Today is Transgender Day of Visibility. A day to celebrate trans people around the world, highlighting their experiences, perspectives and also unfortunately spotlighting the discrimination and challenges they still face. A recent report from TotalJobs found that the number of trans workers in the UK surveyed who said they hid their gender identity at work has risen in the past 5 years – from 52% in 2016 to 65% in 2021. It also found that 43% of trans employees surveyed said they had left a job because the environment was unwelcoming, up from 36% in 2016. This should make us all sit up and want to take action. At Experian, we want colleagues of all gender identities to feel comfortable and safe bringing their whole selves to work. We’ve been working hard on how we can continue to improve the support we offer our trans and non-binary colleagues. We realise that choosing to be open about one’s gender identity is a very personal decision, but all trans and non-binary employees should feel safe at Experian if they choose to disclose. Last year we re-wrote our Transitioning at Work policy to ensure it is reflective and inclusive of the experiences and identities of employees who may use it. We offer paid leave to attend medical appointments and we also provide help in changing your records on our systems. Where an employee chooses to disclose information about their gender identity or status, we treat this information with the utmost confidentiality. We never share this information without the written consent of the individual. We encourage our employees to self-identify and recognise the issues in the current Gender Recognition Act. In September, we supported Stonewall’s Trans Right are Human Rights campaign, pushing for its reform. We continue to monitor the progress that has been made but also progress that is yet to come. It’s important you know that Experian will never ask for you to show a Gender Recognition Certificate (GRC) and we respect your right to privacy as to whether or not you have one. At Experian, we take an always listening, always learning approach to building awareness and acceptance. Creating safe spaces for meaningful dialogue is something we really strive for. It is the responsibility of all our employees to respect their colleagues and to create an inclusive workplace where everyone feels they can belong. We have zero tolerance for discrimination, bullying or harassment and take any incidents very seriously. Experian continues to work with the Experian Pride Network UK&I alongside LGBTQ+ charities Stonewall and Mermaids in the UK to further the inclusion of our trans and non-binary employees. We want all trans and non-binary employees at Experian to feel safe and be able to be themselves at work and we expect all colleagues to support each other to make that real.

