Public Sector

Public Sector

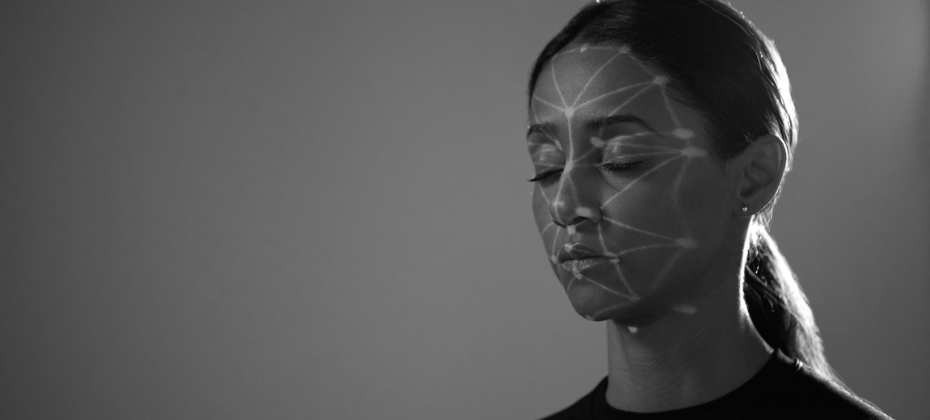

Over the past year and a half, the development of digital identity has shifted the ways businesses interact with consumers. Companies across every industry have incorporated digital services, biometrics, and other verification tools to enhance the consumer experience without increasing risk. Changing consumer expectations A digital identity strategy is no longer a nice-to-have, it’s table stakes. Consumers expect to be recognized across platforms and have a seamless experience every time. 89% of consumers use mobile banking 80% of companies now have a customer recognition strategy in place 55% of banking customers say they plan to visit the bank branch less often moving forward Businesses are responding to these changing expectations while working to grow during the economic recovery – trying to balance consumer experience with risk appetite and bottom-line goals. The present state of digital identity Digital identity strategies require both standardization and interoperability. The first provides the ability to consistently capture data and characteristics that can be used to recognize a specific individual. The second allows businesses to resolve an identity to a specific person – recognizing a phone number, user ID and password, or a device – and use that information to determine if the user of the identity is in fact the identity owner. There are some roadblocks on the road to a seamless digital identity strategy. Issues include a lack of consumer trust and an ambiguous regulatory landscape – creating friction on both ends of the equation. Recipe for success To succeed, businesses need a framework that can reliably use different combinations of physical and digital identity data to determine that the person behind the identity is a known, verified, and unique individual. A one-size-fits-all solution doesn’t exist. However, a layered approach allows businesses to modernize identity, providing the services consumers want and expect while remaining agile in an ever-changing environment. In our newest white paper, developed in partnership with One World Identity, we explore the obstacles hindering digital identity management, and the best way to build a layered solution that is flexible, trustworthy, and inclusive. To learn more, download our “Capturing the Digital Evolution Through a Layered Approach” white paper. Download white paper

The tax gap—the difference between what taxpayers should pay and what they actually pay on time—can have a substantial impact on states’ budgets. Tax agencies and other state departments are responsible for helping states manage their budgets by minimizing expected revenue shortfalls. Underreported income is a significant budget complication that continues to frustrate even the most effective tax agencies, until the right tools are brought into play. The Problem Underreporting is a large, complex issue for agencies. The IRS currently estimates the annual tax gap at $441 billion. There are multiple factors that comprise that total, but the most prevalent is underreporting, which represents 80% of the total tax gap. Of that, 54% is due to underreporting of individual income tax. In addition to being the largest contributor to the tax gap, underreporting is also extremely challenging to identify out of the millions of returns being filed. With 85% of taxes owed correctly reported and paid, finding underreporting can be like trying to locate a needle in the proverbial haystack. Making this even more challenging is the limited resources available for auditing returns, which makes efficiency key. The Solution Data, combined with artificial intelligence (AI) equals efficient detection. The problem with trying to detect which returns are most likely to have underreported income is similar to many other challenges Experian has solved with AI. Partnerships between Experian and state agencies combine what we know about consumers with what their agency knows about their population. We can take the data and use AI to separate the signal from the noise, finding opportunities to recoup lost revenue. Read our case study on how Experian was able to help an agency identify instances of underreporting, detecting an estimated $80 million annual lost revenue from underreported income. Download case study Contact us

