Test Business Information Page

Highlights from the latest Beyond the Trends report Are you curious about the trends affecting the small business economy? The just released Summer 2023 Beyond the Trends report is packed with valuable insights based on data from over 25 million active businesses and the expert opinions from Experian’s V.P. of Commercial Data Science. This post covers some of the report's highlights, download your copy for the full scoop. A word from the report’s author: Energy Prices and Consumer Relief One of the most crucial takeaways from the report is that consumers and small businesses can expect continued relief in fuel prices in the coming months. This relief is due to the increased production of fuel in the United States and other countries. This production, coupled with other global and domestic factors, will provide more affordability in fuel costs for consumers and small businesses. This will help them manage their expenses better and, in turn, help producer costs decline, leading to more positive economic developments. Small Business Delinquency Small businesses, especially those that were propped up by stimulus money, are beginning to feel the pinch of inflation that is eating into their margins. Due to this, their savings are running lean, and many businesses are experiencing a rise in delinquencies. Delinquency rates have now exceeded pre-pandemic levels. Still, the report suggests that this is where they would expect delinquencies to be as the economy begins to grow gradually. Optimism Amidst Challenges Despite the lingering challenges and uncertainties brought about by the pandemic, small business owners remain optimistic. The report shows that the overall sentiment among small business owners is still positive, and they continue to seek out opportunities and innovations that could lead to growth and success. This is a positive development, and it's critical for businesses to continue to be agile and open to new opportunities and ideas. In closing: Small businesses are facing challenges such as filling job openings, higher costs, delinquencies and rising debt, but they remain optimistic and focused on opportunities for growth. By staying true to their values and fundamentals, businesses can thrive even in uncertain times. Grab your copy of the Summer 2023 Beyond the Trends report for more interesting insights on small businesses and their challenges. Download Beyond The Trends Summer 2023 Report

The post-pandemic economic landscape is experiencing an alarming rise in fraudulent activity affecting both businesses and consumers. With 75% of creditors experiencing heightened fraud losses and a 50% increase in fraud reports as per the FTC, the situation grows increasingly challenging. The expansion of e-commerce and the increasing sophistication of the dark web as a marketplace for stolen data exacerbate cybercrime threats. Moreover, lenders struggle to differentiate vast numbers of newly-formed businesses from bad actors due to limited data history available for decisioning. Amidst this, while Artificial Intelligence offers substantial promise in combatting fraud, it also significantly expands fraudsters’ toolboxes and poses significant fraud risks to creditors and consumers. To address these pressing concerns, businesses must step up their fraud risk management game by proactively adopting new fraud detection data and capabilities, and by integrating commercial entity and consumer data into their fraud decisioning strategies. What I am watching: The latest inflation report and jobs report showed positive news for the economy. Unemployment remains low and job creation is slowing but still strong. Inflation was down to 3% in June, the lowest in over two years, and closing in on the Fed’s target of 2%. Despite earlier indications of more interest rate hikes this year, this encouraging news may lead the Fed to leave interest rates alone at their upcoming July meeting. Subscribe Today Download the latest version of the Commercial Pulse Report here. Better yet, subscribe so you'll get it in your inbox every time it releases, or once a month as you choose.

Job satisfaction, or the lack thereof, is causing a shift in the workforce. Over half of employees in the United States are “quiet quitting” and actively looking for other jobs. In part, this is driving the number of self-employed individuals to rise. Growth in the self-employment rate for females is outpacing that of males. Female business owners account for double the number of new businesses open less than two-years when compared with males. Female business owners are seeking credit but across most industries receive less funding. Male and Female business owners have comparable credit risk profiles and utilize a similar mix of commercial credit products, yet male business owners, on average, receive higher credit funding amounts. Even in most industries where new credit originations skew to one gender, male business owners are granted higher credit funding amounts. This disparity in commercial credit lending has an adverse affect on female business owners and forces them to pursue other financing options. What I am watching: As an impending recession approaches, the labor market is expected to constrict which will reduce options for employees. Job vacancies are likely to be limited, quits will decline and self employment will slow as individuals seek the security of more traditional jobs. While people may not take the leap to start their own business as much, it will be interesting to see if the vast number of new businesses created over the past couple of years can survive an economic downturn. Subscribe Now Download the latest version of the Commercial Pulse Report here. Better yet, subscribe so you'll get it in your inbox every time it releases, or once a month as you choose.

