At Experian, we often say our people are our biggest superpower – and today, I’m thrilled to share that this belief has been recognised once again. Experian has been named one of the 2025 World’s Best Workplaces™ by Fortune and Great Place to Work® for the second year in a row.

This achievement reflects the culture we’ve built together – one that’s welcoming, inclusive, and rooted belonging. It’s a celebration of every colleague who brings their whole self to work, who lifts others up, and who powers opportunities for our clients, consumers, and communities.

We’ve made it our mission to create a workplace where everyone feels included, respected, and empowered. That’s why we’re proud to have earned top scores on the Corporate Equality Index and the Disability Equality Index, and to be recognised with the Outie Award for Workplace Excellence and Belonging.

These recognitions matter. But what matters most is how our people experience life at Experian. Whether it’s collaborating, innovating, or growing through world-class development of products, services and contributing to our communities, our culture is designed to help everyone thrive.

We’ve also made bold commitments to career development. Initiatives like Global Careers Week, the AI-driven performance coach Nadia, and the NextGen Forum – a global leadership development programme for emerging talent from across our regions – give our people the resources to take charge of their growth and build a “One Experian” mindset.

Being named one of the World’s Best Workplaces is a moment to celebrate but also a reminder to keep aiming higher. The world of work is evolving fast, and so are we. From embracing AI to enhancing our digital workplace experience, we’ll continue to push forward and listen to our people every step of the way.

Questions we will discuss:

- What does “retirement readiness” mean to you, and how can someone tell when they are financially ready to retire?

- Is there a magic number for retirement savings, and what factors should someone consider when setting a retirement goal?

- How can someone estimate their retirement expenses realistically?

- What are some common myths or misconceptions about how much money you need to retire?

- How should Gen Z, Millennials, and Gen Xers each approach retirement planning differently based on their stage of life?

- What are the biggest obstacles people face when trying to save for retirement, and how can they overcome them?

- How can you balance saving for retirement with paying off debt or supporting family today?

- What tools, calculators, or strategies can help people figure out if they’re on track for retirement?

- How can people prepare for unexpected costs or life changes that could impact their retirement plans?

- What’s one piece of advice you’d give someone just starting—or restarting—their retirement savings journey?

| Columns 1 | Column 2 | Column 3 | Column 4 |

|---|---|---|---|

| Row 1 Col 1 | |||

| Row 2 Col 1 | |||

| Row 3 Col 1 | |||

| Footer 1 | Footer 2 | Footer 3 | Footer 4 |

Credit Chat

Stretching your Dollars: Practical Tips to Cut Costs and Save More

February 5, 2025 3-4 PM ET

- What does “retirement readiness” mean to you, and how can someone tell when they are financially ready to retire?

- Is there a magic number for retirement savings, and what factors should someone consider when setting a retirement goal?

- How can someone estimate their retirement expenses realistically?

Greater transparency in buy now, pay later activity is key to helping consumers build their credit histories and supporting responsible lending. We have members of the military right now right out of high school and there’s not a lot of experience managing their own money. They’re quickly thrust into a place where they don’t have a support system to do that. We have members of the military right now right out of high school and there’s not a lot of experience managing their own money. They’re quickly thrust into a place where they don’t have a support system to do that. We have members of the military right now right out of high school and there’s not a lot of experience managing their own money. They’re quickly thrust into a place where they don’t have a support system to do that. We have members of the military right now right out of high school and there’s not a lot of experience managing their own money. They’re quickly thrust into a place where they don’t have a support system to do that. We have members of the military right now right out of high school and there’s not a lot of experience managing their own money. They’re quickly thrust into a place where they don’t have a support system to do that.

Experian North AmericaScott Brown, Group President, Financial Services

The Human Rights Campaign (HRC) Foundation has recognized Experian with a 100 percent score on their 2019 Corporate Equality Index (CEI), earning the distinction as one of the “Best Places to Work for LGBTQ Equality”. The CEI is the nation’s premier benchmarking tool in evaluating corporate policies and practices related to LGBTQ workplace equality. We are honored to have received such top marks alongside some of America’s most respectable companies. “Our mission as a company is to create greater financial inclusion for consumers, but inclusion also means creating an open and accepting workplaces where everyone can thrive,” said Craig Boundy, former chief executive officer of Experian North America. “We work hard to make diversity and inclusion a priority in our company culture, and our efforts are showing real results.” We strive to celebrate our company’s diversity by creating an inclusive workplace environment where employees feel supported and appreciated. We’ve launched initiatives and implemented policies that have solidified our commitment to being a strong ally to the LGBTQ community. Our dedication to foster a supportive work culture for our LGBTQ employees is exemplified by such practices as: Our progressive benefit programs, which include transgender services and offer equal coverage to same and different-sex domestic partners and spouses. Our non-discrimination and equal employment policies go beyond federal requirements, ensuring equal treatment regardless of “gender identity” or “sexual orientation.” Our dedication to be inclusive through executive sponsorship and the Power of YOU initiative which facilitates Employee Resource Groups and Clubs. "The top-scoring companies on this year's CEI are not only establishing policies that affirm and include employees here in the United States, they are applying these policies to their global operations and impacting millions of people beyond our shores," said HRC president Chad Griffin. Practicing an inclusive work culture has always been one of our top priorities and being honored by the HRC demonstrates our dedication to that goal. We are proud to support our LQBTQ employees, along with the diverse work force that make up the Experian family. For more information on the 2019 Corporate Equality Index, download the HRC report.

