Lorem Ipsumis simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry’s standard dummy text ever since the 1500s, when an unknown printer took a galley of type and scrambled it to make a type specimen book. It has survived not only five centuries, but also the leap into electronic typesetting, remaining essentially unchanged

Author One

Inclusion is at the heart of everything we do, and we’ve made it a priority to embrace the diversity that makes up the Experian family. This is why we’re especially proud to release our 2018 The Power of You Inclusion & Diversity Annual Report, highlighting the strides we’ve made to celebrate our diverse work force and create an inclusive company culture. "We believe that embracing a truly inclusive culture, where everyone has a real sense of belonging, is critical to building a diverse workforce and fostering innovation," says Craig Boundy, former chief executive officer of Experian North America. "We don't just encourage inclusion at Experian, we celebrate it." The Power You initiative was created to recognize ways we can create a more supportive work environment and provide greater transparency into our commitment towards diversity and inclusion. We’ve instated progressive policies and programs, such as flexible working, paid parental leave and Experian clubs, to help foster support, empowerment and employee pride about working for Experian. Here are some of the highlights from the report: 89 percent of employees across North America agree that creating a diverse and inclusive work environment is at the forefront of Experian's values More than 900 employees joined our 8 Employee Resource Groups (ERGs) From 2017 to 2018, the percentage of women hired into executive positions increased from 31% to 38% Nearly half of our job applicants were non-white, a 10% increase from 2017 Volunteer Time Off (VTO) was increased from one day to two days Experian North America was honored with a North America Great Place to Work certification and regional Top Workplaces awards From the events organized by our Employee Resource Groups (ERGs) to the support provided by our Experian Hardship Fund, The Power of You initiative is exemplified by the work and dedication our employees have invested to help in our mission to create an inclusive workplace. "Creating a better tomorrow starts within the company, and that's why we're committed to diversity and inclusion," adds Justin Hastings, former chief human resources officer of Experian North America. "We search the globe for the very best people so we can innovate and meet the needs of our increasingly diverse clients. Drawing on this collective strength is what truly makes us a top workplace." Our dedication to creating a more inclusive and supportive workplace has not gone unrecognized. We’ve been honored with a number of high-profile employer awards, including being named the #1 Top Workplace in Orange County by the Orange County Register and one of the World’s Most Innovative Companies for the fifth consecutive year by Forbes Magazine. Innovation starts with creating an inclusive culture and growing a diverse workforce. We are proud of the supportive work culture we’ve created and will continue finding ways we can further build upon the progress we’ve made. A copy of this year's report can be found here. Photos taken by Nhan T. Nguyen.

Fraud attacks continue to increase, and businesses and consumers alike are recognizing the need for more effective preventative measures. In June 2016, we launched the industry’s first open platform designed to catch fraud faster, improve compliance, and enhance the customer experience. Experian CrossCoreTM has put more control in the hands of fraud teams and it continues to receive global recognition for its impact in the industry. We are proud to announce that CrossCoreTM has been named a market leader for fraud prevention by Cyber Defense Magazine’s 7th Annual InfoSec Awards. Judged by an independent panel of certified security professionals, the InfoSec Awards recognize the best ideas, products and services in the information technology industry. In the past year, the platform was also named best fraud prevention innovation by Cybersecurity Breakthrough and as best cybersecurity initiative of the year by CIR Magazine. Since 2016, Experian has been proud to serve organizations looking for better ways to get more out of their existing fraud and identity systems and to more effectively deploy new products and offers, while improving the customer experience and minimizing risk. According to Experian’s 2019 Global Identity & Fraud Report, 55% of businesses reported an increase in online fraud-related losses over the past 12 months, predominantly around account origination and account takeover attacks. Our study shows that consumers value security and convenience. They also expect to be recognized and met with a personalized experience. Businesses can deliver both security and convenience, but to do so, they need to apply the right tools and relevant information. CrossCoreTM is helping fraud teams around the world accomplish this by adapting and deploying strategies that keep up with the pace of fraud while reducing burdens on IT and data science teams. Learn more about CrossCore.

