Test Business Information Page

New Report: Will the 2023 holiday season hinge on generosity? The latest Beyond the Trends report offers evidence it may.

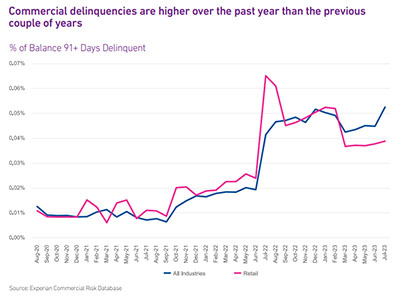

The labor market remains robust with low unemployment (3.8%) and 366K new jobs created in September. Job openings in the U.S. were 9.6MM as of the end of August, an increase of 690K or 5.8% since July. Retail sales in August had a month-over month increase for the fifth consecutive month. As we head into the holiday shopping season, despite headlines of large retailers struggling, the retail industry appears poised for success. It is likely that those retail businesses that survived the difficulties of the pandemic are the most financially sound and are driving the statistics. Over the past year, retailers are seeking less credit and taking on less debt than the previous few years. Despite inflation, consumers are still spending, and retailers are benefitting. Commercial delinquencies have been increasing over the past year. Delinquencies within the retail sector were trending above overall commercial delinquencies until just a few months ago when retailers exhibited lower rates than overall. These are all positive signs heading into the holiday shopping season which tends to make or break a retailer’s year. The September labor report was stronger than expected. Unemployment remained low at 3.8% and 366K new jobs were created which was the highest amount since January. In addition, the jobs created in July and August were revised upward significantly. What I am watching: With the labor market still tight, it will be interesting to see if the retail sector will be able to staff accordingly to support the holiday crunch. If staffing is difficult, retail stores may struggle to keep up with demand. Now that the student loan moratorium has ended, it will be important to monitor the impact to consumer spend. The increased expense of the student loan monthly payments will likely leave individuals with less discretionary income to spend on retail purchases. In addition, business owners who have student loans will have less money to invest in their business

These uncertain economic times are challenging for credit managers. Learn about the benefits of a holistic portfolio management approach.

Now that most worldwide travel restrictions have been lifted, the industry is rebounding. It appears that travel businesses relied on more commercial credit to weather the storm of the pandemic and raised prices to help recove

Catch the latest brew on fraud strategy at our 15-minute Sip and Solve session hosted by Bonnie Gerrity, sharing best practices over coffee.