Experian recently announced its expansion into Employer Services and the release of a new suite of real-time income and employment verification products, Experian Verify™. The COVID-19 pandemic amplified lenders' need for deeper insights into a consumer's financial situation. At the same time, employers were flooded with record-breaking unemployment claims, while managing stay-at-home orders, income and employment verification fulfillment requests, and more. "We're committed to helping employers, businesses, lenders, and consumers on the road to recovery from the pandemic and beyond," said Alex Lintner, Group President Experian Consumer Information Services. "To support this, we're building two businesses: Experian Employer Services and Verification Solutions. These businesses will create meaningful change and provide our clients with competitive options to achieve their verification needs while helping improve access to credit for consumers." With Experian Verify, lenders can quickly and easily create a more complete picture of a consumer's financial situation by verifying an applicant's income and employment status. Powered by our growing network of payroll and proprietary employer data, Experian Verify offers lenders flexible and secure access to income and employment records. With a consumer's consent, lenders can request the information from Experian and an income and employment report can be delivered to lenders through an API, online Experian dashboard, or paired with an Experian credit report. "As we begin to recover from the COVID-19 pandemic and employers are reopening their doors, we're confident we have assembled the best-of-the-best to help employers overcome their toughest challenges. We're committed to leveraging our combined capabilities and focus on high-touch customer service to deliver secure, scalable and transparent services to employers," said Michele Bodda, President of Experian Mortgage, Employer Services and Verification solutions. Visit us for more information on Experian Verify and Experian's Employer Services. Contact us

Recently, I wrote about how Experian is assisting NASWA (National Association of State Workforce Agencies) with identity verification to help mitigate the spike in fraudulent unemployment insurance claims. Because of this I was not all that surprised when I found a letter in my mailbox from the Texas Workforce Commission with a fraudulent claim using my identity, inspiring me to follow up on this topic with a focus on fraud prevention best practices. Identity theft is on the rise According to Experian data analysis and a recent study on unemployment insurance fraud, at least 25% of new claims are a result of identity theft. This is 50 times higher than what we have traditionally seen in the highest ID theft fraud use case, new credit card applications, which generally amounts to less than 0.5% of new applications. Increasing digitization of the last few years—culminating in the huge leap forward in 2020—has resulted in a massive amount of information available online. Of that information, a reported 1.03 billion records were exposed between 2016 and 2020. There are currently approximately 330 million Americans, so on average more than three records per person have been exposed, creating an environment ripe for identity theft. In fact, a complete identity consisting of name, address, date of birth, and Social Security number (SSN) can be purchased for as little as $8. This stolen data is then often leveraged by both criminal rings who are able to perpetrate fraud on a large scale and smaller scale opportunists – like the ones in Riverside, CA leveraging access to identities of prison inmates. Fraud prevention through layered identity controls In the 20 years that I have been combatting ID theft both in the private and public sectors, I’ve learned that the most effective identity proofing goes beyond traditional identity resolution, validation, and verification. To be successful, you must take advantage of all available data and incorporate it into a layered and risk-based approach that utilizes device details, user behavior, biometrics, and more. Below, I outline three key layers to design an effective process for ID proofing new unemployment insurance claims. Layer 1: Resolve and Validate Identities Traditional identity data consists of the same basic information—name, address, date of birth, telephone number, and SSN—which is now readily available to fraudsters. These have been the foundation for ID proofing in the past and are still critical to resolving the identity in question. The key is to also include additional identity elements like email address and phone number to gain a more holistic view of the applicant. Layer 2: Assess Fraud Risk Determining an identity belongs to a real-life subject is not sufficient to mitigate the risk of ID theft associated with a new unemployment insurance claim. You must go beyond identity validation to assess the risk associated with their claim. Risk assessment risk falls into two categories – identity and digital risk. Identity Risk When assessing a claim, it’s important to check the identity for: Velocity: How often have you (or other states) seen the information being presented with this application? Has the information been associated with multiple identities? Recency of change: How long has the identity been associated with the contact information (phone, email, address, etc.)? Red flags: Has the subject been a recent victim of ID theft, or are they reported as deceased? Synthetic Identity: Are there signs that the identity itself is fictitious or manipulated and does not belong to a real-life person? Digital Risk Similar to the identity risk layer above, the device itself and how the subject interacts with the device are significantly important in identifying the likelihood a new claim is fraudulent. Device risk can be assessed by utilizing geolocation and checking for inconsistent settings or high-risk browsers, while behavioral risk might check for mouse movement, typing speed, or screen pressure. Layer 3: Verify Highest Risk Subjects The final stage in this process is to require additional verification for the highest risk claims, which helps to balance the experience of your valid subjects while minimizing the impact of fraud. Additional steps might include: Document verification: Scanning a government-issued ID (driver’s license, passport, or similar), which includes assessing for document security features and biometric comparison to the applicant. One-time passcode (OTP): It is key to deploy this sparingly only to phone numbers that have been associated with the subject for a significant time frame and incorporate checks to determine if it is at high risk (e.g., recently ported or forwarded). Knowledge-based verification (KBV): Leveraging non-public information from a variety of sources. By adding additional, context-based identity elements, it becomes possible to improve the three main objectives of most agencies’ identity proofing process – get good constituents through the first time, protect the agency and citizens from fraud, and deliver a smooth and secure customer experience in online channels. While there’s no quick fix to prevent unemployment insurance fraud, a layered identity strategy can help prevent it. Finding a partner that has a single, holistic solution empowers agencies to defend against unemployment insurance fraud while minimizing friction for the end-user, and preparing for future fraud schemes. To learn more about how you can protect your constituents and your agency from unemployment insurance fraud request a call today. Contact us

