Debt & Collections

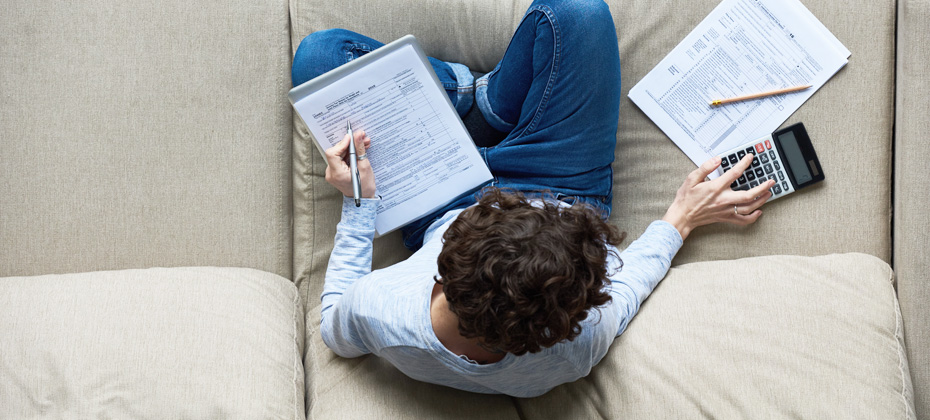

We’ve popped the bottles at midnight, now it’s time to burst the reality bubble. Countdown: t-minus less than 90 days until what is for many the dreaded April 15 tax deadline. Tax Season - Get Started Coupled with debt consolidation post-holidays, January is a harsh contrast to all the feasting and festivities of the holiday season. However, the tax season doesn’t necessarily have to be synonymous with doom and gloom – many Americans look forward to receiving a tax refund. And of those people expecting a tax refund, 35% of consumers said they would use it to pay down debt, according to the National Retail Federation. Lenders and financial institutions can help their consumers get off on the right financial foot for 2019 by helping them to pay down their debt. Here are 5 tools you need to have this tax season to make the most of your collections efforts: 1. Identify your target market – Tax Season Payment IndicatorTM Did you know the average tax refund in 2016 and 2017 was over $2,760, according to the IRS? Also, during the 2017 tax season, 45 million consumers paid at least $500 and 10% or more of a tradeline balance(s), according to Experian data. Tax Season Payment Indicator examines payment behavior over the past two years to determine whether a consumer has made a large payment to a tradeline balance – or balances – during tax season. 2. Keep up-to-date on consumer information – Clear ProfileTM Skip tracing just got easier. Narrow in on the right contact information for your past-due consumer using Clear Profile. Leveraging Clarity Service’s database, Clear Profile provides the most recent and historical demographic elements associated with your consumer’s previous applications including addresses, phone numbers, employers, emails and banks. 3. Know the right time to collect – Collection TriggersSM Take the guesswork out of how to manage your collections efforts. Track your accounts to notify you of a new contact information and changes that indicate your past-due consumers’ ability to pay. 4. Stay ahead of fraudsters – CrossCoreTM Fraudsters are everywhere, so protect your customers and your organization by monitoring your portfolio to keep fraudulent accounts from being opened. Still wondering how to get tax season ready? Get Your Collections Tax Season Ready