Small businesses have been opening at record rates during and following the pandemic. With so many new businesses seeking capital, and not all of them borrowing with good intentions, Experian thought it would be a good time to talk about mitigating fraud with one of the leading FinTech lenders. Ryan Rosett is the Founder and Co-CEO of Credibly, and he shares several valuable insights with us in this Business Chat. Watch Interview What follows is a lightly edited transcript of our interview. Gary Stockton: Hello, and thanks for joining us for this business chat. I'm Gary Stockton from Experian Business Information Services, and I'm here with our Vice President, Dominic DiGiuseppe, and also Ryan Rosett, the founder of Credibly, a fintech dedicated to helping medium and small-size businesses grow via funding decisions that are based on the holistic health and potential of a business.And we're here today to discuss fraud as it relates to FinTech in the small business space. Gentlemen, welcome to Business Chat. So Experian has recently released some interesting new statistics on the impact of fraud across several industries, notably that over 39% of recent FinTech inquiries were rated as high risk by our commercial first-party fraud score.And that's a predictive score that can predict the likelihood of first-party payment default and the credit bust-out scenarios that we see. These inquiries are projected to carry 62% of all first-party fraud risk within the population. And if you would like to see more on that analysis, we'll be including a link in the blog post for this business chat.So Dominic, I wanted to get your reaction to this statistic, given our mission to serve small businesses and considering small businesses make up the greater part of our economy and economic output.Dominic DeGuiseppe: Yeah, Gary, thanks for that. First and foremost, I want to give a shout-out to our data sciences and product teams for being able to continue to innovate in this space.But really, when you look at post-pandemic, the amount of businesses that have been created, it's, we were somewhat surprised by the numbers as well. But the amount of businesses that are being created, the mission that we have an experience making sure that we can help provide capital and we can provide funding and get that into the hands of business owners quickly.So if we take a look at some of the trends here, the amount of businesses that are being formed since the pandemic is pretty surprising. We've continued to see that trend. Rise and stabilize a bit, but it's still much higher than pre-pandemic levels. So when you think about businesses that are looking to understand the type of fraud that's being perpetrated or making sure that these types of businesses are actually legitimate as they're looking to make credit decisions and provide these companies with lending or funding decisions, these are the types of tools that have been that the team has been creating. Rapid new business formation during pandemic To make sure that we're assessing and helping folks determine the levels of risk that are associated with these businesses. I know we've talked about this in the past, a few times in different conversations, but can you tell the folks tuning in here a little bit about the Credibly origin story I find it super unique and interesting.Ryan Rosett: Oh, absolutely. So my partner and I started the business in 2010. If you think about 2010, it was a contrarian time to start a business. It was coming out of, the Great Recession of 2008/2009, and they were always talking about this double-dip recession, but it was actually an opportune time to start just because small businesses were really looking for access to credit.And what we are is that we're a cash flow lender. So, we look at the cash flow and make decisions and determinations in a very quick manner to provide working capital at an affordable rate for the customer. So that means, it's important to us that the business can sustain the payments that we're providing, and we can maximize the amount of money working capital that we can give them.So it's just something that we're focused on, and we've had the wind in our back for a, I would say, eight years. And then there's something called the pandemic hit, which was like, which, I didn't sleep for, I don't know, four months. But it was a period of time that was really like an interesting time for a small business lender, but then recognizing also that the government money really boosted up the small businesses, and it worked well for alternative lenders like ourselves.Gary Stockton: The pandemic did accelerate rapid digitization, and it does seem like an opportunity for FinTechs to address lending for small businesses digitally. This stat that we were talking about, it's really quite astounding that there were that number of businesses that sprung up during the pandemic.It makes a lot of sense, though, when you consider there were quite a lot of people that were transitioning from maybe a different industry into another industry, home businesses springing up. But with so many new businesses coming online and the impact of cybercrime on small businesses, Dominic, how do lenders know whether or not they are dealing with a real business when they onboard new customers digitally?Dominic DeGuiseppe: Yeah, I think that's certainly a challenge. And I think one of the things that we're looking to answer is, really, three things — is the business real? Is the business active? And is the applicant that's applying for the loan or the type of funding are they actually linked to the business?I think we can certainly answer for that, but I think, since we've got one of the top FinTechs in the space out there, Ryan what is Credibly doing to understand different fraud trends and combat what's happening within the space with fraud?Ryan Rosett: What I can say is that fraud is pervasive right now. And, as we're an online lender, we make decisions in under four hours from app to decision and fund same day. The amount of data alternative data that we're pulling in to make decisions is really quick. And