done at a local branch, recent reports show that 40% of Americans have not stepped through the door of a bank or credit union within the last six months, largely due to the rise of online and mobile banking. According to Citi's 2018 Mobile Banking Study, mobile banking is one of the top three most-used apps by Americans. Similarly, the Federal Reserve reported that more than half of U.S. adults with bank accounts have used a mobile app to access their accounts in the last year, presenting forward-looking banks with an incredible opportunity to increase the number of relationship touchpoints they have with their customers by introducing a wider array of banking products via mobile. Be part of the movement Rather than viewing digital disruption as worrisome and challenging, embrace the uncertainty and potential that advances in new technologies, data analytics and artificial intelligence will bring. The pressure to innovate amid technological progress poses an opportunity for us all to rethink the work we do and the way we do it. Are you ready? Learn more about powering your digital transformation in our latest eBook. Download eBook Are you an innovation junkie? Join us at Vision 2020 for future-facing sessions like: - Cloud and beyond - transforming technologies - ML and AI - real-world expandability and compliance

In today’s age of digital transformation, consumers have easy access to a variety of innovative financial products and services. From lending to payments to wealth management and more, there is no shortage in the breadth of financial products gaining popularity with consumers. But one market segment in particular – unsecured personal loans – has grown exceptionally fast. According to a recent Experian study, personal loan originations have increased 97% over the past four years, with fintech share rapidly increasing from 22.4% of total loans originated to 49.4%. Arguably, the rapid acceleration in personal loans is heavily driven by the rise in digital-first lending options, which have grown in popularity due to fintech challengers. Fintechs have earned their position in the market by leveraging data, advanced analytics and technology to disrupt existing financial models. Meanwhile, traditional financial institutions (FIs) have taken notice and are beginning to adopt some of the same methods and alternative credit approaches. With this evolution of technology fused with financial services, how are fintechs faring against traditional FIs? The below infographic uncovers industry trends and key metrics in unsecured personal installment loans: Still curious? Click here to download our latest eBook, which further uncovers emerging trends in personal loans through side-by-side comparisons of fintech and traditional FI market share, portfolio composition, customer profiles and more. Download now

Experian has been named one of the 10 participants, and only credit bureau, in the initial rollout of the SSA's new eCBSV service.

Today is National Fintech Day – a day that recognizes the ever-important role that fintech companies play in revolutionizing the customer experience and altering the financial services landscape. Fintech. The word itself has become synonymous with constant innovation, agile technology structures and being on the cusp of the future of finance. Fintech challengers are disrupting existing financial models by leveraging data, advanced analytics and technology – both inspiring traditional financial institutions in their digital transformation strategies and giving consumers access to a variety of innovative financial products and services. But to us at Experian, National Fintech Day means more than just financial disruption. National Fintech Day represents the partnerships we have carefully fostered with our fintech clients to drive financial inclusion for millions of people around the globe and provide consumers with greater control and more opportunities to access the quality credit they deserve. “We are actively seeking out unresolved problems and creating products and technologies that will help transform the way businesses operate and consumers thrive in our society. But we know we can’t do it alone,” said Experian North American CEO, Craig Boundy in a recent blog article on Experian’s fintech partnerships. “That’s why over the last year, we have built out an entire team of account executives and other support staff that are fully dedicated to developing and supporting partnerships with leading fintech companies. We’ve made significant strides that will help us pave the way for the next generation of lending while improving the financial health of people around the world.” At Experian, we understand the challenges fintechs face – and our real-world solutions help fintech clients stay ahead of constantly changing market conditions and demands. “Experian’s pace of innovation is very impressive – we are helping both lenders and consumers by delivering technological solutions that make the lending ecosystem more efficient,” said Experian Senior Account Executive Warren Linde. “Financial technology is arguably the most important type of tech out there, it is an honor to be a part of Experian’s fintech team and help to create a better tomorrow.” If you’d like to learn more about Experian’s fintech solutions, visit us at Experian.com/Fintech.