The Human Rights Campaign (HRC) Foundation has recognized Experian with a 100 percent score on their 2019 Corporate Equality Index (CEI), earning the distinction as one of the “Best Places to Work for LGBTQ Equality”. The CEI is the nation’s premier benchmarking tool in evaluating corporate policies and practices related to LGBTQ workplace equality. We are honored to have received such top marks alongside some of America’s most respectable companies. “Our mission as a company is to create greater financial inclusion for consumers, but inclusion also means creating an open and accepting workplaces where everyone can thrive,” said Craig Boundy, former chief executive officer of Experian North America. “We work hard to make diversity and inclusion a priority in our company culture, and our efforts are showing real results.” We strive to celebrate our company’s diversity by creating an inclusive workplace environment where employees feel supported and appreciated. We’ve launched initiatives and implemented policies that have solidified our commitment to being a strong ally to the LGBTQ community. Our dedication to foster a supportive work culture for our LGBTQ employees is exemplified by such practices as: Our progressive benefit programs, which include transgender services and offer equal coverage to same and different-sex domestic partners and spouses. Our non-discrimination and equal employment policies go beyond federal requirements, ensuring equal treatment regardless of “gender identity” or “sexual orientation.” Our dedication to be inclusive through executive sponsorship and the Power of YOU initiative which facilitates Employee Resource Groups and Clubs. "The top-scoring companies on this year's CEI are not only establishing policies that affirm and include employees here in the United States, they are applying these policies to their global operations and impacting millions of people beyond our shores," said HRC president Chad Griffin. Practicing an inclusive work culture has always been one of our top priorities and being honored by the HRC demonstrates our dedication to that goal. We are proud to support our LQBTQ employees, along with the diverse work force that make up the Experian family. For more information on the 2019 Corporate Equality Index, download the HRC report.

More areas of the business are leveraging data and insight around customers than ever before. Today’s digital consumer puts more pressure on organizations to provide personal interactions across all industries, even when that individual is not interacting face-to-face. In order to accomplish that monumental feat, businesses are turning to their data assets to give them the insights they so desperately need. But that is no easy task. We find that most organizations lack trust in their data, typically due to outdated and ineffective data management practices. Businesses can no longer wait for others within the organization to improve the quality of their data. Many are looking to take more control themselves. In fact, according to a recent Experian study, 75 percent of respondents believe data quality responsibility should ultimately lie with the business with occasional help from IT. The rise of the business user is putting more pressure on the tools they leverage. While data quality is a continuous practice that requires constant care, it is certainly enabled by technology. That technology needs to be easy-to-use, intuitive, and provide value back to the business quickly. This week, the 2019 Gartner Magic Quadrant for Data Quality Tools was issued. The report provides an overview of the players in the space and the "key capabilities that organizations need in their tool portfolio, if they are to address the increasing importance and urgency of data quality." The business user is reshaping the data quality market. Now, rather than looking at just features and functions, new Experian research shows that the ease of use by business users and the ability to work with existing technology are more important. These tools need to be designed differently than they have in the past. 56% of businesses say their IT department doesn’t fully understand the data management needs of the business. That means that organizations need to put their data more in the hands of the people who leverage it every day. At Experian Data Quality, we believe in empowering business users to better understand their data assets in order to transform their businesses. We offer easy-to-implement, easy-to-use tools that are designed to help businesses maximize their data insight and build trust in their information. We want our clients to tackle their projects with speed and agility, giving them the confidence and clarity to put their data to good use. We are proud to be named a ‘Challenger’ once again in Gartner’s 2019 Magic Quadrant for Data Quality Tools. We believe in the changing nature of the business and are working to challenge the status-quo in our industry and for our clients. Access the Gartner 2019 Magic Quadrant for Data Quality Tools report.