so the risk that there's a fraud application coming through is something that we that you know, I'd say that's largely what we work on.I would say the three largest fraud patterns that we're seeing and you addressed earlier, was an application mismatch. Which is against the verified sources that they listed. And then, we also have just altered documentation associated with the bank statements.And again, that would be something that would be illegal historically, but we're a nonbank lender. And we're just trying to make decisions based on the data that we have. And we want to verify that the applicant is the owner of the business. So those are the types of frauds that we're seeing, I'd say, like a high level and then there are certain things that we do to combat that.So we will call it stipulations to fund. So we may offer to make an offer subject to them supplying additional information. Maybe it's the articles of a corporation. Maybe it's a tax return. And oftentimes, it's not to say whether you're profitable or not profitable, we're looking at who's the owner, who's getting K1s on the tax returns?Those are examples of things that we are looking at. And I know Experian has been an excellent partner of ours in terms of matching and using a number of different data sources that you provide.Dominic DeGuiseppe: How have you seen fraud evolve pre-pandemic to post-pandemic and continue to take shape and take a different shape, from what's been happening as to now?Ryan Rosett: Yeah, that's a good question. So on a pre-pandemic basis today, we're back to the same level of losses. Okay. But the fraud is becoming a little bit more advanced. Okay. Whether it's be it through cyber attacks, whether it's online applications, there's a number of different things that we're working on that we're constantly combating. So it's not it's not something that we put a fix in and then we move away. It's something that we're constantly evaluating, whether it's a submitting partner, or whether we have an affiliate that provides a certain number of lead applications.Those are things that we're constantly measuring to see what the loss rates are, where the fraud is coming from, and then making decisions. So from a pre-pandemic to a post-pandemic, I'd also say that with the PPP, small businesses got a taste of working with alternative lenders through the PPP process, and they became a little bit more comfortable with working with lenders similar to Credibly. So you're seeing like a little bit more comfortability with small businesses having the ability to interface with us and then they're layering in fraud and things of that nature. So it's a constant something we're combating on a daily basis, and it's something that we're thinking about, very often.Dominic DeGuiseppe: Yeah, because when you start to look at it and all the new businesses that are being formed that are coming into the market, working with alternative lenders and FinTech's like yourself, and you guys continuing to shorten the cycle around the app to approval and all the data points that are coming into it. You guys are different than a bank and are able to do those types of things and move quickly. So obviously, with that comes some additional risk; with the FinTech community being tight-knit, how have you been able to benchmark what Credibly is doing against some of the peers that you guys work with in the industry?Ryan Rosett: We have and that's really through public data through asset-backed securitizations; there's reporting relating to the losses that each lender is seeing, of our losses, approximately 10% of our losses we attribute to fraud. The other 90% is, it could be a business that legitimately goes out of business, which happens. So, it's not necessarily fraud. We do benchmark it based on some of our competitors that have asset-backed securitizations and we see the performance in their loss rates and charge costs and things of that nature.Gary Stockton: So, what are you seeing in terms of an amplifying effect on fraud rates with generative AI in the mix and allowing for spoofed content and more access to triangulated private information on business entities?Ryan Rosett: You know, that's a great question. One thing, you're seeing fraudulent IDs. You're seeing IDs that are becoming a little bit more difficult to track and see, because they're creating an identity of someone and they're able to do that through gen AI.So that, that's one aspect. You're also seeing bank statements. We use a number of different bank statements, parsing, and machine learning that looks at these bank statements. It's looking at font type size. There are a number of things when somebody is attributing and oftentimes, sometimes the fraudster is making grave errors also. They're putting data in where data wasn't supposed to be. You're able to detect that really quickly and that's on an automated basis. So that doesn't even touch a human. We see fraud, we kick it out. And, it's declined. So it's a, it's, when we see a, when we fund a fraud application and it's noted as a fraud that we've determined fraud, we then report it we have a, there's a data matching system that we report into so that business owner would never be eligible for. Business financing through an alternative lender. Again,Gary Stockton: Dominic, any closing thoughts?Dominic DeGuiseppe: Yeah, Gary, I would say just in terms of, generally speaking, fraud continues to evolve. There's a number of different things that we're looking at from a business perspective to be able to help our partners. But, Ryan's pointed out a number of those things today, but as FinTechs continue to evolve, fraudsters will continue to evolve and Experian is on our journey to continue to help understand how we can benefit our business partners, making sure that they can combat fraud and keep it out of the business.Gary Stockton: That's great. I think that's a great place to leave today's chat. Dominic, and Ryan, thank you so much for taking time out to share your perspectives on fraud in the commercial space on Business Chat. Thanks for watching, everyone. Related articles:

This post highlights recent commercial fraud insights from Experian and the advantages of taking a multi-layered approach to fraud strategy.

Since the height of the COVID-19 pandemic, the commercial real estate market is experiencing a paradigm shift as office professionals acclimated quite well to working from home, and many balk at going back to the office. As vacancy rates for offices hit record highs, supply of office space is greater than demand, reducing the value of many commercial properties. In parallel, The Federal Reserve’s 500bps of interest rate increases since March 2022 have made it more expensive for property owners to borrow and has left commercial real estate (CRE) lenders fearing greater risk of default will occur in the near future. August unemployment increased to 3.8% from 3.5% in July and is the highest since February 2022. Low unemployment continued to drive wages up with August wages reaching $29 per hour In anticipation of higher losses, CRE lenders are tightening their lending criteria, requiring higher down payments, shortening the loan term, and selling off or diversifying their CRE portfolios. Contrary to recent trends in office space pricing, and also contrary to impressions driven by media coverage focusing on increasing mall vacancies and mall closures, retail real estate appears to be rebounding since the pandemic. The average monthly rent per square foot for retail space has been increasing across the United States since the start of the pandemic. What I am watching There has been interest in re-purposing vacant commercial spaces into multi-family rental properties. As vacancies rise in office buildings and in some large urban malls, more CRE buildings are transitioning to hybrid residential/commercial spaces. A significant increase in residential living spaces should drive housing costs down, which would be a tremendous benefit to the public and help curb inflation. The labor market remains resilient but there are signs of weakening. While unemployment remained low at 3.8% in August, it is the highest since February 2022. The three-month moving average of jobs created in the U.S. declined to under 150K for the first time in a few years. If the labor market continues to weaken, employees will have less bargaining power and it is possible that employers will require workers to come back to work in-person in offices full time. If that comes to fruition, CRE owners and lenders will be in a much better position. Download Full Report Download the latest version of the Commercial Pulse Report here. Better yet, subscribe so you'll get it in your inbox every time it releases, or once a month as you choose.

Since the height of the COVID-19 pandemic, new businesses are opening at a record pace. New businesses tend to be smaller based on number of employees as well as annual revenues. While new businesses make up a greater portion of new commercial credit accounts, they receive less credit.

Recession fears may be calming, but several indicators are still flashing for 2024. Experian and Oxford Economics have released the Q2 2023 Main Street Report, the report brings deep insight into the overall financial well-being of the small-business landscape, as well as provides commentary around what specific trends mean for credit grantors and the small-business community. Report Summary During Q2, lenders adjusted underwriting criteria to limit exposure as delinquencies remained elevated for consumers and small businesses. The markets dealt with inflation above target and customers reevaluated their discretionary spending and growth investment strategies. Not all segments of the markets were impacted by environmental forces. Technology-focused companies are leading investment and growth, while logistic, utility, and healthcare struggle, Supply chain disruptions are smoothing, but lighter forecasted demand is already impacting inventory reorders. The softer demand is hitting trucking and logistic companies hard as tonnage, and mileage are lighter than forecasted as consumers return to the in-person experience and engage with eroded purchasing power. The bright spot is consumer resiliency. This prolonged spending strength is fueled by a tight labor market, wage growth, and relief in energy and food costs.Another element is savings. Dwindling savings, increased reliance on unsecured debt to support spending behavior, reassumption of monthly debt servicing obligations (student loan payments), and prolonged inflation place downward pressure on the consumer. Recession fears may be calming, but several indicators are still flashing for 2024. Download Q2 2023 Main Street Report

The Federal Reserve’s efforts to tame inflation with aggressive interest rate hikes over the past 15 months appear to be working with July’s core inflation rate reaching the lowest level since October 2021. The U.S. labor market remains strong with low unemployment and 187K knew jobs created in July. As inflation eases and the economy continues to be strong, it is becoming more likely that we could experience a soft landing.

Gain insight on small business credit conditions by attending our quarterly webinar.