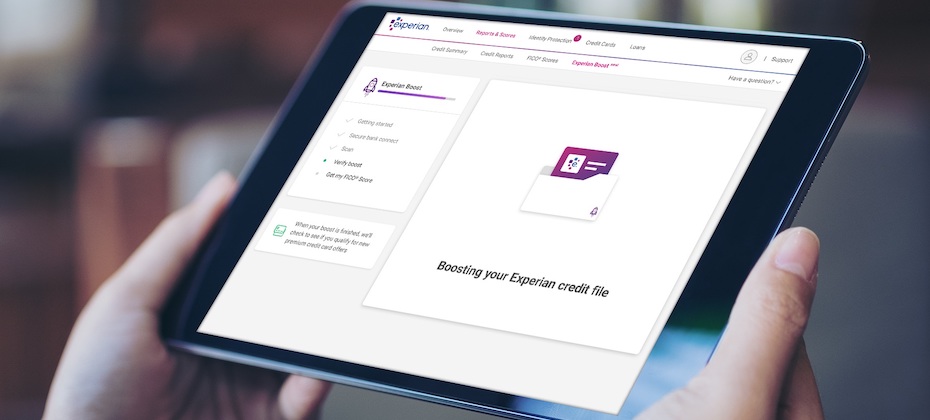

After launching Experian Boost, the first-of-its-kind tool that allows consumers to instantly increase their credit scores, in March 2019 we recently reached a significant milestone. Millions of consumers have boosted their credit scores to the tune of 50 million total points. This means many consumers have improved score bands, saved money with better interest rates, and maybe reached some of their financial goals such as gaining access to credit for a home. In fact, we know our Boost users have gained access to more than 1.7 billion total dollars in credit as a result of improving their credit score. The idea behind Experian Boost is to give consumers control over their credit – to enable them to make real, substantial progress in their financial health journey by getting “credit” for paying bills on time. Our ability to help consumers in a challenging economic climate is what drives us to continue to innovate. For example, we recently expanded Experian Boost to add positive payment history for video streaming services such as Netflix in addition to telecom and utility payments. The benefits to having control and using tools like Experian Boost do not end there. Consumers receive a boosted FICO® Score, which is used by a majority of lenders giving them a great opportunity for credit with better terms. In the first year after launching, we saw one million consumers add a credit card and nearly 250,000 consumers acquired an auto loan. Also, some consumers earned a credit score for the first time. What is also significant about Experian Boost is that this type of financial control and opportunity gives consumers a sense of empowerment, motivation and satisfaction that they can take a positive step in their financial journey. We’ve heard this firsthand from consumers through focus groups, and we even featured some consumers in our commercials who shared their positive experiences in front of the camera. This sentiment of empowerment among consumers is especially important right now as many are struggling financially due to the pandemic. We have many exciting new tools launching in 2021 and will continue to focus on empowering consumers to reach their financial goals. To learn more about Experian Boost, visit www.experian.com/boost.

Does checking my credit report hurt my credit score? How can I improve my credit score? What’s the difference between a credit score and a credit report? These are a few of the questions I most often hear about credit, and the answers to these fundamental questions are essential to financial well-being. Understanding credit scores and the factors that influence overall credit health is important any time, but this is especially true in our current environment. As part of our ongoing commitment to consumer education on the road to recovery, I recently had the pleasure of partnering with Akbar Gbajabiamila, host of American Ninja Warrior, former football pro and financial fitness expert, for an Instagram Live event. Akbar is passionate about helping people develop a financial game plan and he understands having a good credit history is a key component of good financial health. During the Instagram Live event, I answered questions from Akbar’s fans and shared ways to improve your credit score through tools like Experian Boost. In case you missed it, you can watch the video recap on Akbar’s Instagram account (@akbar_gbaja) or at the following link: https://www.instagram.com/tv/CLpbdDJlaQ6/ View this post on Instagram A post shared by 🇳🇬Akbar Gbajabiamila🇺🇸 (@akbar_gbaja) A positive credit history can be the gatekeeper to many of the things we all want in life, and we’re committed to helping facilitate fair and affordable access to credit for all consumers, including those in marginalized communities. This is one of the many reasons I’m passionate about my role at Experian. Educating consumers about credit is an important part of getting the economy as a whole humming again and helping those most in need. If you have additional questions about credit, feel free to check out the free resources below. Additional credit education resources and tools Join Experian’s weekly#CreditChat hosted by @Experian on Twitter with financial experts every Wednesday at 3 p.m. Eastern time. Visit the Ask Experian blog for answers to common questions, advice and education about credit. Add positive telecom, utility and streaming service payments to your Experian credit report for an opportunity to improve your credit scores by visiting experian.com/boost. You can request a free copy of your credit report from each of the three credit bureaus once a week through April 20, 2022 by visiting annualcreditreport.com For additional resources, visit https://www.experian.com/consumereducationor experian.com/coronavirus.

Experian Extends Availability of Free Weekly Credit Reports to Help Americans Recover From COVID-19