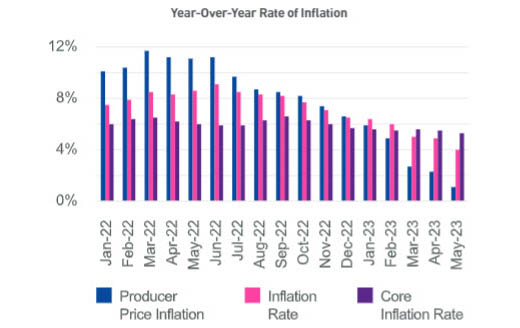

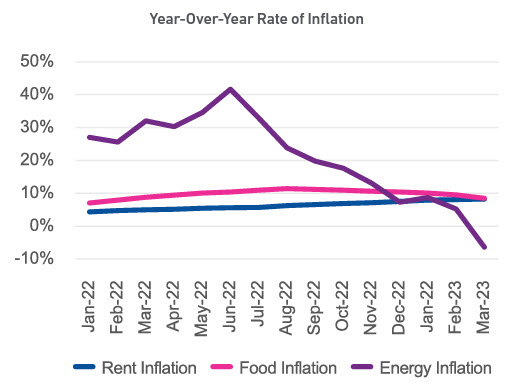

The annual inflation rate continued to decline with May coming in at 4% which was the eleventh consecutive monthly decrease and the lowest level since March 2021. Lower inflation is driven primarily by lower energy costs which decreased 11.7% year over year. Core inflation, which excludes volatile energy and food, slowed to 5.3%. Despite inflation still much higher than the Fed’s 2% target, the Fed paused interest rate hikes after 10 consecutive rate increases in the last 15 months. The Fed indicated that additional hikes may come later this year. New businesses continue to open at a high rate. Despite that these newer, and specifically smaller, businesses are making up a larger and larger portion of commercial credit, they have additional funding needs. According to the Federal Reserve’s 2023 Small Business Credit Survey, almost 70% of businesses with zero employees use personal funding sources for their business while only 27% of them obtain funding from financial institutions or lenders. Since the non-employer businesses reported on 36% had a decline in revenue in 2022 (vs. 38% of employer businesses’ revenue declined in 2022), there is a huge opportunity for financial institutions to tap into this market and support small business growth. What I am watching Small businesses with very few or no employees flourished coming out of the pandemic. It will be interesting to see how many of these micro-businesses will survive the headwinds of inflation, higher interest rates and less access to credit. With an economic slowdown on the horizon, the Fed actions in the coming months will be critical to the outcome. It is yet to be determined if the U.S. economy will achieve the hoped-for soft landing rather than a recession. Download your copy of Experian's Commercial Pulse Report today. Better yet, subscribe so you'll always know when the latest Pulse Report comes out. Subscribe Today

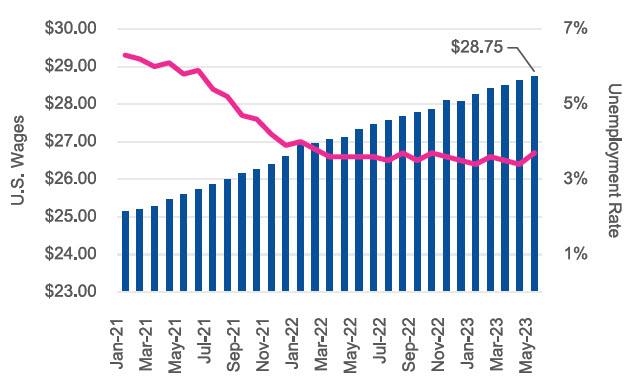

As of Q1 2023, Metropolitan-Core contained 78.1% of businesses, up from 76.3% in Q1 2018. The growth came despite high vacancy rates in offices due to the rise in telecommuting. Remote working has been around for a long time, but became vastly more prevalent during the COVID-19 pandemic when people were required to stay home but employers wanted to continue business operations. As the height of the pandemic gets farther in the rearview mirror, more employers are requiring employees to come back to the office. However, more workers are still working remotely, at least part of the time, than before the pandemic. With fewer people going into offices, there is a shift of population clustering in metro-centers where office buildings are located to areas outside of the metropolitan-core in more suburban and rural areas. With more people spending more time closer to their homes, they patronize businesses near their homes, driving the post-pandemic growth rate of businesses opening to be much greater outside of the metropolitan-core areas. The labor market continues to be robust. 339K jobs were created in May, the most in four months, and way above market forecasts of 190K. On the flip side, unemployment ticked up in May 3.7% from 3.4% in April, and is now the highest level since October 2022. What I am watching: The high rate of post-pandemic new business openings is fueled by small businesses with fewer than 20 employees. Some of the businesses are even home-based side jobs by individuals working remotely for their primary job. It will be interesting to see how many of these small businesses can survive through the expected upcoming economic slowdown or recession. With higher interest rates and commercial lenders tightening criteria, businesses that are struggling will have a tough time securing financing to weather any upcoming storms. Now that the Federal government raised the debt-ceiling and averted a government default, all eyes will turn back to the Federal Reserve’s battle to fight inflation. They indicated a pause in interest rate increases starting with their June 14th meeting. However, with the labor market still robust, the Fed’s decision may be a swayed by the May inflation report that is scheduled for release on June 13th. Download your copy of Experian's Commercial Pulse Report today. Better yet, subscribe so you'll always know when the latest Pulse Report comes out. Subscribe Today