Ben Franklin was wrong. Death and taxes are not the only two constants in life. For many, debt makes a third. And where there is past-due debt, collections is not far from the conversation, if not included in the same breath. While the turn of the new year may mark some arduous work to be done – losing those holiday pounds, spring cleaning, balance transfers and tax filings – there’s also opportunity for lenders, collectors and consumers alike. Just as the spikes in retail trends are analogous with the holiday months, there’s an evident uptick in collections during tax season year after year. As such, successful lenders, financial institutions and collections agencies know that January, February and March are critical months to engage with past-due customers, specifically as they relate to the tax season. The average tax refund for 2016 and 2017 was $2,860 and $2,769 respectively, according to the IRS. And while some may assume that all consumers look at this money as an opportunity for a “treat yourself” splurge, 35% of consumers expecting a refund said they would use it to pay down debt, according to the National Retail Federation. Additionally, during the 2017 tax season, 45 million consumers paid at least $500 and 10% or more of a tradeline balance(s), according to Experian data. So, if past-due consumers want to pay down debt, and the ultimate goal of collections is to recoup over-due funds, and first quarter collections growth appears to be driven by tax refunds, how do we make the connection? Think of the scene from Jerry Maguire – “Help me, help you!” Help consumers help themselves. Experian’s new Tax Season Payment IndicatorTM examines payment behavior over the past two years to determine whether a consumer has made a large payment to a tradeline balance – or balances – during tax season. “Millions of consumers used their tax refunds to pay down debt and many plan to do it again,” said Denise McKendall, Product Manager. “Collectors that leverage previous tax season payment behavior to identify and strategically engage with this group will benefit the most from the tax refund season.” Engaging this information can be like having a collections crystal ball. Targeting consumers that are likely to use their refund to pay down debt can influence messaging, campaign refinement and the timeliness of your touchpoints, resulting in greater collections ROI. This means as the year closes out and planning begins for 2019, collections prioritization strategy is key. And those conversations should be taking place now. Are you tax season ready? Learn More About Tax Season Payment Indicator

In the credit game, the space is deep and diverse. From super prime to prime to subprime consumers, there is much to be learned about how different segments are utilizing credit and navigating the financial services arena. With 78 percent of full-time workers saying they live paycheck-to-paycheck and 71 percent of U.S. workers responding that they live in debt, it is not surprising a sudden life event can plunge a solid credit consumer from prime to subprime within months. Think lost job, divorce or unexpected medical bill. This population is not going away, and they are seeking ways to make ends meet and obtain finances for needs big and small. In many instances, alternative credit data can shed a light on new opportunities for traditional lenders, fintech players and those in the alternative financial space when servicing this specific consumer segment. In a new study, Clarity analyzed the trends and financial behavior of subprime loan users by looking at application and loan data in Clarity’s database, as well as overlaying VantageScore® credit score insights from Experian from 2013 to 2017. Clarity conducted this subprime trends report last year, but this is the first time it factored in VantageScore® credit score data, providing a different lens as to where consumers fall within the credit score tiers. Among the study highlights: Storefront single pay loan customers are becoming more comfortable with applying for online loans, with a growing percentage seeking installment products. For the first time in five years, online single pay lending (payday) saw a reduction in total credit utilization per customer. Online installment, on the other hand, saw an increase. While the number of online installment loans increased by 12 percent and the number of borrowers by only 9 percent, the dollar value grew by 30 percent. Online installment lenders had the greatest percentage increase in average loan amount. California and Texas remain the most significant markets for online lenders, ranking first and second for five years in a row due to population size. There has also been growth in the Midwest. The in-depth report additionally delves into demographics, indicators of financial stability among the subprime market and comparisons between storefront and online product use and performance. “Every year, there are more financial lenders and products emerging to serve this population,” said Andy Sheehan, president of Clarity Services. “It’s important to understand the trends and data associated with these individuals and how they are maneuvering throughout the credit spectrum. As we know, it is often not a linear journey.” The inclusion of the VantageScore® credit score showcased additional findings around prime versus subprime financial behaviors and looks at generational trends. Access Full Report

