Fintech

Fintech

Changing consumer behaviors caused by the COVID-19 pandemic have made it difficult for businesses to make good lending decisions. Maintaining a consistent lending portfolio and differentiating good customers who are facing financial struggles from bad actors with criminal intent is getting more difficult, highlighting the need for effective decisioning tools. As part of our ongoing Q&A perspective series, Jim Bander, Experian’s Market Lead, Analytics and Optimization, discusses the importance of automated decisions in today’s uncertain lending environment. Check out what he had to say: Q: What trends and challenges have emerged in the decisioning space since March? JB: In the age of COVID-19, many businesses are facing several challenges simultaneously. First, customers have moved online, and there is a critical need to provide a seamless digital-first experience. Second, there are operational challenges as employees have moved to work from home; IT departments in particular have to place increase priority on agility, security, and cost-control. Note that all of these priorities are well-served by a cloud-first approach to decisioning. Third, the pandemic has led to changes in customer behavior and credit reporting practices. Q: Are automated decisioning tools still effective, given the changes in consumer behaviors and spending? JB: Many businesses are finding automated decisioning tools more important than ever. For example, there are up-sell and cross-sell opportunities when an at-home bank employee speaks with a customer over the phone that simply were not happening in the branch environment. Automated prequalification and instant credit decisions empower these employees to meet consumer needs. Some financial institutions are ready to attract new customers but they have tight marketing budgets. They can make the most of their budget by combining predictive models with automated prescreen decisioning to provide the right customers with the right offers. And, of course, decisioning is a key part of a debt management strategy. As consumers show signs of distress and become delinquent on some of their accounts, lenders need data-driven decisioning systems to treat those customers fairly and effectively. Q: How does automated decisioning differentiate customers who may have missed a payment due to COVID-19 from those with a history of missed payments? JB: Using a variety of credit attributes in an automated decision is the key to understanding a consumer’s financial situation. We have been helping businesses understand that during a downturn, it is important for a decisioning system to look at a consumer through several different lenses to identify financially stressed consumers with early-warning indicators, respond quickly to change, predict future customer behavior, and deliver the best treatment at the right time based on customer specific situations or behaviors. In addition to traditional credit attributes that reflect a consumer’s credit behavior at a single point in time, trended attributes can highlight changes in a consumer’s behavior. Furthermore, Experian was the first lender to release new attributes specifically created to address new challenges that have arisen since the onset of COVID. These attributes help lenders gain a broader view of each consumer in the current environment to better support them. For example, lenders can use decisioning to proactively identify consumers who may need assistance. Q: What should financial institutions do next? JB: Financial institutions have rarely faced so much uncertainty, but they are generally rising to the occasion. Some had already adopted the CECL accounting standard, and all financial institutions were planning for it. That regulation has encouraged them to set aside loss reserves so they will be in better financial shape during and after the COVID-19 Recession than they were during the Great Recession. The best lenders are making smart investments now—in cloud technology, automated decisioning, and even Ethical and Explainable Artificial Intelligence—that will allow them to survive the COVID Recession and to be even more competitive during an eventual recovery. Financial institutions should also look for tools like Experian’s In the Market Model and Trended 3D Attributes to maximize efficiency and decisioning tactics – helping good customers remain that way while protecting the bottom line. In the Market Models Trended 3D Attributes About our Expert: [avatar user="jim.bander" /] Jim Bander, PhD, Market Lead, Analytics and Optimization, Experian Decision Analytics Jim joined Experian in April 2018 and is responsible for solutions and value propositions applying analytics for financial institutions and other Experian business-to-business clients throughout North America. He has over 20 years of analytics, software, engineering and risk management experience across a variety of industries and disciplines. Jim has applied decision science to many industries, including banking, transportation and the public sector.