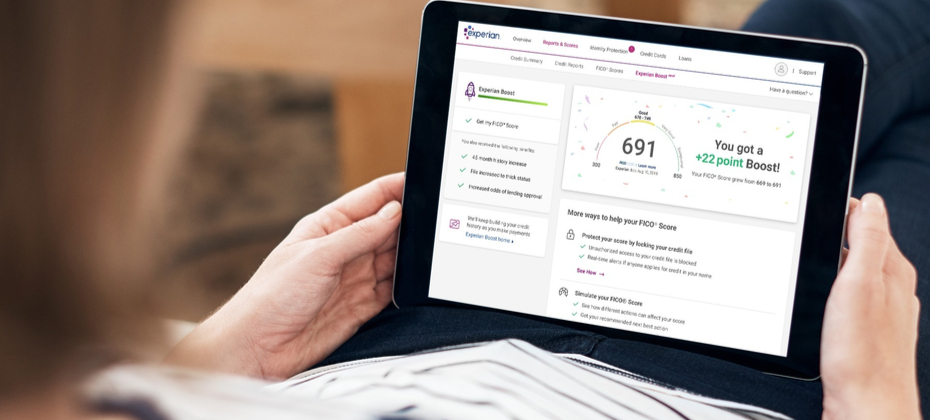

Today marks a notable milestone in our company’s history and for consumers. Today we officially launched Experian Boost, a free tool that, for the first time, will allow millions of consumers to add positive payment history directly into their credit file for an opportunity to instantly increase their credit score. For the past several years, we have been working to develop new products and innovations that will disrupt the credit industry and help improve the financial lives of consumers. This commitment to financial inclusion has defined us and created a real sense of purpose for everyone who works here – and that purpose is realized with the launch of Experian Boost today. There are more than 100 million Americans who don't have access to credit today. A low credit score, due to a thin file or incomplete information, may force these consumers to rely on high interest credit cards and loans. The fact that many of these consumers consistently and responsibly pay cell phone and utility bills on time every month hasn’t seemed to matter. At Experian, we know that’s not right. A good credit score is a gatekeeper to better financial opportunities. We need to develop products and services that make achieving and maintaining a good score easier, not harder. As the consumer’s bureau, we want to ensure that as many people as possible can access and participate in the financial system, and we believe everyone deserves a fair shot at achieving their financial dreams. We have a fundamental mission that is shared by our colleagues around the world: to strive to be a champion for the consumer. With Experian Boost, we're bringing that mission to life and I couldn’t be prouder. Many of our colleagues at Experian worked tirelessly over the last few years to make this day a reality. To everyone who’s played a part, I offer my very heartfelt thanks. It’s truly a great day to be a part of Experian, and we know there will be a lot of great days ahead for all the consumers who will benefit from having their credit score truly reflect who they are. To find out more about the Experian Boost, please visit experian.com/boost.

In this article…

First Heading

Lorem Ipsumis simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry’s standard dummy text ever since the 1500s, when an unknown printer took a galley of type and scrambled it to make a type specimen book. It has survived not only five centuries, but also the leap into electronic typesetting, remaining essentially unchanged

It was popularised in the 1960s with the release of Letraset sheets containing Lorem Ipsum passages, and more recently with desktop publishing software like Aldus PageMaker including versions of Lorem Ipsum.

Why do we use it?

It is a long established fact that a reader will be distracted by the readable content of a page when looking at its layout. The point of using Lorem Ipsum is that it has a more-or-less normal distribution of letters, as opposed to using ‘Content here, content here’, making it look like readable English. Many desktop publishing packages and web page editors now use Lorem Ipsum as their default model text, and a search for ‘lorem ipsum’ will uncover many web sites still in their infancy. Various versions have evolved over the years, sometimes by accident, sometimes on purpose (injected humour and the like).

It was popularised in the 1960s with the release of Letraset sheets containing Lorem Ipsum passages, and more recently with desktop publishing software like Aldus PageMaker including versions of Lorem Ipsum.

Why do we use it?

It is a long established fact that a reader will be distracted by the readable content of a page when looking at its layout. The point of using Lorem Ipsum is that it has a more-or-less normal distribution of letters, as opposed to using ‘Content here, content here’, making it look like readable English. Many desktop publishing packages and web page editors now use Lorem Ipsum as their default model text, and a search for ‘lorem ipsum’ will uncover many web sites still in their infancy. Various versions have evolved over the years, sometimes by accident, sometimes on purpose (injected humour and the like).

Second Heading

It was popularised in the 1960s with the release of Letraset sheets containing Lorem Ipsum passages, and more recently with desktop publishing software like Aldus PageMaker including versions of Lorem Ipsum.

Where can I get some?

There are many variations of passages of Lorem Ipsum available, but the majority have suffered alteration in some form, by injected humour, or randomised words which don’t look even slightly believable. If you are going to use a passage of Lorem Ipsum, you need to be sure there isn’t anything embarrassing hidden in the middle of text. All the Lorem Ipsum generators on the Internet tend to repeat predefined chunks as necessary, making this the first true generator on the Internet. It uses a dictionary of over 200 Latin words, combined with a handful of model sentence structures, to generate Lorem Ipsum which looks reasonable.

There are many variations of passages of Lorem Ipsum available, but the majority have suffered alteration in some form, by injected humour, or randomised words which don’t look even slightly believable. If you are going to use a passage of Lorem Ipsum, you need to be sure there isn’t anything embarrassing hidden in the middle of text. All the Lorem Ipsum generators on the Internet tend to repeat predefined chunks as necessary, making this the first true generator on the Internet. It uses a dictionary of over 200 Latin words, combined with a handful of model sentence structures, to generate Lorem Ipsum which looks reasonable. The generated Lorem Ipsum is therefore always free from repetition, injected humour, or non-characteristic words etc.

Author test

Buttons margin test