Colorado has a great deal to offer first-time homebuyers (FTHBs). While the Denver area attracts many people with its combination of outdoor recreation, culture, and economic opportunities, other parts of Colorado are worthy of attention as well. Take Colorado Springs for example – it ranks third among best places to live in the U.S. when considering lifestyle, the job market, and overall popularity.1

Overview of the Colorado FTHB market

Colorado accounts for 2.15% of all U.S. first-time homebuyers, according to Experian Housing’s recent first-time homebuyer report. This figure puts Colorado in the top 20 of all states across the country.

Colorado’s charm holds a special appeal for younger generations. Known for its wealth of enriching experiences, Colorado naturally attracts adventure-seekers. With an array of outdoor activities like hiking and skiing, it’s no wonder that Generation Y and Generation Z make up 75% of all first-time homebuyers in the state, surpassing the national average of ~70%.

Affordability

With three-quarters of all FTHBs in the younger market segments, affordability is a key consideration in buying a home as housing costs are a significant part of an individual or family’s overall cost of living.2

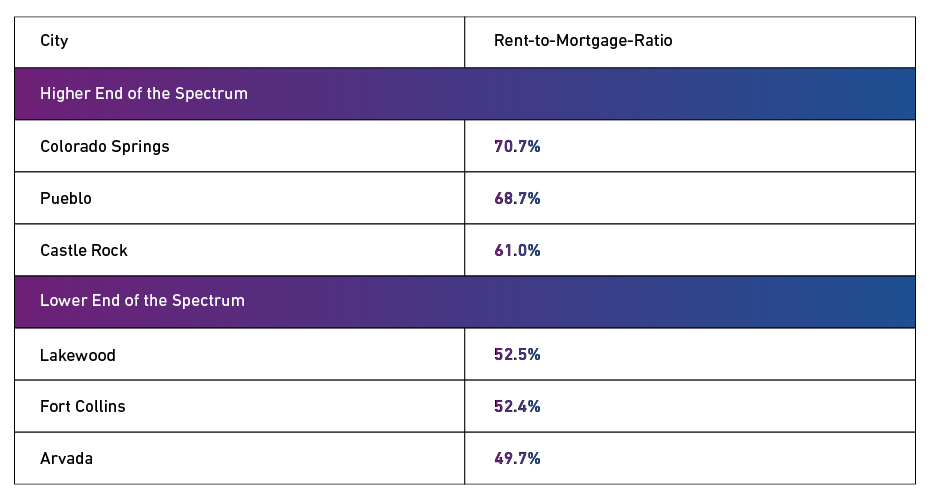

What determines affordability? Affordability can be assessed through various metrics. For the purposes of this study, Experian Housing defined affordability by calculating the rent-to-mortgage ratio (RTM). This involves comparing monthly rent payments to monthly mortgage payments. A higher rent-to-mortgage ratio suggests renters may find mortgage payments more feasible, potentially making home buying a more appealing option.

Comparison of rent costs to mortgage costs

What we observed:

Based on the RTM ratio, home buying is most affordable in Colorado Springs, Pueblo, and Castle Rock, while renting may look more attractive in Lakewood, Fort Collins, and Arvada.

Additional measures to consider:

Other realities play a key role in determining what is affordable. A prospective homebuyer’s income, monthly expenses, downpayment funds available, and the cost of the rent or mortgage payment as an added expense against income, factor heavily in final decision-making.

In this regard, Experian Housing examined other metrics for assessing affordability.

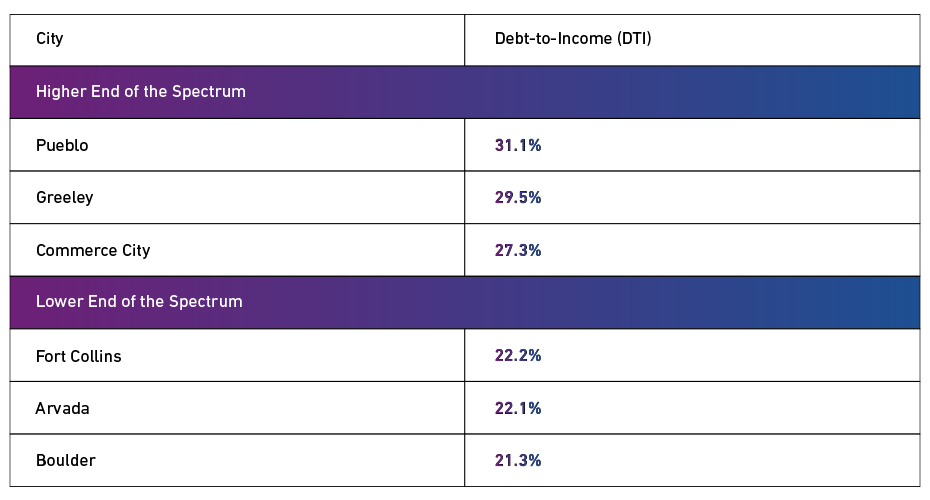

Debt-to-income

What we observed:

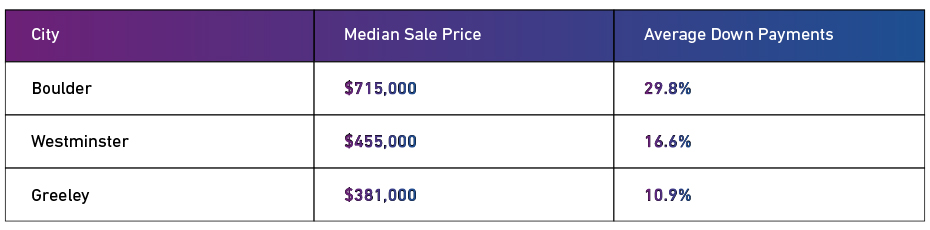

Down payments

Sample of CO data observations: (High, mid, low down payments)

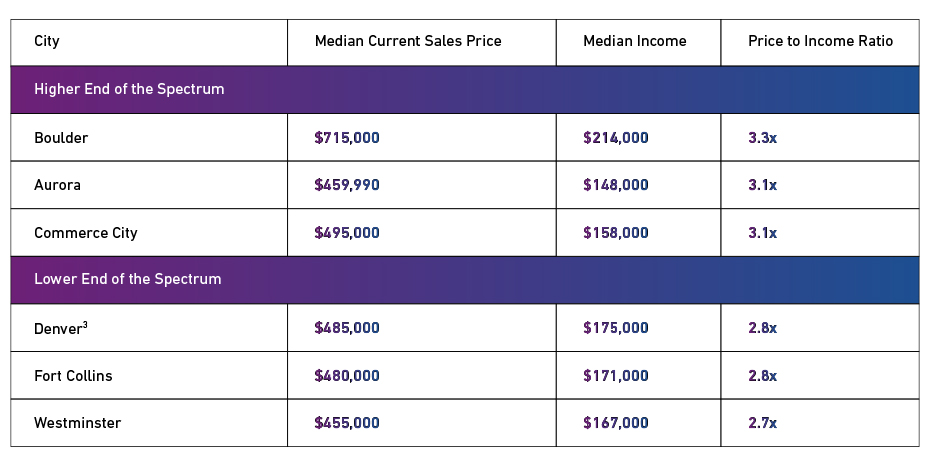

Sale prices and income

What we observed:

Experian Housing examined the median sales prices and median incomes across the U.S. This metric is useful to see how much of one’s income typically is going to housing costs in a given area, which again, impacts overall cost of living.

Comparison is essential because while sales prices may be higher in a given area, correlation with income helps determine affordability.

A closer look at Colorado Springs

Colorado Springs ranks #1 in affordability based on Experian’s research, and its status of best affordable place to live considering overall living costs, jobs, and livability is solid.4

The younger generation is the fastest growing population in Colorado Springs.

Colorado Springs is expected to be the largest city in the state by 2050 given its current rate of growth and expansion.5 In addition to its five military installations, with a huge U.S. Air Force presence, key job sectors include the larger defense industry, education, technology, and manufacturing.

Affordability coupled with opportunity and lifestyle suggest Colorado Springs deserves a closer look and area mortgage lenders have a lot to tout.

Experian’s data system offers unique value to lenders given the ability to take a more comprehensive look at a borrower’s financial behavior. Experian uses credit, property, rental, and other alternative data sources to capture the borrower profile. Access to such data also gives Experian a unique ability to conduct research for reports like this one, and the recent reports on Texas and Florida.

For more information about the lending possibilities for first-time homebuyers, download our white paper and visit us online.

Download white paper Learn more

1 US News & World Report: Best Places to Live in the US 2024-2025 https://realestate.usnews.com/places/rankings/best-places-to-live

2 https://stg1.experian.com/blogs/insights/top-destinations-for-first-time-homebuyers/

3 Arvada, Lakewood and Castle Rock, part of the Denver Metro Area and what is popularly known as the Front Range Urban Corridor, also have price to income ratios of 2.8%.

4 https://www.sofi.com/best-affordable-places-to-live-in-colorado/

5 Colorado Springs Chamber & EDC, coloradospringschamberedc