Women led businesses lag behind on venture capital funding, and are turning to commercial loans and lines to bridge the gap Start-ups founded or cofounded by women receive only 44% of financial backing, but generate more revenue. While it is very encouraging to see the progress of women in business advancing, the pace of progress is slow and more could be done to achieve parity. Women’s salaries are slowly catching up, but they are still only about 80% of men’s wages. There are continued barriers to mothers participating in the labor force due to the limited capacity of childcare facilities, the high costs to families for childcare, and the low wages for childcare workers making lower skilled work sometimes more attractive in a tight labor market. These forces disproportionately affect women whether they work for wages or work for themselves as a small business owner. In addition to the issues facing women as workers, there are unique challenges they face as start-up founders as well. There is a known disparity in the funding provided to start-up businesses pitched by a woman versus a man and that is leaving women without the full funding they need to launch new businesses successfully. Added diversity within venture capital and angel investor groups could help change this dynamic so women can access that capital and expertise when launching their businesses at the same rate as their male counterparts. Without this, they are left to rely on self-funding and loans from banks — if they can get approved. The good news is that many women are making it work and the number of successful women-owned businesses continues to climb. What I am watching: The debt-ceiling standoff continues to cause uncertainty in the financial system with no compromise in place and a looming June 1 deadline, according to Secretary Janet Yellen. This situation is going to dwarf all others until there is a resolution, so all eyes are going to be on Congress and the President. Other signs in the economy suggest that inflation may finally be responding to the aggressive interest rate hikes enacted by the Fed. The Fed will have a more difficult decision on whether to raise interest rates one more time in June or hold them steady and wait to see if inflation continues to improve. Subscribe Today Download your copy of Experian's Commercial Pulse Report today. Better yet, subscribe so you'll always know when the latest Pulse Report comes out.

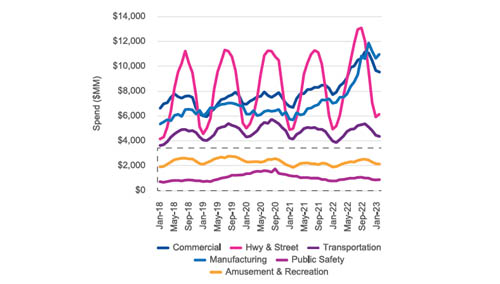

In its continued efforts to tame inflation, the Federal Reserve increased interest rates ¼ point last week, the tenth consecutive increase in just over a year. The cumulative increase is 500bps since March 2022, bringing the Fed Funds rate to 5.00%-5.25%, which is the highest since 2007. While inflation is still above the Fed’s target rate of 2%, they indicated a pause in rate increases. The labor market continues to be strong with April unemployment down to 3.4%, matching the low of January which is the lowest unemployment since 1969. Despite all the efforts by the Fed to have a soft landing, the economy could be upended if Congress does not increase the debt ceiling soon. With inflation slowing, and the labor market strong, a soft landing is possible. Treasury Secretary Yellen said the U.S. could default on debt as early as June 1st. If the U.S. defaults on outstanding debt, many forecast disastrous impacts to the world economy. Despite the recent decline in residential construction spending, construction spend remains strong in both residential and non-residential sectors. The construction industry is one of the few industries that saw a boom throughout the pandemic. Even though over the past few months both residential and non-residential experienced a decline in construction starts and construction spend, the volumes remain above pre-pandemic levels. High construction demand is being met with the formation of many new construction companies. New construction companies are seeking credit at a higher rate, but delinquencies in the construction industry are increasing. Higher risk and higher interest rates are causing commercial lending to tighten, and construction companies are seeing fewer loan originations and smaller loans/lines of credit. What I am watching: The non-residential construction industry is expected to see steady growth in 2023 due to project backlogs but could slow in 2024. Due to higher mortgage rates, the residential construction industry is expected to see a significant decline in housing starts through 2023 with the sector stabilizing in 2024. Aside from the immediate key drivers of interest rates and cost of capital, other areas of focus will be on the labor force and the demand for skilled vs. non-skilled labor. The number of skilled workers is decreasing yet the demand for skilled labor is increasing. The construction industry will have to attract the necessary talent to support the growth. Operational changes in the construction industry will be a driving factor. The construction industry is seeing a shift toward technology in all aspects of construction. Utilization of robotics is increasing which could replace portions of the workforce. Smart Cities, Smart Homes, Green Building are all trending which will materially change construction projects. The Construction Industry is experiencing a noticeable shift and companies will continue to adapt to keep up with demand.

