Innovation

At Experian, we are continually innovating and using technology to find solutions to global issues, modernize the financial services industry and increase financial access for all. Read about our latest innovation news below:

We welcome this week’s response by the UK Government in relation to its work on the new UK Data Strategy, and the commitment to creating a new UK Data Act. Innovative data use has a crucial role to play as Britain takes its place on the global stage. Data has the ability to change people’s lives for the better. It can help build a stronger, smarter future, whether that is through existing products and services or by enabling new and innovative solutions to the problems people and society face today. We share the Government’s goal of using data to deliver better outcomes for people across the UK, and to supercharge its economic success. Already today we see data doing great good in the world: it is enabling the deployment of resources from charities and Government where they are most needed; reducing the number of credit-invisible people and combatting loan sharks; preventing fraud and supporting those who fall victim to fraudsters; and delivering unique new insights that set creators and entrepreneurs on the path to their next success. Data played a transformative, positive role in people’s lives during the pandemic, and has the potential to do so much more as we look to the future. It is crucial that data is used and managed within a trusted, privacy centric framework, and that we as industry and Government together continue to educate and empower people to understand how their data is used, and to be confident in its security. Properly-consented, properly-secured data can empower people; it can support the vulnerable; it can help expand and accelerate our economy. We have the talent, the drive and the ambition in Britain to do all of these things. The new framework sets a foundation to enable and empower, making Britain a desirable hub for investment; a great place to work and build a career; an ideal place to begin new ventures or find funding for existing ones. With the right foundations in place, the opportunity ahead will be limited only by our imaginations. For all of these reasons, Experian welcomes the Government’s goal of making this leap forward for the UK, and we look forward to seeing the detail of the new Data Act as it is released in the coming months.

Two of Experian’s core values – innovation and financial inclusion – are on full display with Experian Boost™ being selected for Fast Company’s 2022 World Changing Ideas Awards, which celebrates the “broadest ideas … that have the potential to affect true systems change.” Experian Boost is a first-of-its-kind service designed to help consumers improve their credit profile and thrive financially. Nearly 9 million people have connected the service to report their on-time utility, telecom, and video streaming service payments. The service tackles inequity and exclusion from the credit economy by enabling consumers to add positive payment history that reinforces their personal financial reliability directly into their Experian credit file, which can potentially boost their credit score instantly. At Experian, we continually focus on expanding credit to underserved communities. Most recently we introduced Experian Go™, a brand-new program that can potentially help the nearly 50 million people in the United States who have a nonexistent or limited credit history. This Fast Company recognition also reflects our purpose and innovative culture focused on creating products and solutions that help consumers thrive, including Experian Boost in the UK and Serasa’s Score Turbo in Brazil. Every day at Experian we are investing in new technologies, talented employees, and innovation to help consumers and our clients maximize every opportunity we have to offer.

With consumers relying more heavily on the digital economy for online shopping, mobile banking, streaming content and other activities, businesses are challenged with recognizing each individual across different devices and channels. The challenge lies with the virtually endless number of touchpoints, attributes and values that can be associated with one’s identity, which is comprised of vast amounts of online and offline, dynamic, multidimensional data. As identities have become more complex, and with the definition of identity constantly evolving, the challenge is now even more pressing. Businesses are applying sophisticated analytics to more accurately identify individuals and create a positive, cohesive customer experience, but it’s critical that they remember: for each consumer – their data and identity are personal. To help companies address consumer recognition, Experian recently unveiled Experian Identity, an integrated approach that incorporates the full breadth of the company’s authoritative data, analytics and technology solutions to help businesses across any industry better connect with their consumers in more personalized, meaningful and secure ways. Experian Identity addresses the need that businesses have to respond to the rapidly evolving identity market with interconnected, scalable technology, products and services that optimize the consumer experience. Building Consumer Trust The key to success for businesses is building consumer trust through the effective use of identity. And that starts with securely managing customer data, while ensuring privacy and regulatory compliance. As a person’s identity evolves over time through major life events, such as opening a first credit card, getting a student loan, buying a car or house, receiving hospital care, or securing a line of credit, businesses must adopt a “customer first” mindset that reinforces their brand and delivers a tailored customer experience. That experience is further strengthened when a business incorporates identity-driven decision-making into every brand touchpoint. By providing a seamless and secure experience, businesses can help consumers prevent fraud and mitigate risk (to themselves and their customers), and build a more holistic view of each individual or small business so they can respond with timely, relevant and fair offers that better address their consumers’ needs.The resulting customer journey becomes demonstrably personalized, responsive, and valued. Constant Innovation Required Identity data sets are constantly growing with inputs from new interactions. Many future sources of data have yet to be even conceived or developed. Staying ahead of the identity market curve is vital, and it requires building and continually evolving an enterprise-scale identity solution that interconnects with your own unique data and systems to create attribute-rich profiles of your customers that work across any identity application. That’s Experian Identity. For more information on how Experian Identity helps optimize identity solutions, visit www.experian.com/identity-solutions and click this link to download the Making Identities Personal white paper.