In 2015, U.S. card issuers raced to start issuing EMV (Europay, Mastercard, and Visa) payment cards to take advantage of the new fraud prevention technology. Counterfeit credit card fraud rose by nearly 40% from 2014 to 2016, (Aite Group, 2017) fueled by bad actors trying to maximize their return on compromised payment card data. Today, we anticipate a similar tsunami of fraud ahead of the Social Security Administration (SSA) rollout of electronic Consent Based Social Security Number Verification (eCBSV). Synthetic identities, defined as fictitious identities existing only on paper, have been a continual challenge for financial institutions. These identities slip past traditional account opening identity checks and can sit silently in portfolios performing exceptionally well, maximizing credit exposure over time. As synthetic identities mature, they may be used to farm new synthetics through authorized user additions, increasing the overall exposure and potential for financial gain. This cycle continues until the bad actor decides to cash out, often aggressively using entire credit lines and overdrawing deposit accounts, before disappearing without a trace. The ongoing challenges faced by financial institutions have been recognized and the SSA has created an electronic Consent Based Social Security Number Verification process to protect vulnerable populations. This process allows financial institutions to verify that the Social Security number (SSN) being used by an applicant or customer matches the name. This emerging capability to verify SSN issuance will drastically improve the ability to detect synthetic identities. In response, it is expected that bad actors who have spent months, if not years, creating and maturing synthetic identities will look to monetize these efforts in the upcoming months, before eCBSV is more widely adopted. Compounding the anticipated synthetic identity fraud spike resulting from eCBSV, financial institutions’ consumer-friendly responses to COVID-19 may prove to be a lucrative incentive for bad actors to cash out on their existing synthetic identities. A combination of expanded allowances for exceeding credit limits, more generous overdraft policies, loosened payment strategies, and relaxed collection efforts provide the opportunity for more financial gain. Deteriorating performance may be disguised by the anticipation of increased credit risk, allowing these accounts to remain undetected on their path to bust out. While responding to consumers’ requests for assistance and implementing new, consumer-friendly policies and practices to aid in impacts from COVID-19, financial institutions should not overlook opportunities to layer in fraud risk detection and mitigation efforts. Practicing synthetic identity detection and risk mitigation begins in account opening. But it doesn’t stop there. A strong synthetic identity protection plan continues throughout the account life cycle. Portfolio management efforts that include synthetic identity risk evaluation at key control points are critical for detecting accounts that are on the verge of going bad. Financial institutions can protect themselves by incorporating a balance of detection efforts with appropriate risk actions and authentication measures. Understanding their portfolio is a critical first step, allowing them to find patterns of identity evolution, usage, and connections to other consumers that can indicate potential risk of fraud. Once risk tiers are established within the portfolio, existing controls can help catch bad accounts and minimize the resulting losses. For example, including scores designed to determine the risk of synthetic identity, and bust out scores, can identify seemingly good customers who are beginning to display risky tendencies or attempting to farm new synthetic identities. While we continue to see financial institutions focus on customer experience, especially in times of uncertainty, it is paramount that these efforts are not undermined by bad actors looking to exploit assistance programs. Layering in contextual risk assessments throughout the lifecycle of financial accounts will allow organizations to continue to provide excellent service to good customers while reducing the increasing risk of synthetic identity fraud loss. Prevent SID

Achieving collection results within the subprime population was challenging enough before the current COVID-19 pandemic and will likely become more difficult now that the protections of the Coronavirus Aid, Relief, and Economic Security (CARES) Act have expired. To improve results within the subprime space, lenders need to have a well-established pre-delinquent contact optimization approach. While debt collection often elicits mixed feelings in consumers, it’s important to remember that lenders share the same goal of settling owed debts as quickly as possible, or better yet, avoiding collections altogether. The subprime lending population requires a distinct and nuanced approach. Often, this group includes consumers that are either new to credit as well as consumers that have fallen delinquent in the past suggesting more credit education, communication and support would be beneficial. Communication with subprime consumers should take place before their account is in arrears and be viewed as a “friendly reminder” rather than collection communication. This approach has several benefits, including: The communication is perceived as non-threatening, as it’s a simple notice of an upcoming payment. Subprime consumers often appreciate the reminder, as they have likely had difficulty qualifying for financing in the past and want to improve their credit score. It allows for confirmation of a consumer’s contact information (mainly their mobile number), so lenders can collect faster while reducing expenses and mitigating risk. When executed correctly, it would facilitate the resolution of any issues associated with the delivery of product or billing by offering a communication touchpoint. Additionally, touchpoints offer an opportunity to educate consumers on the importance of maintaining their credit. Customer segmentation is critical, as the way lenders approach the subprime population may not be perceived as positively with other borrowers. To enhance targeting efforts, lenders should leverage both internal and external attributes. Internal payment patterns can provide a more comprehensive view of how a customer manages their account. External bureau scores, like the VantageScore® credit score, and attribute sets that provide valuable insights into credit usage patterns, can significantly improve targeting. Additionally, the execution of the strategy in a test vs. control design, with progression to successive champion vs. challenger designs is critical to success and improved performance. Execution of the strategy should also be tested using various communication channels, including digital. From an efficiency standpoint, text and phone calls leveraging pre-recorded messages work well. If a consumer wishes to participate in settling their debt, they should be presented with self-service options. Another alternative is to leverage live operators, who can help with an uptick in collection activity. Testing different tranches of accounts based on segmentation criteria with the type of channel leveraged can significantly improve results, lower costs and increase customer retention. Learn About Trended Attributes Learn About Premier Attributes

