Tag: first party fraud

Experian on the State of Identity podcast In today’s environment, any conversation on the identity management industry needs to include some mention of synthetic identity risk. The fact is, it’s top of mind for almost everyone. Institutions are trying to scope their risk level and identify losses, while service providers are innovating ways to solve the problem. Even consumers are starting to understand the term, albeit via a local newscast designed to scare the heck out of them. With all this in mind, I was very happy to be invited to speak with Cameron D’Ambrosi at One World Identity (OWI) on the State of Identity podcast, focusing on synthetic identity fraud. Our discussion focused on some of the unique findings and recommended best practices highlighted in our recently published white paper on the subject, Synthetic identities: getting real with customers. Additionally, we discussed how a lack of agreement on the definition and size of the synthetic identity problem further complicates the issue. This all stems from inconsistent loss reporting, a lack of confirmable victims and an absence of an exact definition of a synthetic identity to begin with. Discussions must continue to better align us all. I certainly appreciate that OWI dedicated the podcast to this subject. And I hope listeners take away a few helpful points that can assist them in their organization’s efforts to better identify synthetic identities, reduce financial losses and minimize reputation risks.

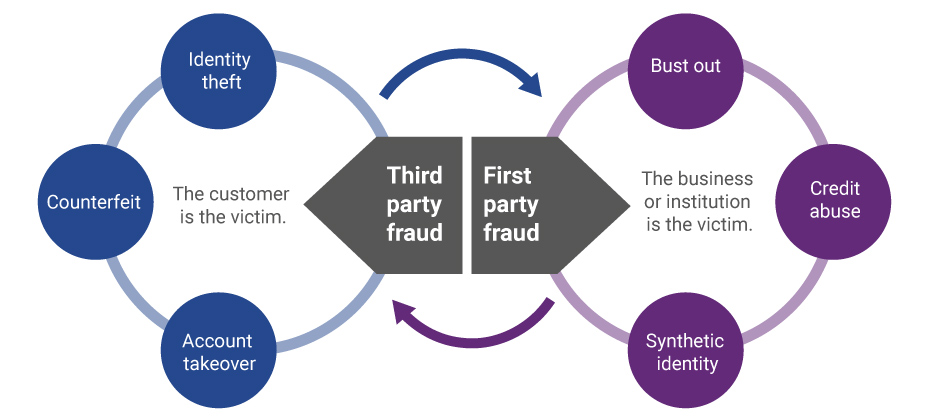

Evolution of first-party fraud to third Third-party and first-party schemes are now interchangeable, and traditional fraud detection practices are less effective in fighting these evolving fraud types. Fighting this shifting problem is a challenge, but it isn’t impossible. To start, incorporate new and more robust data into your identity verification program and provide consistent fraud classification and tagging. Learn more>

A combination of mass identity data compromise and the increasing abilities of organized fraud rings has created a synthetic identity epidemic that is impacting all markets. Here are the three ways that synthetic identities are generally created: Credit applications and inquiries that result in synthetic credit profile creation or build. Exploitation of the authorized user process designed to take over or piggyback on legitimate credit profiles. Data furnishing schemes that falsify regular credit reporting agency updates. When it comes to fighting synthetic fraud, we all need to be a part of the solution – or we are just a part of the problem. Mitigate synthetic identity fraud >

Has the EMV liability shift caused e-commerce fraud to increase 33% in 2016? According to Experian data, CNP fraud increased with Florida, Delaware, Oregon and New York ranked as the riskiest states. Miami accounted for the most fraudulent ZIP™ Codes in the US for shipping and billing fraud.