Simplifying healthcare for all - that seems like a tall task to accomplish considering the last two years. What we once considered simple activities in our daily lives, such as going to the store to buy groceries or getting children to school, was upended by a global pandemic. Factor in the massive changes in healthcare operations, and it is clear the system needs to continue to evolve. It also cements my belief that Experian Health’s mission is even more relevant and achievable today than it was pre-COVID 19. In fact, this aspiration of simplifying healthcare for all is top of mind for me and Experian as we go into HIMSS22, the premier healthcare conference being held in Orlando this week. The healthcare industry has undergone massive changes since the fateful announcements in early 2020. While adapting to the pandemic was a huge undertaking for many organizations at the onset, those who opted to embrace change saw the payoff as they simplified administrative tasks and created efficiencies for both providers and patients. We saw organizations eagerly adopt technology and tools to take paperwork digital, streamlining the patient intake process and improving the accuracy of the data received. Instead of phone calls, patients and providers scheduled appointments and communicated online through secure portals saving time and manpower. The use of telehealth appointments allowed providers to see more patients and do so safely. Who would not want the simplicity of carving out just a few minutes from the comfort of one’s home for a non-urgent appointment? We are proud to have been a part of this evolution helping healthcare organizations pivot in the face of such a daunting predicament. For example, through our digital front door solutions, patients were able to schedule and pre-register for appointments online avoiding extra time spent in waiting rooms. We verified hundreds of thousands of identities quickly as Americans lined up for COVID-19 testing and vaccines. Our mobile payments system served to make the financial aspects of care easier to fulfill. Providers turned to us to help recoup costs from the government and insurers for COVID-19 care with our insurance discovery solution. Experian will not stop here, and we will continue to innovate high-tech, data-driven approaches to simplify healthcare for all; I hope the industry doesn’t stop either in tackling tough operational challenges using the power of technology and data. With this in mind, I look forward to hearing about the lessons learned by the industry as well as future innovations from the participants at HIMSS22. It’s the “can’t-miss healthcare conference of the year,” and we are pleased to be a sponsor and exhibitor once again. For those attending, visit us at Booth #3059. Taking the conference playbook of a hybrid approach with both digital and in-person participation, the healthcare industry should follow suit. Let’s certainly keep valuable in-person mechanisms in place, but not forget about the last two years and the incredible progress made that moved the industry forward. At Experian, we strive to help clients operate more quickly, smoothly and efficiently across the healthcare journey. With a new mindset in the industry and the tools available to act on change from providers like Experian, simplifying healthcare for all is not just a mission but an outcome we must achieve. Tom Cox is President of Experian Health.