The COVID-19 pandemic created a global shift in the volume of online activity and experiences over the past several months. Not only are consumers increasing their usage of mobile and digital channels to bank, shop, work and socialize — and anticipating more of the same in the coming months — they’re closely watching how businesses respond to their needs. Between late June and early July of this year, Experian surveyed 3,000 consumers and 900 businesses to explore the shifts in consumer behavior and business strategy pre- and post-COVID-19. More than half of businesses surveyed believe their operational processes have mostly or completely recovered since COVID-19 began. However, many consumers fear that a second wave of COVID-19 will further deplete their already strained finances. They are looking to businesses for reassurance as they shift their behaviors by: Reducing discretionary spending Building up emergency savings Tapping into financial reserves Increasing online spending Moving forward, businesses are focusing on short-term investments in security, managing credit risk with artificial intelligence, and increasing online customer engagement. Download the full report to get all of the insights into global business and consumer needs and priorities and keep visiting the Insights blog in the coming weeks for a deeper dive into US-specific findings. Download the report

In today’s uncertain economic environment, the question of how to reduce portfolio volatility while still meeting consumers’ needs is on every lender’s mind. With more than 100 million consumers already restricted by traditional scoring methods used today, lenders need to look beyond traditional credit information to make more informed decisions. By leveraging alternative credit data, you can continue to support your borrowers and expand your lending universe. In our most recent podcast, Experian’s Shawn Rife, Director of Risk Scoring and Alpa Lally, Vice President of Data Business, discuss how to enhance your portfolio analysis after an economic downturn, respond to the changing lending marketplace and drive greater access to credit for financially distressed consumers. Topics discussed, include: Making strategic, data-driven decisions across the credit lifecycle Better managing and responding to portfolio risk Predicting consumer behavior in times of extreme uncertainty Listen in on the discussion to learn more. Experian · Effective Lending in the Age of COVID-19

Experian’s Chris Ryan and Bobbie Paul recently re-joined David Mattei from Aite to discuss how emerging fraud trends and changes in consumer behavior will have long-term impacts on businesses. Chris, Bobbie, and David have combined experience of more than 60 years in the world of fraud prevention. In this discussion, they bring that experience to bear as they review how businesses should revise their long-term fraud strategy in response to COVID-19 and the subsequent economic shifts, including: The requirements to authenticate a digital customer Businesses’ technology challenges Differentiating between first party and third party fraud The importance of businesses’ technology investment How to build a roadmap for the next 90 days and beyond Experian · Make Your Fraud Plan Recession-Ready: Your 90 Day and Beyond Plan