Recently, I shared articles about the problems surrounding third-party and first-party fraud. Now I’d like to explore a hybrid type – synthetic identity fraud – and how it can be the hardest type of fraud to detect. What is synthetic identity fraud? Synthetic identity fraud occurs when a criminal creates a new identity by mixing real and fictitious information. This may include blending real names, addresses, and Social Security numbers with fabricated information to create a single identity. Once created, fraudsters will use their synthetic identities to apply for credit. They employ a well-researched process to accumulate access to credit. These criminals often know which lenders have more liberal identity verification policies that will forgive data discrepancies and extend credit to people who appear to be new or emerging consumers. With each account that they add, the synthetic identity builds more credibility. Eventually, the synthetic identity will “bust out,” or max out all available credit before disappearing. Because there is no single person whose identity was stolen or misused there’s no one to track down when this happens, leaving businesses to deal with the fall out. More confounding for the lenders involved is that each of them sees the same scam through a different lens. For some, these were longer-term reliable customers who went bad. For others, the same borrower was brand new and never made a payment. Synthetic identities don't appear consistently as a new account problem or a portfolio problem or correlate to thick- or thin-filed identities, further complicating the issue. How does synthetic identity fraud impact me? As mentioned, when synthetic identities bust out, businesses are stuck footing the bill. Annual SIF (synthetic identity fraud) charge-offs in the United States alone could be as high as $11 billion. – Steven D’Alfonso, research director, IDC Financial Insights1 Unlike first- and third-party fraud, which deal with true identities and can be tracked back to a single person (or the criminal impersonating them), synthetic identities aren’t linked to an individual. This means that the tools used to identify those types of fraud won’t work on synthetics because there’s no victim to contact (as with third-party fraud), or real customer to contact in order to collect or pursue other remedies. Solving the synthetic identity fraud problem Preventing and detecting synthetic identities requires a multi-level solution that includes robust checkpoints throughout the customer lifecycle. During the application process, lenders must look beyond the credit report. By looking past the individual identity and analyzing its connections and relationships to other individuals and characteristics, lenders can better detect anomalies to pinpoint false identities. Consistent portfolio review is also necessary. This is best done using a risk management system that continuously monitors for all types of fraudulent activities across multiple use cases and channels. A layered approach can help prevent and detect fraud while still optimizing the customer experience. With the right tools, data, and analytics, fraud prevention can teach you more about your customers, improving your relationships with them and creating opportunities for growth while minimizing fraud losses. To wrap up this series, I’ll explore account takeover fraud and how the correct strategy can help you manage all four types of fraud while still optimizing the customer experience. To learn more about the impact of synthetic identities, download our “Preventing Synthetic Identity Fraud” white paper and call us to learn more about innovative solutions you can use to detect and prevent fraud. Contact us Download whitepaper 1Synthetic Identity Fraud Update: Effects of COVID-19 and a Potential Cure from Experian, IDC Financial Insights, July 2020

