Tech & Innovation

At Experian, we are continually innovating and using technology to find solutions to global issues, modernize the financial services industry and increase financial access for all.

DEI

Our deep commitment to social and financial inclusion is reflected in our workplace culture, our partnerships and our efforts to break down the barriers to financial equity.

Financial Health

Our initiatives are dedicated to getting tools, resources and information to underserved communities so that consumers can best understand and improve their financial health.

Latest Posts:

On Tuesday, Experian held a press conference and ribbon cutting ceremony with San Diego Mayor, Kevin Faulconer to announce and celebrate the expansion of the data and innovation lab in North America.

Experian has expanded its growing North America DataLabs in San Diego to further innovation and enable leading data scientists to help clients and businesses solve strategic marketing and risk management problems through advanced data analysis processes, research and development.

Experian Marketing Services released its 2016 Digital Marketer Report. The eighth annual study reveals the challenges, priorities and other key issues impacting marketers worldwide.

![[Infographic]: Off-lease Vehicles Surge Back into the Market](http://www.experian.com/blogs/news/wp-content/uploads/2016/04/Feature-Leasing-Image1.png)

As automotive leasing trends to new heights, a rapid influx of off-lease vehicles are returning to market. Experian Automotive’s latest infographic explores the surge in off-lease vehicles, including which models and vehicle segments are most popular.

Tru Optik, the only audience measurement and data management platform built for OTT and Connected TV, has partnered with Experian Marketing Services to offer a service providing real-time census-level viewer data for over-the-top (OTT) TV programs and ad exposure across all screens. Tru Optik clients will be able to measure and segment content and ad exposure based on lifestyle, demographic and purchase behavior powered by Experian’s ConsumerView marketing database.

Tru Optik, the only audience measurement and data management platform built for OTT and Connected TV, has partnered with Experian Marketing Services to offer a service providing real-time census-level viewer data for over-the-top (OTT) TV programs and ad exposure across all screens. Tru Optik clients will be able to measure and segment content and ad exposure based on lifestyle, demographic and purchase behavior powered by Experian’s ConsumerView marketing database.

In recent years, leasing has strongly returned as an option for consumers to choose when looking to get into a new vehicle and maintain an affordable monthly payment. Experian Automotive’s latest infographic examines the lift in leasing, as well as key attributes in the auto finance market.

Experian had the honor of celebrating innovative achievements in marketing with a few of our superstar clients at the 2016 Marketing&Tech Innovation Awards presented by Direct Marketing News and The Hub. The second annual awards program honors achievements in marketing leveraging data and technology. Three Experian Marketing Services’ client programs were recognized for their innovation in analytics, email marketing and omnichannel marketing.

Experian had the honor of celebrating innovative achievements in marketing with a few of our superstar clients at the 2016 Marketing&Tech Innovation Awards presented by Direct Marketing News and The Hub. The second annual awards program honors achievements in marketing leveraging data and technology. Three Experian Marketing Services’ client programs were recognized for their innovation in analytics, email marketing and omnichannel marketing.

Experian identified e-commerce fraud attacks across the United States for both shipping and billing locations among all states and ZIP Codes.

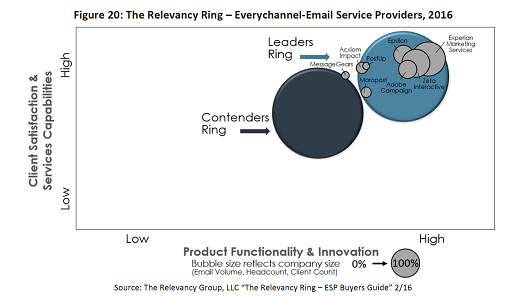

The Experian Marketing Suite is recognized by The Relevancy Group for its innovative technology and functionality, offline and addressable TV solutions for marketers.

The Experian Marketing Suite is recognized by The Relevancy Group for its innovative technology and functionality, offline and addressable TV solutions for marketers.