The aggressive interest rate hikes instituted by the Federal Reserve over the past year and a half may have achieved the desired goal. Easing inflation (3.2% in October) and strong GDP growth (4.9% in Q3) are some of the first indications that the economy may experience the “soft landing” hoped for instead of a recession. The consistently strong labor market produced low unemployment and increasing wages, enabling personal spending to increase. However, while spending continues to grow, the growth rate is on a downward trend. The high rate of spending has been driven by consumers digging into savings and borrowing more. As savings dwindle and the cost to borrow increases, it is likely that consumers will retreat and the pull-back will likely hit discretionary categories first. What I am watching: Heading into the holiday season, consumer spending is still strong but how long will it last? The National Retail Federation is projecting that November and December retail sales will grow 3-4% which is in line with the 3.6% average increase from 2010-2019 but lower than the past three years. People are already dipping into savings and borrowing more to continue their consumption but that well will run dry at some point. In addition, 36% of consumers cite December is a month for seasonal financial distress, according to PYMNTS. While consumers may continue spending through the holiday season, the tide may turn in early 2024 when bills hit with higher interest rates. Download Full Report Download the latest version of the Commercial Pulse Report here. Better yet, subscribe so you'll get it in your inbox every time it releases, or once a month as you choose.

If you want to get the most out of your marketing campaigns, it's important that they are tailored for a specific audience. We invited Tony Romero on Business Chat to talk about part two of his three-part Sip and Solve webinar series focused on B2B marketing where he explains how segmentation and targeting can make all aspects (landing page or email) more effective by using industry SIC as well as NAICS codes. Look-a-like analysis CMO's challenged with restricted budgets Analyzing portfolio diversity and targeting minority-led, women-led businesses Profiling prospects with limited data attributes Watch Our Interview What follows is a lightly edited transcription of our talk. [Gary Stockton]: So in our last chat, we talked about maintaining robust marketing data to power effective campaigns and how clean data really helps businesses conduct effective marketing campaigns. This week, we switch gears to discuss the power of segmentation and targeting using industry SIC and NAICS codes to optimize your marketing budgets. So let's dive in. In our previous chat, we spoke about the changes that tech companies have enacted to make the job of targeting business prospects harder, but it's not game over for marketers. [Tony Romero]: No, definitely not. You know, it's really important to know that there's still a lot of a wealth of data out there that can be used to identify and segment target customers. You know, the first-party data obviously is really key, as well as being able to take information that may be spotty. If, for example, you only have a name or address, you can be able to through services like ours, be able to get a full, comprehensive set of data on that customer, both firmographic, demographic, and credit information, and then be able to use that to promote to customers. [Gary Stockton]: So can you share some examples of how Experian data can help marketers hone in on their target customer, for example, how SICs and NAICS codes can help? [Tony Romero]: Yeah, Gary, you're right. SIC and NAICS codes provide information about what industry the business is in. And so, by knowing that, you're able to target those consumers. So again, as I mentioned before, you can take a look at your existing customer base and find out who's your ideal target customer. And from that, then you can compare that to prospective businesses that look just like that. And that's what's called a lookalike analysis. And by using SIC and NAICS codes, you're able to use that to segment the market and then be able to promote effectively. And Gary, you also mentioned that with the economic state, CMOs have to watch their budgets and be as efficient as possible these days. So again, by doing very good segmenting of your target audience, you are making sure that your finance and financial output to a campaign are as efficient as possible. [Gary Stockton]: Excellent, regulators, they're focusing on diversity, equity, and inclusion. How can Experian help clients in that effort? [Tony Romero]: You know? Yeah. That's a very key point and definitely more than ever. It's important to focus on identifying your existing portfolio and seeing how many customers in your portfolio are minority-led or women-led businesses. So you can do benchmarking, you can see how you fare against other businesses in your market space. And that helps you to determine how much more do you need to market to these minority or women-led businesses. So what's number one is the benchmarking, but secondly, you need to be able to go out and look at your prospective target list and find out who are minority-led or women-led. And there, getting an indicator about a Woman-led or Minority-led business allows you to promote specifically to those types of businesses to help increase your portfolio. [Gary Stockton]: That's good. So if all I have is a name and an email address, and in a lot of cases, you know, if we're driving a newsletter, can I still profile this contact? Or are there other ways to do that with minimal info? [Tony Romero]: Yes, there is. You know, even just having a name and address is enough data to go through our type of service and be able to append all of the other information that we talked about, whether it's firmographic with SIC or NAICS codes, it could be demographic information where we look at the business and find out who the consumers that are tied to that business are? So that's called a B2C linkage. And from that now, you know who the actual individual is and go target those specific individuals. So that's also another key point to bring out [Gary Stockton]: Excellent stuff, Tony. Well, folks, if you enjoyed this chat and want to go a level deeper, don't miss Tony's campaign targeting Sip and Solve webinar – Fine Tuning B2b Campaign Targeting. He goes into greater detail on targeting B2B prospects, just click the image to be taken over to the recording.