Experian is recognized as a leading security solution provider for fraud and identity solutions in order to protect customers and financial institutions

Part four in our series on Insights from Vision 2016 fraud and identity track It was a true honor to present alongside Experian fraud consultant Chris Danese and Barbara Simcox of Turnkey Risk Solutions in the synthetic and first-party fraud session at Vision 2016. Chris and Barbara, two individuals who have been fighting fraud for more than 25 years, kicked off the session with their definition of first-party versus third-party fraud trends and shared an actual case study of a first-party fraud scheme. The combination of the qualitative case study overlaid with quantitative data mining and link analysis debunked many myths surrounding the identification of first-party fraud and emphasized best practices for confidently differentiating first-party, first-pay-default and synthetic fraud schemes. Following these two passionate fraud fighters was a bit intimidating, but I was excited to discuss the different attributes included in first-party fraud models and how they can be impacted by the types of data going into the specific model. There were two big “takeaways” from this session for me and many others in the room. First, it is essential to use the correct analytical tools to find and manage true first-party fraud risk successfully. Using a credit score to identify true fraud risk categorically underperforms. BustOut ScoreSM or other fraud risk scores have a much higher ability to assess true fraud risk. Second is the need to for a uniform first-party fraud bust-out definition so information can be better shared. By the end of the session, I was struck by how much diversity there is among institutions and their approach to combating fraud. From capturing losses to working cases, the approaches were as unique as the individuals in attendance This session was both educational and inspirational. I am optimistic about the future and look forward to seeing how our clients continue to fight first-party fraud.

Electronic signatures and their emerging presence in our Internet-connected world I had the opportunity to represent Experian at the eSignRecords 2015 conference in New York City last week. The concept of electronic signature, while not new, certainly has an emerging presence in the Internet-connected world — as evidenced by the various attendee companies that were represented, everything from home mortgages to automobiles. Much of the discussion focused on the legal aspects of accepting an electronic signature in lieu of an in-person physical signature. The implications of accepting this virtual stamp of approval were discussed, as well as the various cases that already have been tried in court. Of course, the outcome of those cases shapes the future of how to properly integrate this new form of authorization into existing business processes. Attendees discussed the basic concept of simply accepting a signature on an electronic pad as opposed to one written on a piece of paper. That act alone has many legal challenges even though it provides the luxury of in-person authentication through a face-to-face meeting. The complexities and risk increase exponentially when these services are extended over the Internet. The ability to sign documents virtually opens up a whole new world of business opportunities, and the concept certainly caters to the consumer’s need for convenience. However, the anonymity of the Internet presents the everyday challenge of balancing consumer expectations of greater ease of use with necessary fraud prevention measures. Ultimately, it always comes back to understanding who is actually signing that document. All of this highlights the need for robust authentication and security measures. As more and more legal documents and contracts are passed around virtually, the opportunity to properly screen and verify who has access to the documents gets more critical. Many organizations still rely on the tried-and-true method of knowledge-based authentication (KBA), while many others have called for its end. KBA continues to soldier on as an effective way to ensure that people on the other end of the wire are who they say they are by asking questions that — presumably — only they know the answers to. In most cases, KBA is viewed as a “check the box” step in the process to satisfy the lawyers. In certain cases, that’s all you need to do to ensure compliance with legal policy or regulatory requirements. It starts to get tricky is when there’s more on the line than just “check the box” actions. When the liability of first- or third-party fraud, becomes greater than simple compliance, it’s time to implement tighter security, while at the same time limiting the amount of friction caused by the process. Many in attendance discussed the need for layers of authentication based on the type of documents that are being processed and handled. This speaks directly to the point that one size does not fit all. As the industry matures and acceptance of e-signatures increases, so too does the need for more robust, flexible options in authentication. Another topic — that was quite frankly foreign to everyone we talked to — was the need for security around the concept of account takeover. When discussing this type of fraud, most attendees did not even consider this to be a hole in their strategy. Consider this fictional scenario. I’m responsible for mergers and acquisitions for my publicly traded company. I often share confidential information via electronic means, leveraging one of the many electronic signature solutions on the market. I become a victim of a phishing attack and unknowingly provide my login credentials to the fraudster. The fraudster now has access to every electronic document that I have shared with various organizations — most of which have been targets for mergers and acquisitions. Fraudsters are creative. They exploit new technologies — not because they’re trendsetters, but because oftentimes these new technologies fail to consider how fraudsters can benefit from the system. If you are considering adopting e-signature as a formal process, please consider implementing: Flexible levels of authentication based on the risk and liability of the documents that are being presented and what they are protecting FraudNet for Account Takeover, which enhances security around access to these critical documents to protect against data breaches Not only the needs and experiences of your own business, but customer needs as well to enable to the best possible customer interactions If you haven’t considered implementing e-signature technology into your business process, you should — but be sure to have your fraud team present when considering the implementation.