Pre COVID-19, operations functions for retailers and financial institutions had not typically consisted of a remote (stay at home) workforce. Some organizations were better prepared than others, but there is a firm belief that retail and banking have changed for good as a result of the pandemic and resulting economic and workforce shifts. Market trends and implications When stay at home orders were issued, non-essential brick and mortar businesses closed unexpectedly. What were retailers to do with no traffic coming through the doors at their physical locations? The impact on big-box retailers like Best Buy, Dick’s Sporting goods, Sears, JCPenney, Nike, Starbucks, Macy’s, Neiman Marcus, Nordstrom, Kohl’s to name a few, has been unprecedented; some have had to shut their doors for good. Over the past several months global retail has seen e-commerce sales grow over 81% compared to the same period last year, according to Card Not Present. Some sectors have seen triple-digit growth year over year. Most online retailers have been ill-prepared to handle this increase in transactional volume in such a short amount of time, which has resulted in rapid fraud loss increases. A recent white paper from Aite Group reported that prior to COVID-19, a large financial institution forecasted an 8% decrease in fraud for 2020, but has since revised the projection to increase 10-15%. What does this all mean? Bad actors are taking advantage of the pandemic to exploit the online retail channel. The increased remote channel usage—online, mobile, and contact centers in particular—continues to be an area where retailers are exposed. Account takeover, through phishing and relaxed call center controls, is rising as well. Increases in phishing attacks are leading to compromised and stolen identities and synthetic identity fraud. Account takeover (ATO) fraud has increased 347% since 2019 according to PYMNTS.com. A recent survey found more than a quarter of merchants (27%) admit that they don’t have measures to prevent ATO. 24% of merchants can’t identify an ATO during a purchase. 14% of merchants say they are not even aware that an ATO has occurred unless a customer contacts them. When criminals use these compromised accounts to make fraudulent purchases, the merchant loses revenue and the value of the goods. They can also suffer from damage to brand reputation and a loss of customer confidence. A lack of account security can have lasting effects as 65% of customers surveyed say they would likely stop buying from a merchant if their account was compromised, according to that same Card Not Present study. So how can retailers start to identify bad actors with malicious intent? This will be a constant struggle for retailers. Rather than a one size fits all solution, retailers must move toward a strategy that is nimble and dynamic and can address multiple areas of exposure. A fraudster could easily slip by one verification method—for instance with a stolen credential—only to be foiled by a secondary authentication tactic like device identity. A layered fraud strategy continues to be the industry best practice, where both passive and active authentication methods are leveraged to frustrate fraudsters without applying undue friction to “good” consumers. The layered solution should also utilize device risk, identity verification and fraud analytics, with tailoring to each businesses’ needs, risk tolerance, and customer profiles. Learn more about how to build a layered fraud strategy today. Learn more

Every few months we hear in the news about a fraud ring that has been busted here in the U.S. or in another part of the world. In May, I read about a fraud ring based in Georgia and Louisiana that bought 13,000 stolen identities of children who were on the Louisiana Medicaid program and billed the government for services not rendered. This group defrauded the Medicaid program of more than $500,000. This is just one of many stories that we hear about fraud rings, and given the rapidly changing economic environment, now is the time for businesses to think about how to protect against fraud rings. There are a number of challenges that organizations may have when it comes to sharing trends and collaborations, understanding the ways to tie fraud rings together, creating treatments for identifying fraud rings and ways to store and catalogue fraud ring experiences so they can be easily recognized. The trouble with identifying fraud rings It’s important to understand the challenges that organizations have because they see the fraud rings through their own internal lens. Here are a few of the top things businesses should work on: Think like a fraudster. This will help businesses become more creative in their approach to fraud prevention. Facilitate internal collaboration. Share with in-organization partners. Sometimes this can be difficult due to organizational structure. Promote external collaboration. Intel-sharing groups are a great way for businesses to network within their industries and learn about the fraud that others are seeing. An organization that I’ve worked with in the past is the National Cyber Forensic and Training Alliance (NCFTA). Putting the pieces together How do businesses identify a fraud ring? There are three steps to get started. The first is reviewing and understanding the data. Fraudsters are lazy and want to replicate the process over and over again, and because of this there is always some piece of information that is repeated. It could be a name, an email address, device fingerprint, or similar. The second step is tying the fraud ring together. This is done by creating rules to help identify the trends. Having rules in place to identify fraud rings allows businesses to easily pull stats together for their leadership. Lastly, applying an acronym or name to the particular fraud ring and adding comments to the cases associated with a particular ring will help with post-investigation analysis. Learning from the past Before I became a consultant, I remember identifying a fraud ring that was submitting events with the same language pack and where the device fingerprint was staying consistent. Those events were being referred out for review and marked with the same note. At a post-mortem review, I was able to talk to the fraud ring we had seen, and it was easy to pull all events associated with this fraud ring because my team had marked the events with the same comments. Another fraud ring example happened a few years ago. A client called me and said that they were under a fraud attack and this fraud ring was rotating the email handle. I reviewed the data and came up with a rule to catch this activity. Fraud rings will use email handle rotation to help them keep track of accounts that are opened or what emails they used in the past. By coupling the email handle rotation with an email verification service like Emailage, this insight could be very telling. I would assume that when fraud rings use email handle rotation these emails are new and have just been created. These are just a few of the many fraud rings that I’ve encountered over the course of my career and I’m sure there will be a lot more in the years to come. The best advice I can give to anyone that reads this post is to understand the data that you are reviewing, look for anomalies within the data, ask questions and test your theories by running queries on the data that you’re reviewing. I would love to hear about the different fraud rings that you’ve encountered over your career. Stay safe. Contact us