As a leading information services company, some of our chief priorities include protecting and ensuring the accuracy of consumer information. The integrity of our data is critical and aligns with our efforts to advocate for financial inclusion for everyone. Data accuracy is particularly relevant for the transgender and non-binary community with regard to name changes. It’s important to note that information about gender/sex, age, race, ethnicity, religion or sexual orientation is not included in credit reports or scores. However, when someone transitions, and changes their name, their credit and financial history may still be tied to their birth name, which is also referred to as their “deadname.” This can unintentionally “out” the consumer or force them to establish a new credit history. At Experian, we have a process through which those who identify as transgender and non-binary can provide legal documentation to prove their identity without the negative emotional and financial impact. You can learn more about this process here. When you affirm your identity and update your name, Experian will also suppress your deadname so it does not appear on your Experian credit report. Taking these steps only changes your name on your Experian credit reports, and you may need to inquire about the process with other credit bureaus. Fair access to credit tools is part of our mission, as is providing these services with dignity and respect. At Experian, this is our purpose, advocating for all communities and people. This is financial inclusion.

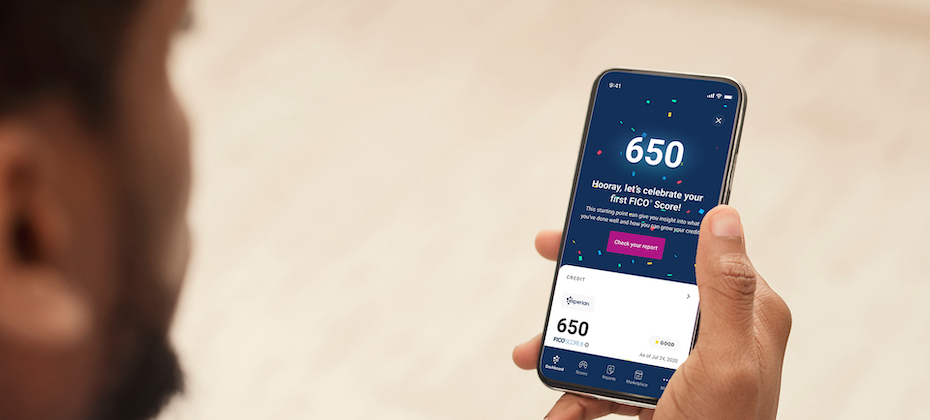

For the past several years, we’ve been on a journey to improve financial access for millions of people around the world. We’ve made it our job to help consumers get the best financial outcomes. This focus on consumers defines us and informs everything we do. In 2019, we reshaped how consumers access credit with Experian Boost™. Since then, nearly 9 million consumers have connected to the product. While we are proud of what we have and continue to accomplish with Experian Boost, we know there is more to be done to ensure more consumers can access fair and affordable credit. Improving outcomes for underserved consumers When credit is used responsibly, it can create new opportunities from getting a college degree, buying a car or home and starting or expanding a business. These are milestones that help people establish careers, build wealth and ultimately achieve greater financial freedom. Yet, there are millions of consumers who are unable to participate in the mainstream financial ecosystem today because they don’t have a financial identity. In fact, our recent research shows there are at least 28 million credit invisibles in the U.S. with an additional 21 million consumers who are unscoreable by the credit score models most used by lenders today. Without an established credit history, these consumers struggle to qualify for everything from an auto loan to a mortgage and even an apartment or employment. This problem more frequently impacts communities of color with 28 percent of all Black and 26 percent of all Hispanic consumers currently unscoreable or credit invisible. Increasing financial inclusion depends on creating opportunities for underrepresented consumers to succeed. And this starts with ensuring all consumers have a financial identity. Bringing financial power to all with Experian Go The challenge is many consumers who are not in the credit ecosystem today are unsure where to start. Today, we reached a pivotal and exciting milestone in our commitment to consumers with the launch of Experian Go™. This new program opens the front door to the financial ecosystem for millions of consumers by helping them establish their financial identity and move from credit invisible to scoreable. Within minutes, credit invisibles can have an authenticated Experian credit report, tradelines and a credit history by using Experian Boost™[1], and instant access to financial offers through Experian Go. In fact, early analysis shows 91 percent of consumers with no credit history who connect to Experian Boost, a free feature that allows users to contribute their on-time cell phone, video streaming service, internet, and utility payments directly to their Experian credit report, can become scoreable in minutes with an average starting near-prime FICO® Score of 665[2]. Throughout the experience, we’ll provide ongoing credit education and access to tools like Experian Boost™ to make it easy for consumers to learn how to use and responsibly grow their credit histories. Until now, our industry has struggled to verify the identity of credit invisibles. Over the last several years, we’ve introduced new identity verification technologies to our toolbox. With Experian Go, we’re leveraging these technologies to verify a credit invisible’s identity and get them in the front door to start building credit. No other credit bureau or organization is doing this today. During our pilot, we helped more than 15,000 consumers establish their credit history. This is a great start. Now that Experian Go has launched, I look forward to helping millions more consumers get the credit they deserve. To learn more about Experian Go, visit www.experian.com/go. [1] Results may vary. Some may not see improved scores or approval odds. Not all lenders use Experian credit files, and not all lenders use scores impacted by Experian Boost. [2] Experian analysis based on an anonymized and statistically relevant sample of consumer credit reports with only Experian Boost tradelines included and FICO® Scores. December 2021.