NA – North AmericaWe recognize that COVID-19 has challenged Americans across the country, and nearly a year later, people are still struggling to recover. Among the more pressing issues for people has been navigating the financial landscape and hardships brought on by illness and high unemployment rates. At Experian, we empathize with consumers and are committed to helping them manage their financial lives. As part of this commitment, Experian, along with the other U.S. credit reporting agencies, is continuing to offer free weekly credit reports to all Americans for an additional year via AnnualCreditReport.com. At Experian, we view ourselves as the consumers’ bureau, and aim to help people better position themselves as they recover from COVID-related hardships. We’re proud of our ongoing efforts to assist consumers, particularly during these difficult times. Financial and credit information is constantly updated, and we believe providing consumers with increased access to their credit reports will help them improve their financial health, monitor for lender updates and ensure there is no fraudulent or unfamiliar activity on their credit profiles. We are committed to helping facilitate access to fair and affordable access to credit for all consumers. Our goal is not only to help consumers build credit, but also to effectively manage it. Beyond our continued offering of free credit reports, consumers can access resources and educational materials to help learn about credit and other important personal finance topics. In fact, we recently launched our United for Financial Health project to empower vulnerable populations to improve their financial health through education and action. We’re continually exploring new ways to use our data and resources to empower consumers and to improve their financial health and recover from COVID-19; extending access to free weekly credit reports is just another step in that process.

Experian’s 2020 Inclusion & Diversity Report Underscores Community Service During COVID-19

Diversity & InclusionA year ago, we shifted our business to remote working as the global pandemic took hold. Like the rest of the world, we had no idea how long we’d be away, but we didn’t really imagine we’d still be operating our business with a remote workforce a year later. What a year it has been. It is incredible to look back and reflect on how our lives have changed, how we were able to adapt to this new way of living and working, and really importantly, how we were able to keep innovating to help communities and businesses during this difficult time. We have captured highlights of our work and efforts in our North America annual diversity and inclusion report, 2020 Power of YOU. At Experian, the safety and well-being of our colleagues has consistently been a top priority. As such, we have been able to focus on serving consumers and clients when and where they need help the most. As a company, we expanded our benefits to take care of our employees. Coworkers jumped in to take care of each other. Our employee resource group dedicated to mental health and caregiving partnered with colleagues to create a dynamic set of tools and guides tackling different topics every week through webinars, articles and personal, candid videos from leaders. We supported each other during times of social unrest. We celebrated progress in growing our business. We logged 18,000 volunteer hours to increase financial inclusion, support frontline healthcare workers, honor active duty military and veterans, and fight hunger in underprivileged communities. We leveraged our diversity of perspectives, backgrounds and experiences to help vulnerable populations in crisis from COVID-19, including launching our United for Financial Health program. We remain steadfast and committed to equity for all. We are proud to start the new year with this wonderful look back at last year, propelling us forward to more opportunities to innovate and serve. We invite you to check out the 2020 Power of YOU Report here.

As consumer demand for the digital channel continues to increase at an exceptional rate it has created an opportunity for businesses to serve the growing ranks of connected consumers. The most important thing is for businesses to ensure they are putting the consumer at the heart of the relationship. Experian has been studying insights related to consumer behavior and business strategy throughout the Covid-19 pandemic. For the third wave of our Global Insights Report we surveyed 3,000 consumers and 900 businesses across the globe in January. We observed not only consumer demand for the digital channel increasing but that fact that these trends are persisting. We believe that what started as necessity has turned into a preference. According to the report, 38% of consumers expect to increase their online activity in the next 12 months. Furthering our belief that the preference for digital transactions persists, 60% of consumers are using a universal mobile wallet to make digital payments. We also found that the two top activities among consumers online are personal banking (58%) and ordering groceries and takeout food (56%). The report also shows that security remains at the top of consumers’ minds when they are transacting online. 55%of consumers say security is the most important factor in their digital experience – this is highest in the UK (65%), followed by Japan (64%). All in all, the new research confirms that this shift to online activity, which continues to increase with no indications of slowing down, is a contributing factor to consumers’ growing appetite for digital. In this regard, we found that businesses have taken notice and are investing more resources around the digital experience. In fact, 9 in 10 businesses have a strategy in place related to the digital customer journey. 47% of businesses have put this strategy into place since Covid-19. In addition, more than a third of businesses are increasing staff or support for digital operations and experience. Fraud is the biggest challenge among businesses. However, 55% of businesses plan to increase fraud management budgets. As we move towards a post-pandemic era, and more consumers start to prefer banking and shopping online, a digital channel strategy simply isn’t enough. There needs to be a re-imagined customer journey that connects identity, preferences, products, and service. And data and technology have the power to help transform your customer relationships.