Experian’s own Chris Ryan and Bobbie Paul recently joined David Mattei from Aite to discuss the latest research and insights into emerging fraud schemes and how businesses can combat them in light of COVID-19 and the resulting economic changes. Between them, Chris, Bobbie, and David have more than 60 years of experience in the world of fraud prevention. Listen in as they discuss how businesses can shape their fraud prevention plan in the short term, including: The impacts of the health crisis and physical distancing The rise of e-commerce and consumer digital engagement Changes in criminal activity Fraud attack vectors 2020 fraud loss projections Critical next steps for the 30-60 day time frame Experian · Make Your Fraud Plan Recession-Ready: 2020 Fraud Trends

Today, Experian and Oliver Wyman launched the Ascend Portfolio Loss ForecasterTM, a solution built to help lenders make better decisions – during COVID-19 and beyond – with customized forecasts and macroeconomic data. Phrases like “the new normal,” “unprecedented times,” and “extreme economic volatility” have flooded not only media for the last few months, but also financial institutions’ strategic discussions regarding plans to move forward. What has largely been crisis response is quickly shifting to an urgent need to answer the many questions around “Will we survive this crisis?,” let alone “What’s next?” And arguably, we’ve entered a new era of loss forecasting. After the longest period of economic growth in post-war U.S. history, previously built models are not sufficient for the unprecedented and sudden changes in economic conditions due to COVID-19. Lenders need instant insights to assess impact and losses to their portfolios. The Ascend Portfolio Loss Forecaster combines advanced modeling from Oliver Wyman, pandemic-specific insights and macroeconomic scenarios from Oxford Economics, and Experian’s quality data to analyze and produce accurate loan loss forecasts. Additionally, all of the data, including the forecasts and models, are regularly updated as macroeconomic conditions change. “Experian’s agility and innovative technologies allow us to help lenders make informed decisions in real time to mitigate future risk,” said Greg Wright, chief product officer of Experian’s Consumer Information Services, in a recent press release. “We’re proud to work with our partners, Oxford Economics and Oliver Wyman, to bring lenders a product powered by machine learning, comprehensive data and macroeconomic forecast scenarios.” Built using advanced modeling and expert scenarios, the web-based application maximizes the more than 15 years of Experian’s loan-level data, including VantageScore® credit score, bankruptcy scores and customer-level attributes. Financial institutions can gauge loan portfolio performance under various scenarios. “It is important that the banks take into account the evolving credit behaviors due to the COVID-19 pandemic, in addition to the robust modeling technique for their loss forecasting and strategic decisioning,” said Anshul Verma, senior director of products at Oliver Wyman, also in the release. “With the Ascend Portfolio Loss Forecaster, lenders get robust models that work in the current conditions and take into account evolving consumer behaviors,” Verma said. To watch Experian’s webinar on portfolio loss forecasting, please click here and to learn more about the Ascend Portfolio Loss Forecaster, click the button below. Learn More