We’re talking B2B marketing data hygiene with Tony Romero from our product team today on Business Chat.

Experian can be your trusted provider to supercharge B2B marketing campaigns with powerful data, analytics and consulting services.

As data privacy regulations become more strict and tech firms implement change, we share how marketers can remain effective while remaining compliant.

Experian Business Information Services recently introduced a powerful new marketing platform called Business TargetIQ. Product Manager, Kelly DeBoer answered a few questions about the product and described use cases that promote greater collaboration between credit and marketing departments. What does Business TargetIQ do? Business TargetIQ is our new marketing platform so it's a B2B marketing platform where clients can access data for marketing applications. How is it different from other business marketing platforms? It is unique in that it not only includes your standard or core firmagraphic information but also includes Experian's credit attributes. Does it have credit data? What does that mean to marketing or collaboration? Typically marketing data and credit data are housed in separate silos of information. With this tool the information will be combined together which will allow the tool not only to be used in traditional marketing applications for targeting but can also be in that risk factor which applies to different divisions within our client's applications or use cases of the data. Who would most benefit from Business TargetIQ? The thing about Business TargetIQ is it truly applies to all different verticals, as well as all different contacts within the company. So whether it's a financial vertical or a trade vertical, retail, just across the board all clients can utilize this. Anybody that's doing marketing can utilize this platform. What core problems does Business TargetIQ solve? It solves a lot of different problems, so, the most common client issues that are brought to our attention are gaps in data, as well as in the marketing initiatives. So they may have data in-house but they have holes within the data. Our tool will allow them to not only upload their client records and fill in a lot of those gaps that they may have, whether it be contact information, or firmagraphics or address information. It will standardize that data and fill in those gaps. But will also provide the means to again use that data. Our business database which has over 16 million records. They can then utilize that information for prospecting, for data append, for analytics, for research applications, so it solves a lot of problems with regard to marketing and data concerns. How does credit data help with prospecting? So what we find is clients come to us and they may say you know I have an idea of what our clients look like, they're in this SIC or in this industry code, or they have this sales volume or employee size, but what they may not know is on the back end which really helps identify and target those businesses is the credit attributes, so the risk factors around those. So do they have delinquencies in their payments? Have they filed bankruptcies? Do they have UCC filings? So it allows them to take it that next step and not only really define what their clients look like, but identify clients that look like that. Learn More About Business TargetIQ