We all know that first party fraud is a problem. No one can seem to agree on the definitions of first party fraud and who is on the hook to find it, absorb the losses and mitigate the risk going forward. More often than not, first-party fraud cases and associated losses are simply combined with the relatively big “bucket” of credit losses. More importantly, the means of quickly detecting potential first-party fraud, properly segmenting it (as either true credit risk or malicious behavior) and mitigating losses associated with it usually lies within more general credit policies instead of with unique, targeted strategies designed to combat this type of fraud. In order to create a frame of reference, it’s helpful to have some quick — and yes, arguable — definitions: Synthetic identity: the fabrication of an identity with the intention of perpetrating fraudulent applications for, and access to, credit or other financial services Bust-out: the substantive building of positive credit history, followed by the intentional, high-velocity opening of several new accounts with subsequent line utilization and “never payment” Default payment: intentionally allowing credit lines to default to avoid payments Straight-roller: an account opened with immediate utilization followed by default without any attempt to make a payment Never pay: a form of straight-roller that becomes delinquent within the first few months of opening the account So what’s a risk manager to do? In my opinion, the best methods to consider in the fight against first-party fraud include analytical solutions that take multiple data points into consideration and focus on a risk-based approach. For my money, the four most important are: Models and scores developed with the proper set of identity and credit risk attributes derived from current and historic identity and account usage patterns (in other words, ANALYTICS) — Used at both the account opening and account management phases of the Customer Life Cycle, such analytics can be customized for each addressable market and specific first-party fraud threat The monitoring of individual identity elements at a portfolio level and beyond — This type of monitoring and LINK ANALYSIS allows organizations to detect the creation of synthetic identities Reasonable (e.g., one-to-one) identity and device associations over time versus a cluster of devices or coordinated attacks stemming from a single device — Knowing a customer’s device profile and behavioral usage with DEVICE INTELLIGENCE provides assurance that applications and account access are conducted legitimately Leveraging industry experts who have worked with other institutions to design and implement effective first-party fraud detection and loss-mitigation strategies — This kind of OPERATIONAL CONSULTING can save time and money in the long run and afford an opportunity to avoid mistakes By active use of these methods, you are applying a risk-based approach that will allow you to realize substantial savings in the forms of loss reduction and operational efficiencies associated with non-acquisition of high-risk first-party fraud applications, more effective credit line management of potentially high-risk accounts, better segmentation of treatment strategies and associated spend against high-risk identities, and removal of first-party fraud accounts from traditional collections processes that will prove futile. Download our recent White Paper, Data confidence realized: Leveraging customer intelligence in the age of mass data compromise, to understand how data and technology are needed to strengthen fraud risk strategies through comprehensive customer intelligence.