The COVID-19 pandemic and resulting rush to transition to a remote lifestyle made it clear that many businesses need a refreshed digital authentication and fraud prevention strategy that includes an investment in technology and provides consumer assurance. This is particularly important when it comes to identity, as many of the standard in-person verification methods and tools are currently unavailable. The meaning of identity is growing and shifting Technology trends are intersecting with social trends to create heightened awareness, and a whole new public conversation has emerged around customer trust and privacy. Attitudes and ideas are changing—even to the point of what we mean by “identity.” An identity is no longer just a name, date of birth, and SSN. Now, there are digital manifestations everywhere you look: screen names, email addresses, mobile phone numbers, device identifiers, and the other “exhaust” we leave behind as we travel the internet. This leads to concerns about what an identity is, who owns it, and who manages and protects it. Businesses have to be able to prove to their ability to protect their customers’ identities through investment in technology and a robust fraud strategy. Consumer attitudes are changing Several years ago, consumers were excited by all the new digital capabilities and the speed, ease, and convenience they provided. Last year, Experian found that consumers still wanted those things, with 70% willing to provide more information to businesses if there was a perceived benefit. However, they also wanted more security in the balance. In Experian’s most recent Global Identity and Fraud Report, we found that 74% of consumers say that security is the most important factor when deciding to engage with a business. Consumers are particularly more tolerant of friction during the enrollment process—as a means of building trust. But, when they return to the app or website, they want to be recognized. This means achieving a balance by using layered technologies, some of which are active and visible to the consumer, and some of which are invisibly working in the background to confirm the identity of returning consumers. Consumer attitudes vs. regulatory pressure The drivers behind the business changes are twofold: shifting consumer attitudes and regulatory changes. While regulations are becoming stricter on a national and global level, they’re not keeping pace with technology and social change. The digital world is evolving at a rapid pace, opening up more new ways for companies to collect information about consumers and use it to identify and verify, and also to target goods and services. With all of this data available, it’s important for businesses to use the tools in the market to help protect identity information. Next steps in technology The bottom line is, businesses can’t wait for regulations to dictate how best to protect information. Instead, they should be looking to technologies like physical and behavioral biometrics to help provide identity authentication and protection – layering those solutions with information from the user and from third parties to give a holistic consumer view. Businesses should adopt a platform approach for identity and fraud in order to be able to adapt quickly, whether to incorporate new kinds of technology or to prevent emerging types of fraud. By investing in technology now, even in the midst of the COVID-19 pandemic, businesses can build the flexibility needed to respond to future crises and help offset future fraud losses. In turn, those fraud-loss savings can then be used to help grow the business in the future. Learn more about Experian’s commitment to helping businesses maximize their investment in technology to safeguard against fraud. Learn more

To combat the growing threat of synthetic identity fraud, Experian recently announced the launch of Sure ProfileTM, a revolutionary change to the credit profile that gives lenders peace of mind with Experian’s commitment to share in losses that result from an identity we’ve assured. “Experian has always been a leader in combatting fraud, and with Sure Profile, we’re proud to deliver an industry-first fraud offering integrated into the credit profile that mitigates lender losses while protecting millions of consumers’ identities,” said Robert Boxberger, President of Decision Analytics, Experian North America. Synthetic identity fraud is expected to drive $48 billion in annual online payment fraud losses by 2023. Between opportunistic fraudsters and a lack of a unified definition for synthetic identity theft it can be nearly impossible to detect—and therefore prevent—this type of fraud. This breakthrough solution provides a composite history of a consumer’s identification, public record, and credit information and determines the risk of synthetic fraud associated with that consumer. It’s not just a fraud tool, it’s a comprehensive credit profile that utilizes premium data so lenders can make positive credit decisions. Sure Profile leverages the capabilities of the Experian Ascend Identity PlatformTM and uses Experian’s industry-leading data assets and data quality to drive advanced analytics that set a higher level of protection for lenders. It’s powered by newly-developed machine learning and AI models. And it offers a streamlined approach to define and detect synthetic identities early in the originations process. Most importantly, Sure Profile differentiates between real people and potentially risky applicants so lenders can increase application approvals with greater assurance and less risk. “Experian can confidently define and help detect synthetic fraud. That's why we can help stop it,” said Craig Boundy, CEO of Experian North America. “Experian stands behind our data with assurance given to our clients. It’s better for lenders and it’s better for consumers.” Sure Profile is a complement to our robust set of identity protection and fraud management capabilities, which are designed to address fraud and identity challenges including account openings, account takeovers, e-commerce fraud and more. This first-of-its kind profile is the future of underwriting and portfolio protection and it’s here now. Read press release Learn More About Sure Profile