So you’ve created the perfect campaign with great creatives and an unbeatable offer. You deploy the campaign and sit on the edge of your seat waiting for all the leads to flood in. After a couple of days, you notice a couple of responses but nowhere near the volume of what you were hoping for, and you’re stuck asking yourself “why?” Here are a couple of hypotheses: 1.) the people you reached out to aren’t the right audience so they don’t care about your offer, or 2.) your target audience didn’t see your efforts because you used the wrong channel. The process of finding new business customers can be expensive and sometimes unpredictable, but it doesn’t have to be. Here are 3 tips to help improve your prospecting efforts: Tip #1: Define your ideal customer One of the most fundamental ways you can help grow your current customer base is to have a clear understanding of what they actually look like (or defining what they should look like). What’s their job title? What are their biggest business challenges? Are they web savvy? How do they prefer to get industry news? Addressing discovery questions like these allows you to better understand who you’re talking to and how to talk to them. Additionally, you’ll be able to use this profile to help you mimic your best customers and target look-a-likes. Tip #2: Target new businesses Get your products/services in front of new businesses before your competitors. Not surprisingly, many marketers overlook targeting new businesses because of the lack of data — how do you know a new company is in business? How do you know if they’re the right business for you to even target? Fortunately, there are many services in today's market that can help fill in the gaps. Using something like Experian’s US Business Database, which is a database of more than 16 million active U.S. companies, can help you discover new businesses sooner and beat out your competitors to reach them first. Tip #3: Find the decision-makers Identifying the right businesses to target is important, but ensuring that your offer gets in front of the right person – the decision maker – is even better. By finding the decision maker and directing your marketing efforts towards them, you can rest assure that your message lands in the hands of the person that matters most. Want to take it one step further? Once you know who you’re talking to, you can tailor the message and offer to be more relevant for that specific audience, which ultimately helps increase your chances of getting a response. Finding and reaching new business customers can be a daunting and expensive tasks, especially if you don’t target your prospecting efforts. Be sure to keep these tips in mind when approaching your marketing strategy and don’t let today’s data challenges hold you back. Learn more about Experian's US Business Database or our other marketing capabilities.

I had the pleasure of speaking with Kelly DeBoer recently. She is a Product Manager at Experian working in Business Information Services. Kelly leads product strategy for our business marketing products. In this Business Q&A we talk about B2B marketing trends and how Experian is helping business clients get the most out of their marketing initiatives. Gary: B2B marketing has changed significantly in the last five years. What are some of the important trends that you're seeing? Kelly: What we're seeing in the B2B space is really what we've seen in the B2C space for years, and that is, our clients are really trying to gain as much insight into their not only existing clients but potential clients as well? So you know additional firmographic information, credit information, anything that gives them a fuller picture of their clients, and then not only how to retain their existing clients and cross-sell, but also in terms of prospecting, how to best reach these targets once we've identified them what's the best channels to reach those prospects to get the best response. Gary: Kelly, most of our clients think of Experian Business Information Services as firstly business data and credit risk management. So how are we helping clients with their marketing initiatives? Kelly: With regard to B2B marketing, Experian has a tremendous amount of marketing assets including not only our U.S. Business Database which has over 16 million businesses. We also overlay that with our credit information, so clients can come and tap into this this huge resource to help them with their targeting in terms of selecting by firmographics, employee size, sales volume, as well as credit attributes, UCC filings, bankruptcies, information that can be translated to marketing campaigns. It can be utilized for direct marketing, for telemarketing, for digital applications – social media, email campaigns, analytical solutions, modeling. So it's a vast amount of resources that we can tap into to help with marketing campaigns. Gary: Can you share about some B2B marketing solutions we can look forward to from Experian? Kelly: Experian has a lot on the horizon with regard to B2B marketing. But one thing I'm particularly excited about is our new B2C linkage business to consumer linkage. Ultimately our clients have been coming to us saying you know, we're looking for a way to link our consumer records to any businesses that they may be associated with. So we create a customized linkage system that allows us to take in those consumer records, match them to our commercial repositories, and then provide back information that allows our clients to then not only target that consumer at their residential address but also their business address. So it gives them a chance to cross-sell and up-sell commercial offers as well as their consumer offers. Experian Business Marketing Solutions