Related Posts

Read Moreio55 Button 2- Learn more Primary button Secondary button Related Posts

Insights from Reuters Next: Building a More Inclusive Financial System with Data and AI

Data & AnalyticsToday, we stand at the forefront of a digital revolution that is reshaping the financial services industry. And, against this backdrop, financial institutions are at vastly different levels of maturity; the world’s biggest banks are managing large-scale infrastructure migrations and making significant investments in AI while regional banks and credit unions are putting plans in place for modernization strategies, and fintechs are purpose-built and cloud native. To explore this more, I recently had the privilege of attending the annual Reuters NEXT live event in New York City. The event gathers globally recognized leaders across business, finance, technology, and government to tackle some of today’s most pressing issues. On the World Stage, I joined Del Irani, a talented anchor and broadcast journalist, to discuss the future of lending and the pivotal role of data and AI in building a more inclusive financial system. Improving financial access Our discussion highlighted the lack of access to traditional financial systems, and the impact it has on nearly 100 million people in North America alone. Globally, the problem affects over one billion people. These people, who are credit invisible, unscoreable, or have subprime credit scores, are unable to secure everyday financial products that many of us take for granted. What many don’t realize is, this is not a fringe subset of the population. Most of us, myself included, know someone who has faced the challenges of financial exclusion. Everyday Americans, including young people who are just starting out, new immigrants and people from diverse communities, often lack access to mainstream financial products. We discussed how traditional lending has a limited view of a consumer. Like looking through a keyhole, the lender’s understanding of the person in view is often incomplete and obstructed. However, with expanded data, technology, and advanced analytics, there is an opportunity to better understand the whole person, and as a result have a more inclusive financial system. At Experian, we have a unique ability to connect the power of traditional credit with alternative data, bringing a more holistic understanding of consumers and their behaviors. We are dedicated to leveraging our rich history in data and our expertise in technology to create the future of credit and ultimately bring financial power to everyone. The future of lending After spending two days with over 700 industry leaders from around the world, one thing is abundantly clear: much like the early days of the internet, today, we are at the cutting-edge of a technical revolution. Reflecting on my time at Reuters NEXT, I am particularly excited by the collective commitment to drive innovative, and smarter ways of working. We are only beginning to scratch the surface of how data and technology can transform financial services, and Experian is positioned to play a significant role. As we look to the future, I am excited about the ways we will create new opportunities for businesses and consumers alike.

The advertising ecosystem has seen significant transformation over the past few years, with increased privacy regulation, changes in available signals, and the rise of channels like connected TV and retail media. These changes are impacting the way that consumers interact with brands and how brands understand and continue to deliver relevant messages to consumers with precision. Experian has been helping marketers navigate these changes, and as a result, our marketing data and identity solutions underpin much of today’s advertising industry. We’re committed to empowering marketers and agencies to understand and reach their target audiences, across all channels. Today, we are excited to announce our acquisition of Audigent—a leading data and activation platform in the advertising industry. With Audigent’s combination of first-party publisher data, inventory and deep supply-side distribution relationships, publishers, big and small, can empower marketers to better understand their customers, expand the reach of their target audiences and activate those audiences across the most impactful inventory. I am excited to bring together Audigent’s supply-side network as a natural extension to our existing demand-side capabilities. Audigent’s ability to combine inventory with targeted audiences using first-party, third-party and contextual signals provides the best of all worlds, allowing marketers to deliver campaigns centered on consumer choices, preferences, and behaviors. The addition of Audigent further strengthens our strategy to be the premier independent provider of marketing data and identity, ultimately creating more relevant experiences for consumers. To learn more about Experian and Audigent, visit https://www.experian.com/marketing/ and https://audigent.com/.