There are lots of reasons why people miss a bill payment. Unfortunately, the approaches for collecting those late payments tend to follow a one-size-fits-all approach. For example, a customer takes a long vacation and forgets to pay his credit card bill before he leaves. When he gets home ten days later he already has five phone calls and two official notices from the collections department. And the calls continue for the next few days until he has an opportunity to call them back to take care of the situation. How does this customer feel? Frustrated? Annoyed? Under-valued? The current collections process is outdated, especially in a world where personalized and relevant communications are becoming the norm. The collections process is driven by the measurement of delinquency and loss. Rarely does it consider the broader customer profile. Too often, this narrow view leads to one-size-fits all collections strategies and overly aggressive processes. Getting debt collection right is about more than the money. It needs to be about the customer. It’s about knowing the difference between a customer who has simply forgotten to make a payment or someone dealing with financial hardship. We recently released a paper on the collections process, looking at how common it is for overly aggressive collections to lead to account closures and erosion of customer lifetime value. In fact, we found 3 percent of 30-day delinquencies in card portfolios closed their accounts after paying their balance in full. Seventy-five percent of those closures came with the payment to bring the account current and the remaining 25 percent closed the account within the following 60 days. Our analysis also showed that people with the lowest balances and the lowest amount past-due had the highest incidence of paying off their debt and closing their accounts. That means that by being too aggressive over a fairly low dollar amount, you can damage the relationship with a customer who could bring a lifetime of more business. We also used our Mosaic® lifestyle segmentation system to do a deeper look into who was more likely to close their accounts. We found the likelihood to close accounts was four times higher in the young, urban, affluent population than it was with others. This particular segment usually has the greatest potential for lifetime value and are the hardest to attract. It seems counterproductive to let overly aggressive and perhaps unnecessary, debt collection end the relationship. However, if we become smarter about the collections process, it could be possible to not only keep the customer, but also strengthen the relationship. Consider this, the customer on that long vacation receives an email that says, “Hey we noticed you forgot to make your last payment. Can you email us back the reason why and when we should expect it?” This creates an opportunity to build the relationship with that customer and get a commitment to settle the payment by a particular date. Ten days later when he gets back from vacation, he receives a reminder to make the payment and takes care of it. Instead of feeling frustrated, annoyed or undervalued, the customer has a positive experience and continues doing business with a company who is focused on building relationships vs. simply collecting money. There is a real opportunity to take best practices around customer experience from earlier stages of the customer lifecycle and apply them to the collections stage. Sure, some situations may require a more aggressive approach, for others, the idea of an email and the option to log on to a virtual platform to handle the debt on their own terms is the preferred approach. Some customers may not need options other than a little more time to pay on their own terms. It comes down to knowing your customer and applying the insights we can uncover from data to handle debt collection. This will allow us to improve the customer experience and strengthen customer life-time value.

“Who Moved My Cheese?” Perhaps you've heard of this popular book, released in 1998. If you haven't, it's a quick read and one that describes four fictional characters - two mice and two "little people" - on their quest to hunt for cheese. On their journey, they have to assess their routines and consider change - that word that makes so many of us uncomfortable. I bring this up because it is no secret that the consumer has changed dramatically over the years. Technology, the need for personalization, the demand for speed. Yes, the consumer has changed for sure, and everyone seems to recognize this but collections professionals. Look at any financial institution and you will hear and see leaders talking about and executing on digital acquisition and account management strategies. After all, digital is the medium that consumers desire when interacting with their financial service providers. Marketers know this and most have adapted, but when it comes to collections, the industry seems to be fixated on utilizing the tactics of the past. Today, collectors largely rely on calling consumers and sending out dunning letters. Right Party Contact rates continue to decline, and with 50 percent of consumers lacking land lines, the contact rates are only going to get worse. I say all this because if you want to see success, you must change. Offering your past-due customers a digital experience will not only increase your collections performance and recoveries, but simultaneously improve your customer experience and reduce costs. This is a huge opportunity if collectors would just embrace a digital collections strategy. And let me note that having a payment portal is not a digital collections strategy. If that was the case, digital marketers would be done with just a simple website, and then they can wish their consumers will land on the site. A digital collections experience is much more. Why stay stuck in the past? Change is good, let someone else look for that old cheese.

As soon as the holiday decorations are packed away and Americans reign in the New Year, the advertisements shift to two of our favorite themes – weight loss and taxes. No wonder the “blues” kick in during February. While taxes aren’t due until April 17, the months of January, February and March have consumers prepping to file. Coincidentally, it is also a big season for lenders to collect after the high-spending months of October through December. “Knowing which of your customers may receive a refund is critical,” said Colleen Rose, an Experian product manager specializing in the collections industry. “This information can help lenders create a strategy to capitalize on this important segment during the compressed collections window.” The industry has become more familiar with trended data and its ability to predict how consumers are faring on the credit score slider, but many don’t know that it has also proven popular in identifying people who may get a tax refund, and who is likely to use a refund to pay down delinquent balances. The past two tax seasons are evaluated to provide a complete picture of a customer’s behavior during tax refund season. Balance, credit limit and other historical fields are incorporated with tradeline-level data to determine who paid down their delinquent balances during this time. According to the IRS, in fiscal year 2016, the average individual income tax refund was about $3,050, so it’s a prime time for consumers to come into some unexpected cash to either pay down debt or spend. It’s estimated that 35% of consumers who get a refund will pay down debt. “Using Experian’s trended data attributes, we’ve identified past-due customers who paid down a delinquent tradeline balance by at least 10% and made a large payment during tax season,” said Rose. “With these specific attributes, we can help clients target a very desirable population during the critical collections months, helping them to refine their campaigns and create offers geared toward this population.” Anticipating who is likely to receive a refund and use it to pay down debt can influence how collections departments develop their messaging, call outreach and mailings. And for consumers who owe multiple debts, these well-timed touchpoints and messages could influence who they pay back first. The collectors with the best data, once again win, with trended data providing the secret sauce for predictions. ‘Tis the season for taxes.