The past few years have sparked a swift digital transformation that subsequently drove a rapid increase in fraud. In fact, fraudsters have gotten more creative, putting businesses and consumers at risk now more than ever. At Experian, we predict that more intricate challenges lie ahead and are dedicated to helping businesses combat fraud threats. Here’s what we expect in 2022: 1. Buy Now, Pay Never – The Buy Now, Pay Later (BNPL) space has grown massively recently. In fact, the number of BNPL users in the US has grown by more than 300 percent per year since 2018, reaching 45 million active users in 2021 who are spending more than $20.8 billion . Without the right identity verification and fraud mitigation tools in place, fraudsters will take advantage of some BNPL companies and consumers in 2022. Experian predicts BNPL lenders will see an uptick in two types of fraud: identity theft and synthetic identity fraud, when a fraudster uses a combination of real and fake information to create an entirely new identity. This could result in significant losses for BNPL lenders. 2. Beware of Cryptocurrency Scams – Digital currencies, such as cryptocurrency, have become more conventional and scammers have caught on quickly. According to the FTC, investment cryptocurrency scam reports have skyrocketed, with nearly 7,000 people reporting losses totaling more than $80 million from October 2020 to March 2021 . In 2022, Experian predicts that fraudsters will set up cryptocurrency accounts to extract, store and funnel stolen funds, such as the billions of stimulus dollars that were swindled by fraudsters. 3. Double the Trouble for Ransomware Attacks – In the first six months of 2021, there was $590 million in ransomware-related activity, which exceeds the value of $416 million reported for the entirety of 2020 according to the U.S. Treasury's Financial Crimes Enforcement Network . Experian predicts that ransomware will be a significant fraud threat for companies in 2022 as fraudsters will look to not only ask for a hefty ransom to gain back control, but criminals will also steal data from the hacked company. This will not only result in companies losing sales because of the halt caused by the ransom attack, but it will also enable fraudsters to gain access and monetize stolen data such as employees’ personal information, HR records and more – leaving the company’s employees vulnerable to personal fraudulent attacks. 4. Love, Actually? – Because more consumers went on dating apps and social media to look for love during the pandemic, fraudsters saw an opportunity to create intimate, trusted relationships without the immediate need to meet in-person. The FBI found that from January 1, 2021 — July 31, 2021, the FBI Internet Crime Complaint Center received over 1,800 complaints, related to online romance scams, resulting in losses of approximately $133 million. Experian predicts that romance scams will continue to see an uptick as fraudsters take advantage of these relationships to ask for money or a “loan” to cover anything from travel costs to medical expenses. 5. Digital Elder Abuse Will Rise – According to Experian’s latest Global Insights Report, there has been a 25 percent increase in online activity since the start of Covid-19 as many, including the elderly, went online for everything from groceries to scheduling health care visits. This onslaught of digital newbies presents a new audience for fraudsters to attack. Experian predicts that consumers will get hit hard by fraudsters through social engineering (when a fraudster manipulates a person to divulge confidential or private information) and account takeover fraud (when a fraudster steals a username and password from one site to takeover other accounts). This could result in billions of dollars of losses in 2022. As a leader in fraud prevention and identity verification, Experian offers a full suite of automated tools that harness data and analytics to prevent fraud and mitigate losses. Learn more about Experian's fraud management tools.