Enterprise Security Magazine recently named Experian a Top 10 Fraud and Breach Protection Solutions Provider for 2020. Accelerating trends in the digital economy--stemming from stay-at-home orders and rapid increases in e-commerce and government funding--have created an attractive environment for fraudsters. At the same time, there’s been an uptick in the amount of personally identifiable information (PII) available on the dark web. This combination makes innovative fraud and breach solutions more crucial than ever. Enterprise Security Magazine met with Kathleen Peters, Experian’s Chief Innovation Officer, and Michael Bruemmer, Vice President of Global Data Breach and Consumer Protection, to discuss COVID-19 digital trends, the need for robust fraud protection, and how Experian’s end-to-end breach protection services help businesses protect consumers from fraud. According to the magazine, “With Experian’s best in class analytics, clients can rapidly respond to ever-changing environments by utilizing offerings such as CrossCore® and Sure ProfileTM to identify and prevent fraud.” In addition to our commitment to develop new products to combat the rising threat of fraud, Experian is focused on helping businesses minimize the consequences of a data breach. The magazine noted that, “To serve as a one-stop-shop for data breach protection, Experian offers a wide range of auxiliary services such as incident management, data breach notification, identity protection, and call center support.” We are continuously working to create and integrate innovative and robust solutions to prevent and manage different types of data breaches and fraud. Read the full article Contact us

In the wake of unprecedented unemployment fraud since the start of COVID-19, Experian announced it was selected as the exclusive partner for identity and fraud verification for the Unemployment Insurance (UI) Integrity Center’s centralized Identity Verification (IDV) capability. IDV is available to state agencies at no cost through UI Integrity Center, which is operated by the National Association of Workforce Agencies (NASWA) in partnership with the U.S. Department of Labor. With the Federal Bureau of Investigations (FBI) reporting a spike in fraudulent unemployment insurance claims complaints related to COVID-19, it’s more important than ever for state agencies to use innovative solutions to verify identities that are applying for unemployment insurance to protect consumers. If improper unemployment insurance payments are made to fraudsters, the efforts of the CARES Act could be largely wasted. The IDV capability leverages Experian’s Precise IDTM to provide a centralized identity verification and proofing solution. Precise ID combines identity analytics with advanced fraud risk models to distinguish various types of fraud, which can help state agencies maximize time and resources. When state agencies submit claims, the IDV solution will return ID theft scoring and associated cause codes, enabling them to assess whether a claim may be fraudulent. “Due to the COVID-19 health crisis, unemployment is high, with over roughly 60 million Americans filing for unemployment since March,” said Robert Boxberger, president of Experian’s Decision Analytics in North America. “At Experian, we’re proud to have a strong culture dedicated to continuous innovation that helps protect consumers’ financial health. We’re taking that same consumer focus and helping make the unemployment insurance application process more efficient and safer for constituents.” The Integrity Data Hub (IDH) is a robust, multi-state data system that contains a continuously expanding set of sources to provide advanced cross-matching and analytic capabilities to states. It is designed to be easily implemented by any state Unemployment Insurance agency, regardless of claim volume, technology, or access to internal resources. The IDH was designed and built using the latest National Institute of Standards and Technology IT security standards, including the use of asymmetric encryption and other techniques to ensure the security of sensitive data. “We’re excited to partner with Experian and utilize its Precise ID solution to assist states in mitigating fraud during these unprecedented times,” said Scott Sanders, NASWA Executive Director. “States are finding this to be a very valuable tool and we are pleased that we can offer this solution to states through our partnership with the U.S. Department of Labor.” Read Press Release Learn More About Precise ID