For most businesses, the customer experience is at the heart of every strategy. Debt collection shouldn’t be different. Here’s why: 21% of visits to an online debt recovery system were made outside the traditional working hours of 8 a.m. to 8 p.m. Of the consumers who committed to a repayment plan, only 56% did so in a single visit. PricewaterhouseCoopers reported that 46% of consumers use only digital channels to conduct banking, avoiding traditional offline channels. Conversely, data collected by Gallup between 2013 and 2016 showed that 48% of American banking customers would only consider using a bank that offered physical branches. The debt collection process is an often-overlooked opportunity to build customer relationships and loyalty. Leverage data and technology to replace outdated approaches, minimize charge-offs and create environments that value each customer. Learn more>

It’s no secret. Consumers engage and interact with brands through a variety of channels, including email, direct mail, websites and mobile. And since most organizations work to keep the consumer experience at the core, they tend to invest in an omnichannel approach that caters to the consumer’s preferences. The lone exception may be during the collections process. Often, once an account falls behind on payment, the consumer experience falls behind with it. But should it? While many banks and financial institutions view the collections process merely as an opportunity to collect outstanding debt, the potential is much more. If treated effectively, the collections process can present an opportunity to develop a positive customer relationship that builds loyalty over time. If handled poorly, the collections process could cost an organization a number of lifetime customers. To correct this, banks and financial institutions need to implement the same omnichannel approach in the collections process as they do with every other consumer interaction. Collections can no longer be treated as a linear process that leads from one channel to the next. There needs to be a more personalized touch — communicating with consumers through preferred channels, contacting them at the most opportune times. Sound complex? Sure. But consider a recent Experian analysis that invited consumers to establish a nonthreatening dialogue with an online debt recovery system. The analysis revealed 21 percent of visits to an organization’s website were outside the traditional working hours of 8 a.m. to 8 p.m. Furthermore, of the consumers who committed to a repayment plan, only 56 percent did so in a single visit. Each consumer is different. So is each situation. And banks and financial institutions need to acknowledge those differences. Luckily, technology can address the complexities of an omnichannel and personalized approach. Platforms such as Experian’s PowerCurve® Collections enable banks and financial institutions to simplify the collections process for both the consumer and the organization. By treating the collections process the same as any other stage in the consumer journey, organizations have an opportunity to build a relationship. And to do so, banks and financial institutions need to leverage the data and technology at their disposal. If they do so appropriately, they’ll minimize their charge-offs and also create a lifetime customer. To learn more about leveraging the collections process to build customer loyalty, download our white paper Getting in front of the shift to omnichannel collections.

The collections space has been migrating from traditional mail and outbound calls to electronic payment portals, digital collections and virtual negotiators. Now that collectors have had time to test virtual collections, we’ve collected some data points. Here are a few: On average, 52% of consumers who visit a digital site will proceed to a payment schedule if the right offer is made. 21% of the visits were outside the core hours of 8 a.m. to 8 p.m., an indication that traditional business hours don’t always work. Of the consumers who committed to a payment plan, only 56% did it in a single visit. The remaining 44% did so mostly later that day or on a subsequent day. As more financial institutions test this new virtual approach, we anticipate customer satisfaction and resolutions will continue to climb. Get your debt collections right>