Understanding and managing first party fraud Background/Definitions Wherever merchants, lenders, service providers, government agencies or other organizations offer goods, services or anything of value to the public, they incur risk. These risks include: Credit risk — Loosely defined, credit risk arises when an individual receives goods/services in exchange for a promise of future repayment. If the individual’s circumstances change in a way that prevents him or her from paying as agreed, the provider may not receive full payment and will incur a loss. Fraud risk — Fraud risk arises when the recipient uses deception to obtain goods/services. The type of deception can involve a wide range of tactics. Many involve receiving the goods/services while attributing the responsibility for repayment to someone else. The biggest difference between credit risk and fraud risk is intent. Credit risk usually involves customers who received the goods/services with intent to repay but simply lack the resources to meet their obligation. Fraud risk starts with the intent to receive the goods/services without the intent to repay. Between credit risk and fraud risk lies a hybrid type of risk we refer to as first-party fraud risk. We call this a hybrid form of risk because it includes elements of both credit and fraud risk. Specifically, first party fraud involves an individual who makes a promise of future repayment in exchange for goods/services without the intent to repay. Challenges of first party fraud First party fraud is particularly troublesome for both administrative and operational reasons. It is important for organizations to separate these two sets of challenges and address them independently. The most common administrative challenge is to align first-party fraud within the organization. This can be harder than it sounds. Depending on the type of organization, fraud and credit risk may be subject to different accounting rules, limitations that govern the data used to address risk, different rules for rejecting a customer or a transaction, and a host of other differences. A critical first step for any organization confronting first-party fraud is to understand the options that govern fraud management versus credit risk management within the business. Once the administrative options are understood, an organization can turn its attention to the operational challenges of first-party fraud. There are two common choices for the operational handling of first-party fraud, and both can be problematic. First party fraud is included with credit risk. Credit risk management tends to emphasize a binary decision where a recipient is either qualified or not qualified to receive the goods/services. This type of decision overlooks the recipient’s intent. Some recipients of goods/services will be qualified with the intent to pay. Qualified individuals with bad intentions will be attracted to the offers extended by these providers. Losses will accelerate, and to make matters worse it will be difficult to later isolate, analyze and manage the first party fraud cases if the only decision criteria captured pertained to credit risk decisions. The end result is high credit losses compounded by the additional first party fraud that is indistinguishable from credit risk. First party fraud is included with other fraud types. Just as it’s not advisable to include first party fraud with credit risk, it’s also not a good idea to include it with other types of fraud. Other types of fraud typically are analyzed, detected and investigated based on the identification of a fraud victim. Finding a person whose identity or credentials were misused is central to managing these other types of fraud. The types of investigation used to detect other fraud types simply don’t work for first-party fraud. First party fraudsters always will provide complete and accurate information, and, upon contact, they’ll confirm that the transaction/purchase is legitimate. The result for the organization will be a distorted view of their fraud losses and misconceptions about the effectiveness of their investigative process. Evaluating the operational challenges within the context of the administrative challenges will help organizations better plan to handle first party fraud. Recommendations Best practices for data and analytics suggest that more granular data and details are better. The same holds true with respect to managing first party fraud. First party fraud is best handled (operationally) by a dedicated team that can be laser-focused on this particular issue and the development of best practices to address it. This approach allows organizations to develop their own (administrative) framework with clear rules to govern the management of the risk and its prevention. This approach also brings more transparency to reporting and management functions. Most important, it helps insulate good customers from the impact of the fraud review process. First-party fraudsters are most successful when they are able to blend in with good customers and perpetrate long-running scams undetected. Separating this risk from existing credit risk and fraud processes is critical. Organizations have to understand that even when credit risk is low, there’s an element of intent that can mean the difference between good customers and severe losses. Read here for more around managing first party fraud risk.

By: Kennis Wong Data is the very core of fraud detection. We are constantly seeking new and mining existing data sources that give us more insights into consumers’ fraud and identity theft risk. Here is a way to categorize the various data sources. Account level - When organizations detect fraud, naturally they leverage the data in-house. This type of data is usually from the individual account activities such as transactions, payments, locations or types of purchases, etc. For example, if there’s a purchase $5000 at a dry cleaner, the transaction itself is suspicious enough to raise a red flag. Customer level - Most of the times we want to see a bigger picture than only at the account level. If the customer also has other accounts with the organization, we want to see the status of those accounts as well. It’s not only important from a fraud detection perspective, but it’s also important from a customer relationship management perspective. Consumer level - As Experian Decision Analytics’ clients can attest, sometimes it’s not sufficient to look only at the data within an organization but also to look at all the financial relationships of the consumer. For example, in the situation of bust out fraud or first-party fraud, if you only look at the individual account, it wouldn’t be clear whether a consumer has truly committed the fraud. But when you look at the behavior of all the financial relationships, then the picture becomes clear. Identity level - Fraud detection can go into the identity level. What I mean is that we can tie a consumer’s individual identity elements with those of other consumers to discover hidden inconsistencies and relationships. For example, we can observe the use of the same SSN across different applications and see if the phones or addresses are the same. In the account management environment, when detecting existing account fraud or account takeover, this level of linkage is very useful as more data becomes available after the account is open. Loading...