Synthetic identity fraud, otherwise known as SID fraud, is reportedly the fastest-growing type of financial crime. One reason for its rapid growth is the fact that it’s so hard to detect, and thus prevent. This allows the SIDs to embed within business portfolios, building up lines of credit to run up charges or take large loans before “busting out” or disappearing with the funds. In Experian’s recent perspective paper, Preventing synthetic identity fraud, we explore how SID differs from other types of fraud, and the unique steps required to prevent it. The paper also examines the financial risks of SID, including: $15,000 is the average charge-off balance per SID attack Up to 15% of credit card losses are due to SID 18% - the increase in global card losses every year since 2013 SID is unlike any other type of fraud and standard fraud protection isn’t sufficient. Download the paper to learn more about Experian’s new toolset in the fight against SID. Download the paper

The CU Times recently reported on a nationwide synthetic identity fraud ring impacting several major credit unions and banks. Investigators for the Federal and New York governments charged 13 people and three businesses in connection to the nationwide scheme. The members of the crime ring were able to fraudulently obtain more than $1 million in loans and credit cards from 10 credit unions and nine banks. Synthetic Identity Fraud Can’t Be Ignored Fraud was on an upward trend before the pandemic and does not show signs of slowing. Opportunistic criminals have taken advantage of the shift to digital interactions, loosening of some controls in online transactions, and the desire of financial institutions to maintain their portfolios – seeking new ways to perpetrate fraud. At the onset of the COVID-19 pandemic, many financial institutions shifted their attention from existing plans for the year. In some cases they deprioritized plans to review and revise their fraud prevention strategy. Over the last several months, the focus swung to moving processes online, maintaining portfolios, easing customer friction, and dealing with IT resource constraints. While these shifts made sense due to rapidly changing conditions, they may have created a more enticing environment for fraudsters. This recent synthetic identity fraud ring was in place long before COVID-19. That said, it still highlights the need to have a prevention and detection plan in place. Financial institutions want to maintain their portfolios and their customer or member experience. However, they can’t afford to table fraud plans in the meantime. “72% of FI executives surveyed believe synthetic identity fraud to be more challenging than identity theft. This is due to the fact that it is harder to detect—either crime rings nurture accounts for months or years before busting out with six-figure losses, or they are misconstrued as credit losses, and valuable agent time is spent trying to collect from someone who doesn’t exist,” says Julie Conroy, Research Director at Aite Group. Prevention and Detection Putting the fraud strategy discussion on hold—even in the short term—could open up a financial institution to potential risk at time when cost control and portfolio maintenance are watch words. Canny fraudsters are on the lookout for financial institutions with fewer protections. Waiting to implement or update a fraud strategy could open a business up to increased fraud losses. Now is the time to review your synthetic identity fraud prevention and detection strategies, and Experian can help. Our innovative new tool in the fight against synthetic identity fraud helps financial institutions stop fraudsters at the door. Learn more

The COVID-19 pandemic created a global shift in the volume of online activity and experiences over the past several months. Not only are consumers increasing their usage of mobile and digital channels to bank, shop, work and socialize — and anticipating more of the same in the coming months — they’re closely watching how businesses respond to their needs. Between late June and early July of this year, Experian surveyed 3,000 consumers and 900 businesses to explore the shifts in consumer behavior and business strategy pre- and post-COVID-19. More than half of businesses surveyed believe their operational processes have mostly or completely recovered since COVID-19 began. However, many consumers fear that a second wave of COVID-19 will further deplete their already strained finances. They are looking to businesses for reassurance as they shift their behaviors by: Reducing discretionary spending Building up emergency savings Tapping into financial reserves Increasing online spending Moving forward, businesses are focusing on short-term investments in security, managing credit risk with artificial intelligence, and increasing online customer engagement. Download the full report to get all of the insights into global business and consumer needs and priorities and keep visiting the Insights blog in the coming weeks for a deeper dive into US-specific findings. Download the report

Experian’s Chris Ryan and Bobbie Paul recently re-joined David Mattei from Aite to discuss how emerging fraud trends and changes in consumer behavior will have long-term impacts on businesses. Chris, Bobbie, and David have combined experience of more than 60 years in the world of fraud prevention. In this discussion, they bring that experience to bear as they review how businesses should revise their long-term fraud strategy in response to COVID-19 and the subsequent economic shifts, including: The requirements to authenticate a digital customer Businesses’ technology challenges Differentiating between first party and third party fraud The importance of businesses’ technology investment How to build a roadmap for the next 90 days and beyond Experian · Make Your Fraud Plan Recession-Ready: Your 90 Day and Beyond Plan