Everyone loves a story. Correction, everyone loves a GOOD story. A customer journey map is a fantastic tool to help you understand your customer’s story from their perspective. Perspective being the operative word. This is not your perspective on what YOU think your customer wants. This is your CUSTOMER’S perspective based on actual customer feedback – and you need to understand where they are from those initial prospecting and acquisition phases all the way through collections (if needed). Communication channels have expanded from letters and phone calls to landlines, SMS, chat, chat bots, voicemail drops, email, social media and virtual negotiation. When you create a customer journey map, you will understand what channel makes sense for your customer, what messages will resonate, and when your customer expects to hear from you. While it may sound daunting, journey mapping is not a complicated process. The first step is to simply look at each opportunity where the customer interacts with your organization. A best practice is to include every department that interacts with the customer in some way, shape or form. When looking at those touchpoints, it is important to drill down into behavior history (why is the customer interacting), sociodemographic data (what do you know about this customer), and customer contact patterns (Is the customer calling in? Emailing? Tweeting?). Then, look at your customer’s experience with each interaction. Again, from the customer’s viewpoint: Was it easy to get in touch with you? Was the issue resolved or must the customer call back? Was the customer able to direct the communication channel or did you impose the method? Did you offer self-serve options to the right population? Did you deliver an email to someone who wanted an email? Do you know who prefers to self-serve and who prefers conversation with an agent, not an IVR? Once these two points are defined: when the customer interacts and the customer experience with each interaction, the next step is simply refining your process. Once you have established your baseline (right channel, right message, right time for each customer), you need to continually reassess your decisions. Having a system in place that allows you to track and measure the success of your communication campaigns and refine the method based on real-time feedback is essential. A system that imports attribute – both risk and demographic – and tracks communication preferences and campaign success will make for a seamless deployment of an omnichannel strategy. Once deployed, your customer’s experience with your company will be transformed and they will move from a satisfied customer to one that is a fan and an advocate of your brand.

It should come as no surprise that the process of trying to collect on past-due accounts has been evolving. We’ve seen the migration from traditional mail and outbound calls, to offering an electronic payment portal, to digital collections and virtual negotiators. Being able to get consumers who have past-due debt on the phone to discuss payments is almost impossible. In fact, a recent informal survey divulged a success rate of a 15% contact rate to be considered the best by several first-party collectors; most reported contact rates in the 8%-range. One can only imagine what it must be like for collection agencies and debt buyers. Perhaps, inviting the consumer to establish a non-threatening dialog with an online system can be a better approach? Now that collectors have had time to test virtual collections, we’ve collected some data points. Conversion rates, revisits, and time of day An analysis of several clients found that on average 52% of consumers that visit a digital site will proceed to a payment schedule if the right offer is made. 21% of the visits were outside the core hours of 8 a.m. to 8 p.m., an indication that consumers were taking advantage of the flexibility of reaching out at any time of the day or night to explore their payment and settlement options. The traditional business hours don’t always work. Here is where it really gets interesting, and invites a clear comparison to the traditional phone calls that collectors make trying to get the consumer to commit to a payment plan on the line. Of the consumers that committed to a payment plan, only 56% did it in a single visit. The remaining 44% that committed to payments did so mostly later that day, or on a subsequent day. This strongly suggests they either took time to check their financial status, or perhaps asked a friend or family to help with the payment. In other words, rather than refusing to agree to an instantaneous agreement pressured by a collector, the consumer took time to reflect and decide what was the best course of action to settle the amount due. On a similar note, the attrition rate of “Promises to Pay” were 24% lower using online digital solutions versus the traditional collector phone call. This would be consistent with more time to agree to a payment plan that could be met, rather than weakly agreeing to a collector phone call just to get the collector off the phone. Another possible reason for a lower attrition rate may be that a well-defined digital collection solution can send out reminders to consumers via email or text in advance of the next scheduled payment, so that the consumer can be reminded to have the funds available when the next payment hits their account. For accounts where settlement offers are part of the mix, a higher percentage of balances is being resolved versus the collection floor. In fact, the average payment improvement is 12% over what collectors tend to get on the collections floor. The reason for this significant change is unclear, but the suspicion is that a digital collection solution will negotiate stronger than a collector, who is often moving to the bottom of an acceptable range too soon. What's next? Further assessing the consumer’s needs and capabilities during the negotiation session will undoubtedly be a theme going forward. Logical next steps will include a “behind-the-scenes” look at the consumer’s entire credit picture to help the creditor craft an optimal settlement amount that both the consumer can meet, and at the same time optimizes recovery. Potential impact to credit scores will also come into the picture. Depending on where the consumer and his past-due debt is in the credit lifecycle, being able to reasonably forecast the negative impact of a missed payment can act as an additional argument for making a past-due or delinquent payment now. As more financial institutions test this new virtual approach, we anticipate customer satisfaction and resolutions will continue to climb.