More areas of the business are leveraging data and insight around customers than ever before. Today’s digital consumer puts more pressure on organizations to provide personal interactions across all industries, even when that individual is not interacting face-to-face. In order to accomplish that monumental feat, businesses are turning to their data assets to give them the insights they so desperately need. But that is no easy task. We find that most organizations lack trust in their data, typically due to outdated and ineffective data management practices. Businesses can no longer wait for others within the organization to improve the quality of their data. Many are looking to take more control themselves. In fact, according to a recent Experian study, 75 percent of respondents believe data quality responsibility should ultimately lie with the business with occasional help from IT. The rise of the business user is putting more pressure on the tools they leverage. While data quality is a continuous practice that requires constant care, it is certainly enabled by technology. That technology needs to be easy-to-use, intuitive, and provide value back to the business quickly. This week, the 2019 Gartner Magic Quadrant for Data Quality Tools was issued. The report provides an overview of the players in the space and the "key capabilities that organizations need in their tool portfolio, if they are to address the increasing importance and urgency of data quality." The business user is reshaping the data quality market. Now, rather than looking at just features and functions, new Experian research shows that the ease of use by business users and the ability to work with existing technology are more important. These tools need to be designed differently than they have in the past. 56% of businesses say their IT department doesn’t fully understand the data management needs of the business. That means that organizations need to put their data more in the hands of the people who leverage it every day. At Experian Data Quality, we believe in empowering business users to better understand their data assets in order to transform their businesses. We offer easy-to-implement, easy-to-use tools that are designed to help businesses maximize their data insight and build trust in their information. We want our clients to tackle their projects with speed and agility, giving them the confidence and clarity to put their data to good use. We are proud to be named a ‘Challenger’ once again in Gartner’s 2019 Magic Quadrant for Data Quality Tools. We believe in the changing nature of the business and are working to challenge the status-quo in our industry and for our clients. Access the Gartner 2019 Magic Quadrant for Data Quality Tools report.

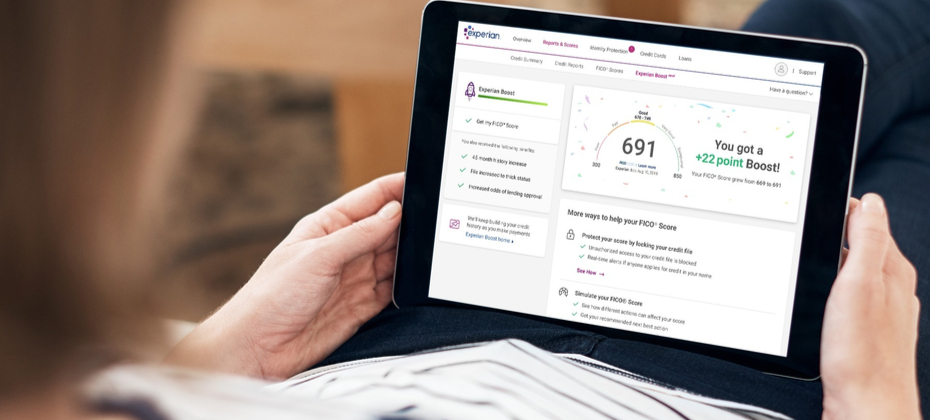

Today marks a notable milestone in our company’s history and for consumers. Today we officially launched Experian Boost, a free tool that, for the first time, will allow millions of consumers to add positive payment history directly into their credit file for an opportunity to instantly increase their credit score. For the past several years, we have been working to develop new products and innovations that will disrupt the credit industry and help improve the financial lives of consumers. This commitment to financial inclusion has defined us and created a real sense of purpose for everyone who works here – and that purpose is realized with the launch of Experian Boost today. There are more than 100 million Americans who don't have access to credit today. A low credit score, due to a thin file or incomplete information, may force these consumers to rely on high interest credit cards and loans. The fact that many of these consumers consistently and responsibly pay cell phone and utility bills on time every month hasn’t seemed to matter. At Experian, we know that’s not right. A good credit score is a gatekeeper to better financial opportunities. We need to develop products and services that make achieving and maintaining a good score easier, not harder. As the consumer’s bureau, we want to ensure that as many people as possible can access and participate in the financial system, and we believe everyone deserves a fair shot at achieving their financial dreams. We have a fundamental mission that is shared by our colleagues around the world: to strive to be a champion for the consumer. With Experian Boost, we're bringing that mission to life and I couldn’t be prouder. Many of our colleagues at Experian worked tirelessly over the last few years to make this day a reality. To everyone who’s played a part, I offer my very heartfelt thanks. It’s truly a great day to be a part of Experian, and we know there will be a lot of great days ahead for all the consumers who will benefit from having their credit score truly reflect who they are. To find out more about the Experian Boost, please visit experian.com/boost.

2024 Best Place to Work for Disability Inclusion

Web Developer

With a passion for crafting seamless digital experiences and a keen eye for front-end development, Krishna brings practical insights and hands-on expertise to every post. Whether exploring new frameworks or optimizing performance, his writing reflects a commitment to clean code and user-centric design.

With a passion for crafting seamless digital experiences and a keen eye for front-end development, Krishna brings practical insights and hands-on expertise to every post. Whether exploring new frameworks or optimizing performance, his writing reflects a commitment to clean code and user-centric design.

With a passion for crafting seamless digital experiences and a keen eye for front-end development, Krishna brings practical insights and hands-on expertise to every post. Whether exploring new frameworks or optimizing performance, his writing reflects a commitment to clean code and user-centric design.