Every few months we hear in the news about a fraud ring that has been busted here in the U.S. or in another part of the world. In May, I read about a fraud ring based in Georgia and Louisiana that bought 13,000 stolen identities of children who were on the Louisiana Medicaid program and billed the government for services not rendered. This group defrauded the Medicaid program of more than $500,000. This is just one of many stories that we hear about fraud rings, and given the rapidly changing economic environment, now is the time for businesses to think about how to protect against fraud rings. There are a number of challenges that organizations may have when it comes to sharing trends and collaborations, understanding the ways to tie fraud rings together, creating treatments for identifying fraud rings and ways to store and catalogue fraud ring experiences so they can be easily recognized. The trouble with identifying fraud rings It’s important to understand the challenges that organizations have because they see the fraud rings through their own internal lens. Here are a few of the top things businesses should work on: Think like a fraudster. This will help businesses become more creative in their approach to fraud prevention. Facilitate internal collaboration. Share with in-organization partners. Sometimes this can be difficult due to organizational structure. Promote external collaboration. Intel-sharing groups are a great way for businesses to network within their industries and learn about the fraud that others are seeing. An organization that I’ve worked with in the past is the National Cyber Forensic and Training Alliance (NCFTA). Putting the pieces together How do businesses identify a fraud ring? There are three steps to get started. The first is reviewing and understanding the data. Fraudsters are lazy and want to replicate the process over and over again, and because of this there is always some piece of information that is repeated. It could be a name, an email address, device fingerprint, or similar. The second step is tying the fraud ring together. This is done by creating rules to help identify the trends. Having rules in place to identify fraud rings allows businesses to easily pull stats together for their leadership. Lastly, applying an acronym or name to the particular fraud ring and adding comments to the cases associated with a particular ring will help with post-investigation analysis. Learning from the past Before I became a consultant, I remember identifying a fraud ring that was submitting events with the same language pack and where the device fingerprint was staying consistent. Those events were being referred out for review and marked with the same note. At a post-mortem review, I was able to talk to the fraud ring we had seen, and it was easy to pull all events associated with this fraud ring because my team had marked the events with the same comments. Another fraud ring example happened a few years ago. A client called me and said that they were under a fraud attack and this fraud ring was rotating the email handle. I reviewed the data and came up with a rule to catch this activity. Fraud rings will use email handle rotation to help them keep track of accounts that are opened or what emails they used in the past. By coupling the email handle rotation with an email verification service like Emailage, this insight could be very telling. I would assume that when fraud rings use email handle rotation these emails are new and have just been created. These are just a few of the many fraud rings that I’ve encountered over the course of my career and I’m sure there will be a lot more in the years to come. The best advice I can give to anyone that reads this post is to understand the data that you are reviewing, look for anomalies within the data, ask questions and test your theories by running queries on the data that you’re reviewing. I would love to hear about the different fraud rings that you’ve encountered over your career. Stay safe. Contact us

Experian’s own Chris Ryan and Bobbie Paul recently joined David Mattei from Aite to discuss the latest research and insights into emerging fraud schemes and how businesses can combat them in light of COVID-19 and the resulting economic changes. Between them, Chris, Bobbie, and David have more than 60 years of experience in the world of fraud prevention. Listen in as they discuss how businesses can shape their fraud prevention plan in the short term, including: The impacts of the health crisis and physical distancing The rise of e-commerce and consumer digital engagement Changes in criminal activity Fraud attack vectors 2020 fraud loss projections Critical next steps for the 30-60 day time frame Experian · Make Your Fraud Plan Recession-Ready: 2020 Fraud Trends