We regularly hear from clients that charge-offs are increasing and they’re struggling to keep up with the credit loss. Many clients use the same debt collection strategy they’ve used for years – when businesses or consumers can’t repay a loan, the creditor or collection agency aggressively contacts them via phone or mail to obtain repayment – never considering the customer experience for the debtor. Our data shows that consumers accounted for $37.24 billion in bankcard charge-offs in Q2 2017, a 17.1 percent increase from Q2 2016. Absorbing credit losses at such a high rate can impact the sustainability of the institution. Clearly the process could use some adjusting. Traditionally, debt collection has been solely about the money. The priority was ensuring that as much of the outstanding debt as possible was repaid. But collecting needs to be about more than that. It also should focus on the customer and his or her individual situation. When it comes to debt collection, customers should not all be treated the same way. I recently shared some tips in Credit Union Business Magazine about how to actively engage and collect from members. The same holds true for other financial institutions – they need to know the difference between a customer who has simply forgotten to make a payment and one who is dealing with financial hardship. As an example, if a person is current on his or her mortgage payment but has slipped behind on his or her credit card payment, that doesn’t necessarily signify financial hardship. It’s an opportunity to work with the customer to manage the debt and get back to current. Modern financial institutions build acquisition and customer management strategies targeted at individuals, so why should the collection process be any different? The challenge is keeping the customer at the center while also managing against potential increases in delinquencies. This holistic approach may be slightly more complex, but technology and analytics will simplify the process and bring about a more engaging experience for customers. The Power of Data and Technology Instead of relying on the same outdated collections approach – which results in uncomfortable exchanges on the phone that don’t ensure repayment –leverage data to your advantage. The data and technology exists to help you make more informed decisions, such as: What’s the most effective communication channel to reach the defaulting customer? When should you contact him or her? How often? The best course of action could be high-touch outreach, but sometimes doing nothing is the right approach. It all depends on the situation. Data and analytics can help uncover which customers are most likely to pay on their own and those who may need a little more help, allowing you to adjust your treatment strategy accordingly. By catering to the preferences of the customer, there’s a greater chance for a positive experience on both sides. The results: less charge-off debt, higher customer satisfaction and a stronger relationship. Explore the Digital Age In 2016, 36 million Americans made some form of mobile payment—paying a bill, purchasing something online, or paying for fast food, or making a Mobile Wallet purchase at a retailer. By 2020, nearly 184 million consumers will have done so, according to Aite. Consumers expect and deserve convenience. In the digital world, financial institutions have an opportunity to provide that expectation and then some. Imagine a customer being able to negotiate and manage his or her past-due account virtually, in the privacy of his or her own home, when it’s most convenient, to set their payment dates and terms. Luckily, the technology exists to make this vision a reality. Customers, not money, need to be at the heart of every debt collections strategy. Gone are the days of mass phone calls to debtors. That strategy made consumers unhappy, embarrassed and resentful. Successful debt collection comes down to a basic philosophy: Treat customers and his or her unique situation individually rather than as a portfolio profile. The creditors who live by that philosophy have an opportunity to reap the rewards on the back-end.