Earlier this year, the Consumer Financial Protection Bureau (CFPB) issued a Notice of Proposed Rulemaking (NPRM) to implement the Fair Debt Collection Practices Act (FDCPA). The proposal, which will go into deliberation in September and won't be finalized until after that date at the earliest, would provide consumers with clear-cut protections against disturbance by debt collectors and straightforward options to address or dispute debts. Additionally, the NPRM would set strict limits on the number of calls debt collectors may place to reach consumers weekly, as well as clarify how collectors may communicate lawfully using technologies developed after the FDCPA’s passage in 1977. So, what does this mean for collectors? The compliance conundrum is ever present, especially in the debt collection industry. Debt collectors are expected to continuously adapt to changing regulations, forcing them to spend time, energy and resources on maintaining compliance. As the most recent onslaught of developments and proposed new rules have been pushed out to the financial community, compliance professionals are once again working to implement changes. According to the Federal Register, here are some key ways the new regulation would affect debt collection: Limited to seven calls: Debt collectors would be limited to attempting to reach out to consumers by phone about a specific debt no more than seven times per week. Ability to unsubscribe: Consumers who do not wish to be contacted via newer technologies, including voicemails, emails and text messages must be given the option to opt-out of future communications. Use of newer technologies: Newer communication technologies, such as emails and text messages, may be used in debt collection, with certain limitations to protect consumer privacy. Required disclosures: Debt collectors will be obligated to send consumers a disclosure with certain information about the debt and related consumer protections. Limited contact: Consumers will be able to limit ways debt collectors contact them, for example at a specific telephone number, while they are at work or during certain hours. Now that you know the details, how can you prepare? At Experian, we understand the importance of an effective collections strategy. Our debt collection solutions automate and moderate dialogues and negotiations between consumers and collectors, making it easier for collection agencies to reach consumers while staying compliant. Powerful locating solution: Locate past-due consumers more accurately, efficiently and effectively. TrueTraceSM adds value to each contact by increasing your right-party contact rate. Exclusive contact information: Mitigate your compliance risk with a seamless and unparalleled solution. With Phone Number IDTM, you can identify who a phone is registered to, the phone type, carrier and the activation date. If you aren’t ready for the new CFPB regulation, what are you waiting for? Learn more Note: Click here for an update on the CFPB's proposal.

Big Data, once thought to be overhyped consultant-speak, is now a term and business model so ubiquitous it underpins billions of dollars in revenue across nearly every industry. Similarly, the advanced analytics derived from big data are key to staying relevant in an everchanging global economy and to consumers with expanding expectations. But for many financial institutions, using big data and advanced analytics seemed to only be in reach for big banks with large, advanced data teams. With the expansion of the Experian Ascend Technology PlatformTM, the conversation is changing. Financial institutions of all sizes can now leverage advanced analytics, artificial intelligence and machine learning with new configurations in the award-winning platform. In a release earlier this week, Experian announced new tools and configurations in the Ascend Analytical SandboxTM to fit teams of every size and skill level. Now fintechs, banks and credit unions of every size can have access to Experian’s one-stop source for advanced analytics, business intelligence and ultimately, better decisions. The secure hybrid-cloud environment allows users to combine their own data sets with Experian’s exclusive data assets, including credit, alternative, commercial, auto and more. From there, users can build and test models across different stages of the lending cycle, including originations, prescreen, account management and collections, and seamlessly put their models into production. Experian’s Ascend Analytical Sandbox also allows users to benchmark their portfolios against the industry, identify credit trends and explore new product opportunities. All the insights gathered through the Ascend Analytical Sandbox can be viewed and shared through interactive dashboards and customizable reports that can be pulled in near real time. Additional use cases include: Reject inferencing – refine models, scorecards and strategies by analyzing trades opened by previous applicants who were rejected or approved but did not move forward Prescreen campaigns – design prescreen campaigns, evaluate results and improve strategies Cross-sell – identify cross-sell opportunities for existing customers and identify how they may be working with other lenders Collections strategies, stress testing and loss forecasting – build stronger models to identify customers that have ability and willingness to pay debts, stress test and forecast loss Peer benchmarking and industry trends – compare current portfolio against peers and the industry Recession planning – identify areas to adjust your portfolio to prepare for an economic downturn OneMain Financial, a large provider of personal installment loans serving 10 million total customers across more than 1,700 branches, turned to Experian to improve its risk modeling and credit portfolio management capabilities with the Ascend Analytical Sandbox. Since using the solution, the company has seen significant improvements in reject inferencing – a process that is traditionally expensive, manually-intensive and time consuming. According to OneMain Financial, the Ascend Analytical Sandbox has shortened the process to less than two weeks from up to 180 days. "Experian's Ascend Technology Platform and Analytical Sandbox is an industry gamechanger," said Michael Kortering, OneMain Financial's Senior Managing Director and Head of Model Development. "We're completing analyses that just weren't possible before and we're getting decisions to our clients faster, without compromising risk.” For more information on Ascend Analytical Sandbox SX – the latest solution for financial institutions of all sizes – or other enterprise-wide capabilities of the Experian Ascend Technology Platform, click here.