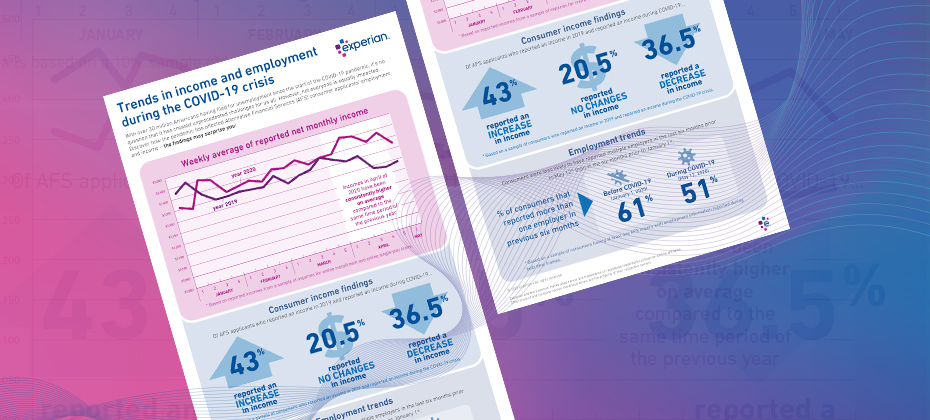

With many individuals finding themselves in increasingly vulnerable positions due to COVID-19, lenders must refine their policies based on their consumers’ current financial situations. Alternative Financial Services (AFS) data helps you gain a more comprehensive view of today's consumer. The COVID-19 pandemic has had far-reaching economic consequences, leading to drastic changes in consumers’ financial habits and behavior. When it comes to your consumers, are you seeing the full picture? See if you qualify for a complimentary hit rate analysis Download AFS Trends Report

The economic impact of the COVID-19 health crisis is ever-evolving and requires great flexibility and planning from lenders. Shannon Lois, Experian’s Senior Vice President, Analytics, Consulting and Operations, discusses what lenders can expect and next steps to take. Q: Though COVID-19 is catalyzing a sharp economic slowdown, many experts expect it to be temporary and liken it more to a global natural disaster than the prior financial crisis. What are your reactions? SL: There is still debate as to whether we will have a U-shaped or a V-shaped recession and its probable severity and longevity. Regardless, we are in a recession caused by a health pandemic with uncertainty of what it will mean for our global economy and without a clear view as to when it will end. The sooner we can contain the virus the more it will help to curtail the size of the recession. The unemployment rates and the consumer lack of confidence in the future will continue to contract spending which in turn will continue to propagate the recession. Our ability to limit COVID-19 over the coming months will have a direct impact in the economy, although the effects will probably linger on for six or more months. Q: From an economic perspective, what are the current trends we’re seeing? SL: Unemployment has skyrocketed and every business sector has been impacted although with different degrees of severity. In particular, tourism/hospitality, airlines, automotive, consumer products and retail have suffered. Consumers’ financial status varies and will continue to fluctuate, and credit conditions tighten while welfare payments increase. The government programs that have started will help, but they’re not enough to counter a prolonged recession. As some states seek to reopen and others extend their shelter in place orders, we will continue to see economic changes, with different sectors bouncing back or dipping further depending on their geographic location. Q: How does the economic slowdown compare to what we may have expected previously? SL: This recession is different than anything we have encountered previously not only because of the health concerns and implication of our population but because of the uncertainty of it all. As an example, social distancing has significantly and immediately impacted consumer demand but overall it is their low confidence in the future that will cause a continuous drop in discretionary and non-discretionary spending. Not only do we have challenges on the demand side, we also are seeing the same on the supply side with no automotive manufacturing occurring in the USA, and international oil flooding the market causing negative impact on domestic oil and the broad energy market. Q: How do the unemployment and liquidity challenges come into play? SL: The unemployment rate has already jumped to a record high. Most consumers are facing liquidity and affordability challenges and businesses do not have enough cash reserves to sustain them. Consumer activity has shifted drastically across all channels while lenders are exercising more caution. If this is a V-shaped recession (and hopefully it will be), then most activity is bound to spring back quickly in Q3. With companies safeguarding some jobs and the help of governments’ supplemental programs, businesses will restore supply and consumer demand will get a kick start. Q: What is the smartest next play for financial institutions? SL: The path forward requires several steps. First, understand your customers, existing and new. Refine your policies with the right information around your customers’ financial situations and extend programs (forbearance and loan payment forgiveness) as needed under the right guidelines. It’s also important to use refreshed data to lend to consumers and businesses who need it now more than ever, with the proper policies and fraud checks in place. Finally, increase your agility to operate effectively and dynamically with automation, interactive communication and self-serving digital tools. Experian is committed to helping lenders throughout these uncertain times. For more resources, visit our Look Ahead 2020 Resource Hub. Learn more About Our Expert Shannon Lois, Senior Vice President, Analytics, Consulting and Operations, Decision Analytics Shannon and her team of analysts, scientists, credit, fraud and marketing risk management experts provide results-driven consulting services and state-of-the-art advanced analytics, science and data products to clients in a wide range of businesses, including banking, auto, credit, utility, marketing and finance. Prior to her current role, she founded the Advisory Services practice at Experian, driving to actionable and proven solutions for our clients’ most pressing business problems.