School is nearly back in session. You know what that means? The next wave of college students is taking out their first student loans. It’s a milestone moment – and likely the first trade on the credit file for many of these individuals. According to the College Board, the average cost of tuition and fees for the 2016–2017 school year was $33,480 at private colleges, $9,650 for state residents at public colleges, and $24,930 for out-of-state residents attending public universities. So really, regardless of where students go, the cost of a college education is big. In fact, from January 2006 to July 2016, the Consumer Price Index for college tuition and fees increased 63 percent. So, unless mom and dad did a brilliant job saving, chances are many of today’s students will take on at least some debt to foot the college bill. But it’s not just the young who are consumed by student loan debt. In Experian’s latest State of Student Lending report, we dive into how the $1.4 trillion in student loan debt for Americans is impacting all generations in regards to credit scores, debt load and delinquencies. The document additionally looks at geographical trends, noting which states have the most consumers with student loan debt and which ones have the least. Overall, we discovered 13.4% of U.S. consumers have one or more student loan balances on their credit file with an average total balance of $34k. Additionally, these consumers have an average of 3.7 student loans with 1.2 student loans in deferment. The average VantageScore® credit score for student loan carriers is 650. As we looked across the generations, every group – from the Silents (age 70+) to Gen Z (oldest are between 18 to 20) had some student loan debt. While we can make assumptions that the Silents and Boomers are likely taking out these loans to support the educational pursuits of their children and grandchildren, it can be mixed for Gen X, who might still be paying off their own loans and/or supporting their own kids. Gen X members also reported the largest average student loan total balance at $39,802. Gen Z, the newest members to the credit file, have just started to attend college, thus their generation has the largest percent of student loan balances in deferment at 77%. Their average student loan total balance is also the lowest of all generations at $11,830, but that is to be expected given their young ages. In regards to geographical trends, the Northern states tended to sport the highest average student loan total balances, with consumers in Washington D.C. winning that race with $52.5k. Southern states, on the other hand, reported higher percentages of consumers with student loan balances 90+ days past due. South Carolina, Louisiana, Mississippi, Arkansas and Texas held the top spots in the delinquency category. Access the complete State of Student Lending report. Data from this report is representative of student loan data on file as of June 2017.

The economic expansion just passed the eight-year mark, and consumer credit defaults across mortgages, bankcards and auto loans are at pre–financial crisis levels. More specifically: The first-mortgage default rate dropped 4 basis points from May to 0.60%. The bankcard default rate experienced its first drop in 9 months, with a decrease of 4 basis points bringing it to 3.49%. Auto loan defaults decreased 3 basis points from the previous month to 0.82%. With inflation at 1% to 2%, debt service levels close to record lows, and disposable income increasing and supporting spending growth, consumers are in good financial shape nationally. Lenders should take this opportunity to review and adjust their acquisition strategies accordingly. Can your originations platform capitalize on this?

Create a better consumer experience during the debt collection process When most people think about debt collection, unpleasant images may come to mind, like relentless phone calls or collections notices. Whatever the case may be, the collections process often ends in a less than desirable experience for consumers. And, quite frankly, it needs to change. Steve Platt, Experian’s Group President of Decision Analytics, recently spoke with American Banker regarding how banks and other financial institutions can create a better consumer experience during the debt collection process. While balancing consumer needs and managing rising delinquencies can be a complex challenge, Steve conveyed that the technology and analytics exist to simplify the process. As an industry, we’re at a point where customer acquisition costs far exceed the costs to nurture existing customers through the entire life-cycle - from application to repayment. So, suffice to say, lenders need to rethink how they engage and communicate with their customers. Technology to the rescue Luckily, we live in an era where troves and troves of data are made available every day. We just need to help lenders leverage it to its fullest extent. For example, the right data and technology can help answer questions, such as: What’s the most effective communication channel to reach a customer? When should you contact them? How often? There isn’t a one-size-fits-all approach to debt collection. Each customer is different. Each has their own unique situation. Effective debt collection is about knowing the difference between a customer who has simply forgotten to pay and those who may be struggling financially, and communicating with them accordingly. Go digital Part of knowing how to engage consumers is also understanding we live in a digital world. We perform many of our daily tasks through our mobile devices, desktops or tablets. So, it would make sense for lenders to help their customers manage their past-due accounts virtually. Imagine being able to negotiate payment dates and terms from the privacy of your own home. It just so happens that technology can make this a reality. At the end of the day, the customer needs to be at the heart of the collections strategy. Each customer needs to be communicated with on a case-by-case basis depending on their unique circumstances. The resources exist to make customers feel like individuals, rather than numbers in a spreadsheet. And the lenders that appeal to the customer’s experience will see lower charge-offs and higher customer retention.