Ten years ago movie night at our house would usually include a run to the video store where we would pick out a selection from the New Arrivals section, some candy, perhaps some popcorn and we would have our fingers crossed the selection was a good one. Nowadays it’s not uncommon to find us binge watching streamed episodes of “House of Cards” or “Mad Men on weekends.” What’s even more gratifying is after watching “House of Cards” unprompted, Netflix now recommends “The Newsroom” and other shows we invariably like. How do they know we would like these shows? This is predictive marketing at work, driven by big data. Netflix has developed sophisticated propensity models around each member’s viewing habits, and the net result is a better viewing experience with the service. We make amazing entertainment discoveries every week. In business marketing propensity models will determine which prospects or customers are likely to respond to a particular offer. For example, the marketing department of a large financial institution seeking to expand their commercial small business loan portfolio, might want to segment and target commercial lending offers to a concentration of customers most likely to accept a particular offer. When applied in business, propensity models can unlock opportunities for increased profit, share of wallet and deeper engagement with prospects and customers. At Experian, in a typical propensity modeling engagement we will first meet with our customers to understand their goals and objectives. We talk first about pre-screen criteria that enable us to screen out prospects that would not fit into the criteria. A sporting equipment manufacturer would probably not sell to companies in the mining or agriculture industries, so we weed out the ones least likely to lead to a successful conversion. Our data scientists and statisticians get to work on large data sets and evaluate a number of factors. Experian will then develop a customized response model that will identify significant characteristics of responders vs. non responders and therefore will maximally differentiate responders from non responders. Since (holding other factors constant) a higher response rate is preferred, a response model can help lower the cost per response. The response model will generate a “score” that can be used to rank order the prospects base in terms of response likelihood. The response model can be used in two different ways to achieve maximum effectiveness. It can be used to optimize the number of responders for a given sized solicitation, or it may be used to minimize the number of solicitations in order to achieve a budgeted number of responders. A high response score will indicate someone who is likely to respond, as is shown graphically in Exhibits 1 and 2. This work results in a model of the ideal target to which an offer would most likely resonate with. This is called a lookalike. The marketing department at our large financial institution might start off with a large list of potential candidates to send the offer via direct mail, 1 million for example. But mailing an offer to that many people may be cost prohibitive. A propensity model can identify prospects most likely to accept the offer, so your direct mail campaign is more targeted, thereby increasing ROI. A highly targeted mailing to your ideal targets is a safer bet, and would make for a much more predictable outcome. The marketer can feel more confident mailing an offer to lookalike prospects because the chances of successful conversion are that much higher. That’s the case for Woodland Hills based ForwardLine, who have been providing alternative short-term financing to small businesses since 2003. Working with Experian Decision Analytics, ForwardLine did an analysis of their direct marketing program and determined that 22 percent of direct mail was generating 68 percent of their underwriting approvals, exposing a significant gap in wasted marketing funds. The Experian Decision Analytics team developed a custom model which enabled ForwardLine to algorithmically target lookalike prospects with a higher propensity to convert into a successful loan engagement. Michael Carlson, V.P Marketing, ForwardLine ForwardLine Vice President of Marketing, Michael Carlson is thrilled with the initial results. “Working with Experian we were not only able to improve performance, but we are able to reduce our marketing spend, while achieving the same results. We have taken our direct marketing effort from a small program that was profitable, but not meaningful in terms of generating significant volume, to working with Experian to achieve remarkable results. It’s largely why we enjoyed 20 percent growth this year.” Best in Industry Credit Attributes Experian clients use our archived Biz AttributesSM along with collection specific data elements as independent variables for propensity model development. Experian’s Biz AttributesSM are a set of commercial bureau attribute definitions (includes several key demographic attributes as well) which are accurately developed off Experian’s Commercial BizSourceSM credit bureau. When used for response model development, Biz AttributesSM provides significant performance lift over other credit attributes. Biz AttributesSM are also effective in segmentation, as overlay to scores and policy rules definition, providing greater decisioning accuracy. Additionally, at Experian we are constantly monitoring our growing data warehouse looking for ways to develop new attributes. We live in an ever changing market place which requires us to develop new credit and demographic attributes as well as making enhancements to existing attributes. This process takes a disciplined, rigorous, and comprehensive approach based on experience guided by data intelligence. Our goal is to provide world-class service and the industry’s best practices for modeling attributes. To keep pace with market changes, new attributes are developed as new data elements become available, while raw data elements and existing attributes are monitored and managed following rigorous and comprehensive attribute governance protocols to ensure continued integrity of attributes. If you would like to learn more about propensity models, contact your Experian representative today.