Experian recently contributed to a TSYS whitepaper focused on the various threats associated with first party fraud. I think the paper does a good job at summarizing the problem, and points out some very important strategies that can be employed to help both prevent first party fraud losses and detect those already in an institution’s active and collections account populations. I’d urge you to have a look at this paper as you begin asking the right questions within your own organization. Watch here The bad news is that first party fraud may currently account for up to 20 percent of credit charge-offs. The good news is that scoring models (using a combination of credit attributes and identity element analysis) targeted at various first party fraud schemes such as Bust Out, Never Pay, and even Synthetic Identity are quite effective in all phases of the customer lifecycle. Appropriate implementation of these models, usually involving coordinated decisioning strategies across both fraud and credit policies, can stem many losses either at account acquisition, or at least early enough in an account management stage, to substantially reduce average fraud balances. The key is to prevent these accounts from ending up in collections queues where they’ll never have any chance of actually being collected upon. A traditional customer information program and identity theft prevention program (associated, for example with the Red Flags Rule) will often fail to identify first party fraud, as these are founded in identity element verification and validation, checks that often ‘pass’ when applied to first party fraudsters.

By: Kennis Wong As I said in my last post, when consumers and the media talk about fraud and fraud risk, they are usually referring to third-party frauds. When financial institutions or other organizations talk about fraud and fraud best practices, they usually refer to both first- and third-party frauds. The lesser-known fraud cousin, first-party fraud, does not involve stolen identities. As a result, first-party fraud is sometimes called victimless fraud. However, being victimless can’t be further from the truth. The true victims of these frauds are the financial institutions that lose millions of dollars to people who intentionally defraud the system. First-party frauds happen when someone uses his/her own identity or a fictitious identity to apply for credit without the intention to fulfill their payment obligation. As you can imagine, fraud detection of this type is very difficult. Since fraudsters are mostly who they say they are, you can’t check the inconsistencies of identities in their applications. The third-party fraud models and authentication tools will have no effect on first-party frauds. Moreover, the line between first-party fraud and regular credit risk is very fuzzy. According to Wikipedia, credit risk is the risk of loss due to a debtor's non-payment of a loan or other line of credit. Doesn’t the definition sound similar to first-party fraud? In practice, the distinction is even blurrier. That’s why many financial institutions are putting first-party frauds in the risk bucket. But there is one subtle difference: that is the intent of the debtor. Are the applicants planning not to pay when they apply or use the credit? If not, that’s first-party fraud. To effectively detect frauds of this type, fraud models need to look into the intention of the applicants.

By: Kennis Wong When consumers and the media talk about fraud and fraud risk, nine out of ten times they are referring to third-party frauds. When financial institutions or other organizations talk about fraud, fraud best practices, or their efforts to minimize fraud, they usually refer to both first- and third-party frauds. The difference between the two fraud types is huge. Third-party frauds happen when someone impersonates the genuine identity owner to apply for credit or use existing credit. When it’s discovered, the victim, or the genuine identity owner, may have some financial loss -- and a whole lot of trouble fixing the mess. Third-party frauds get most of the spotlight in newspaper reporting primarily because of large-scale identity data losses. These data losses may not result in frauds per se, but the perception is that these consumers are now more susceptible to third-party frauds. Financial institutions are getting increasingly sophisticated in using fraud models to detect third-party frauds at acquisition. In a nutshell, these fraud models are detecting frauds by looking at the likelihood of applicants being who they say they are. Institutions bounce the applicants’ identity information off of internal and external data sources such as: credit; known fraud; application; IP; device; employment; business relationship; DDA; demographic; auto; property; and public record. The risk-based approach takes into account the intricate similarities and discrepancies of each piece of data element. In my next blog entry, I’ll discuss first-party fraud.