The COVID-19 pandemic and resulting rush to transition to a remote lifestyle made it clear that many businesses need a refreshed digital authentication and fraud prevention strategy that includes an investment in technology and provides consumer assurance. This is particularly important when it comes to identity, as many of the standard in-person verification methods and tools are currently unavailable. The meaning of identity is growing and shifting Technology trends are intersecting with social trends to create heightened awareness, and a whole new public conversation has emerged around customer trust and privacy. Attitudes and ideas are changing—even to the point of what we mean by “identity.” An identity is no longer just a name, date of birth, and SSN. Now, there are digital manifestations everywhere you look: screen names, email addresses, mobile phone numbers, device identifiers, and the other “exhaust” we leave behind as we travel the internet. This leads to concerns about what an identity is, who owns it, and who manages and protects it. Businesses have to be able to prove to their ability to protect their customers’ identities through investment in technology and a robust fraud strategy. Consumer attitudes are changing Several years ago, consumers were excited by all the new digital capabilities and the speed, ease, and convenience they provided. Last year, Experian found that consumers still wanted those things, with 70% willing to provide more information to businesses if there was a perceived benefit. However, they also wanted more security in the balance. In Experian’s most recent Global Identity and Fraud Report, we found that 74% of consumers say that security is the most important factor when deciding to engage with a business. Consumers are particularly more tolerant of friction during the enrollment process—as a means of building trust. But, when they return to the app or website, they want to be recognized. This means achieving a balance by using layered technologies, some of which are active and visible to the consumer, and some of which are invisibly working in the background to confirm the identity of returning consumers. Consumer attitudes vs. regulatory pressure The drivers behind the business changes are twofold: shifting consumer attitudes and regulatory changes. While regulations are becoming stricter on a national and global level, they’re not keeping pace with technology and social change. The digital world is evolving at a rapid pace, opening up more new ways for companies to collect information about consumers and use it to identify and verify, and also to target goods and services. With all of this data available, it’s important for businesses to use the tools in the market to help protect identity information. Next steps in technology The bottom line is, businesses can’t wait for regulations to dictate how best to protect information. Instead, they should be looking to technologies like physical and behavioral biometrics to help provide identity authentication and protection – layering those solutions with information from the user and from third parties to give a holistic consumer view. Businesses should adopt a platform approach for identity and fraud in order to be able to adapt quickly, whether to incorporate new kinds of technology or to prevent emerging types of fraud. By investing in technology now, even in the midst of the COVID-19 pandemic, businesses can build the flexibility needed to respond to future crises and help offset future fraud losses. In turn, those fraud-loss savings can then be used to help grow the business in the future. Learn more about Experian’s commitment to helping businesses maximize their investment in technology to safeguard against fraud. Learn more

To combat the growing threat of synthetic identity fraud, Experian recently announced the launch of Sure ProfileTM, a revolutionary change to the credit profile that gives lenders peace of mind with Experian’s commitment to share in losses that result from an identity we’ve assured. “Experian has always been a leader in combatting fraud, and with Sure Profile, we’re proud to deliver an industry-first fraud offering integrated into the credit profile that mitigates lender losses while protecting millions of consumers’ identities,” said Robert Boxberger, President of Decision Analytics, Experian North America. Synthetic identity fraud is expected to drive $48 billion in annual online payment fraud losses by 2023. Between opportunistic fraudsters and a lack of a unified definition for synthetic identity theft it can be nearly impossible to detect—and therefore prevent—this type of fraud. This breakthrough solution provides a composite history of a consumer’s identification, public record, and credit information and determines the risk of synthetic fraud associated with that consumer. It’s not just a fraud tool, it’s a comprehensive credit profile that utilizes premium data so lenders can make positive credit decisions. Sure Profile leverages the capabilities of the Experian Ascend Identity PlatformTM and uses Experian’s industry-leading data assets and data quality to drive advanced analytics that set a higher level of protection for lenders. It’s powered by newly-developed machine learning and AI models. And it offers a streamlined approach to define and detect synthetic identities early in the originations process. Most importantly, Sure Profile differentiates between real people and potentially risky applicants so lenders can increase application approvals with greater assurance and less risk. “Experian can confidently define and help detect synthetic fraud. That's why we can help stop it,” said Craig Boundy, CEO of Experian North America. “Experian stands behind our data with assurance given to our clients. It’s better for lenders and it’s better for consumers.” Sure Profile is a complement to our robust set of identity protection and fraud management capabilities, which are designed to address fraud and identity challenges including account openings, account takeovers, e-commerce fraud and more. This first-of-its kind profile is the future of underwriting and portfolio protection and it’s here now. Read press release Learn More About Sure Profile