When running a credit report on a new applicant, you must ensure Fair Credit Reporting Act (FCRA) compliance before accessing, using and sharing the collected data. The Coronavirus Aid, Relief, and Economic Security (CARES) Act has impacted credit reporting under the FCRA, as has new guidance from the Consumer Financial Protection Bureau (CFPB). Recent updates include: The CARES Act amended the FCRA to require furnishers who agree to an “accommodation,”1 to report the account as current, although it is permitted to continue to report the account as delinquent if the account was delinquent before the accommodation was made. Although not legally obligated, data furnishers should continue furnishing information to the credit reporting agencies (CRAs) during the COVID-19 crisis, and make sure that information reported is complete and accurate. Below is a brief FCRA-related compliance overview2 covering various FCRA requirements3 when requesting and using consumer credit reports for an extension of credit permissible purpose. For more information regarding your responsibilities under the FCRA as a user of consumer reports, please consult your Legal Counsel and the Notice to Users of Consumer Reports: Obligations of Users Under the FCRA handbook located on our website. Before obtaining a consumer report you have… Reviewed your federal and state regulations and laws related to consumer reports, scores, decisions, etc. Made sure you have a valid permissible purpose for pulling the consumer report. Certified compliance to the CRA from which you are getting the consumer report. You have certified that you complied with all the federal and state requirements. After you take an adverse action based on a consumer report you… Provide the consumer with an oral, written or electronic notice of the adverse action. Provide written or electronic disclosure of the numerical credit score used to take the adverse action, or when providing a “risk-based pricing” notice. Provide the consumer with an oral, written or electronic notice, which includes the below information: Name, address and telephone number of CRA that supplied the report, if nationwide. A statement that the CRA did not make the adverse decision and therefore can’t explain why the decision was made. Notice of the consumer’s right to a free copy of their report from the CRA, if requested within 60 days. Notice of the consumer’s right to dispute with the CRA the accuracy or completeness of any information in a consumer report provided by the CRA. Provide the consumer with a “risk-based pricing” notice if credit was granted but on less favorable terms based on information in their consumer report. We understand how challenging it is to understand and meet all your obligations as a data furnisher – we’re here to make it a little easier. Click below to speak with a representative and gain more insight on how the CARES Act impacts FCRA reporting. Download overview Speak with a representative 1An “accommodation” is defined as “an agreement to defer one or more payments, make a partial payment, forbear any delinquent amounts, modify a loan or contract, or any other assistance or relief” granted to a consumer affected by COVID-19 during the covered period. 2This FCRA overview is not legal guidance and does not enumerate all your requirements under the FCRA as a user of consumer reports. Additionally, this FCRA Overview is not intended to provide legal advice or counsel you regarding your obligations under the FCRA or any other federal or state law or regulation. Should you have any questions about your institution’s specific obligations under the FCRA or any other federal or state law or regulation, you should consult with your Legal Counsel. 3This FCRA overview is intended to be used solely by financial service providers when extending credit to consumers and does not include all FCRA regulatory obligations. You are responsible for regulatory compliance when requesting and using consumer reports, which includes adhering to all applicable federal and state statutes and regulations and ensuring that you have the correct policies and procedures in place.