In the early 1960s, Simon Ramo had a vision of a cashless society made possible by information and technology. This vision led to the creation of our business in North America. Ramo believed information could change the way people lived. Today, we know this to be true and continually see the ways data and technology can create enormous good in the lives of millions of consumers. While much has changed since the 1960s, Ramo’s vision holds true and continues to fuel the way we work at Experian. These principles have put consumers at the center of our business, which has forced us to think outside the box and do things differently. Let me give you an example. Until 2019, consumers had never been able to contribute information directly to their credit report. When we launched Experian Boost, we fundamentally changed the game. We put consumers in the driver’s seat and empowered them to contribute their on-time bill payments directly to their Experian credit report. By doing so, we’ve helped millions of consumers instantly improve their FICO® Score. This was a game changing move that is making a tangible difference for consumers. In fact, Experian Boost users have accessed more than $1.7 billion in credit due to improved credit scores. While we are proud of what we continue to accomplish with Experian Boost, we know financial inclusion depends on all of us doing more. On all of us doing things differently. We recently released new research in partnership with Oliver Wyman which shows 106 million Americans, or 42% of the adult population, lack access to mainstream credit because they are credit invisible, unscoreable or have a subprime credit score. Communities of color are more likely to lack access to mainstream credit, with 28% of Black and 26% of Hispanic consumers unscoreable or invisible, which is perpetuating historic disadvantage. While we have made a lot of progress in recent years by incorporating new data in decisions, as an industry, we can and must do better to ensure all consumers have access to fair and affordable credit. The old way of doing things, the old tools, will not work to ensure more consumers can access the financial services they need when they need them. The score models historically used by lenders are leaving nearly 50 million Americans behind. We need better data and better technology to help more consumers. When advanced analytics and machine learning are combined with expanded data sets as they are with Experian’s Lift Premium™ score, 96% of the population can be scored, including an estimated 65% credit invisibles and the entire conventionally unscoreable population. This is significantly greater than the 81% of consumers that can be scored by conventional scores today. Scoring 100% of Americans and expanding fair access to credit to creditworthy consumers is our goal. This is an exciting time as we are nearing a point where we can say, no matter who you are, where you live or what part of your financial journey you’re on, we can score you and help you access the financial services you need. We can’t do it on our own. Financial inclusion depends on industry adoption of these new tools and insights. As we begin a new year, I believe the financial services industry is at an inflection point. And I am hopeful. I think we can all agree it’s time for a new way of doing things and today we have the tools available to make it happen.

It’s a privilege to be recognized for a cause that’s important to so many of us at Experian. I am honored to be awarded a bronze Stevie® Award in the “Women Helping Women – Business” category for supporting women in Decision Analytics (DA) and overseeing our employee resource groups across DA. The award specifically calls out our long-standing Accelerated Development Program (ADP), which identifies and mentors women business leaders within our organization The Stevie Award trophy is one of the world's most coveted business prizes, representing more than 60 countries. The awards have been given to small, medium and large businesses for an array of categories since 2002. In 2018, HR Director Richard Teague and I helped launch ADP, which has identified 44 mid-career, high-potential women on the Global Decision Analytics team in a leadership training program. Around half of the women who participate have been promoted within two years. The ADP program also complements our DEI initiatives, which includes our five employee resource groups that have played a valuable connecting and our engagement our team members during both the pandemic and personal challenges. If you would like to find out more about any of the GDA DEI networks, including how you can get involved, please contact the relevant network lead: Mental Health – Chris Fletcher Disability and Neurodiversity – David Bernard LGBTQ+ - David Gallihawk Gender Network – Marika Vilen or Jen Cosgrove Race and Ethnicity – Shri Santhanam