Gain insight on small business credit conditions by attending our quarterly webinar.

Improve profiability through decision automation. This Experian article goes in depth on automating credit decisions for better efficiency.

The Commercial Pulse Report provides a bi-weekly directional update on small business credit. It delivers a quick read on macroeconomic conditions, high-level credit trends, score and attribute impacts, and other market-related activities.

Explore how Experian’s Ascend Commercial Suite helps risk managers navigate portfolio risk in an uncertain economy with data insights and strategic tools.

Recent news of the SVB collapse highlights the vulnerability of small banks and their crucial role in serving local communities. Small and medium-sized financial institutions should prepare for additional interest rate hikes.

The aggressive interest rate hikes instituted by the Federal Reserve over the past year and a half may have achieved the desired goal. Easing inflation (3.2% in October) and strong GDP growth (4.9% in Q3) are some of the first indications that the economy may experience the “soft landing” hoped for instead of a recession. The consistently strong labor market produced low unemployment and increasing wages, enabling personal spending to increase. However, while spending continues to grow, the growth rate is on a downward trend. The high rate of spending has been driven by consumers digging into savings and borrowing more. As savings dwindle and the cost to borrow increases, it is likely that consumers will retreat and the pull-back will likely hit discretionary categories first. What I am watching: Heading into the holiday season, consumer spending is still strong but how long will it last? The National Retail Federation is projecting that November and December retail sales will grow 3-4% which is in line with the 3.6% average increase from 2010-2019 but lower than the past three years. People are already dipping into savings and borrowing more to continue their consumption but that well will run dry at some point. In addition, 36% of consumers cite December is a month for seasonal financial distress, according to PYMNTS. While consumers may continue spending through the holiday season, the tide may turn in early 2024 when bills hit with higher interest rates. Download Full Report Download the latest version of the Commercial Pulse Report here. Better yet, subscribe so you'll get it in your inbox every time it releases, or once a month as you choose.

If you want to get the most out of your marketing campaigns, it's important that they are tailored for a specific audience. We invited Tony Romero on Business Chat to talk about part two of his three-part Sip and Solve webinar series focused on B2B marketing where he explains how segmentation and targeting can make all aspects (landing page or email) more effective by using industry SIC as well as NAICS codes. Look-a-like analysis CMO's challenged with restricted budgets Analyzing portfolio diversity and targeting minority-led, women-led businesses Profiling prospects with limited data attributes Watch Our Interview What follows is a lightly edited transcription of our talk. [Gary Stockton]: So in our last chat, we talked about maintaining robust marketing data to power effective campaigns and how clean data really helps businesses conduct effective marketing campaigns. This week, we switch gears to discuss the power of segmentation and targeting using industry SIC and NAICS codes to optimize your marketing budgets. So let's dive in. In our previous chat, we spoke about the changes that tech companies have enacted to make the job of targeting business prospects harder, but it's not game over for marketers. [Tony Romero]: No, definitely not. You know, it's really important to know that there's still a lot of a wealth of data out there that can be used to identify and segment target customers. You know, the first-party data obviously is really key, as well as being able to take information that may be spotty. If, for example, you only have a name or address, you can be able to through services like ours, be able to get a full, comprehensive set of data on that customer, both firmographic, demographic, and credit information, and then be able to use that to promote to customers. [Gary Stockton]: So can you share some examples of how Experian data can help marketers hone in on their target customer, for example, how SICs and NAICS codes can help? [Tony Romero]: Yeah, Gary, you're right. SIC and NAICS codes provide information about what industry the business is in. And so, by knowing that, you're able to target those consumers. So again, as I mentioned before, you can take a look at your existing customer base and find out who's your ideal target customer. And from that, then you can compare that to prospective businesses that look just like that. And that's what's called a lookalike analysis. And by using SIC and NAICS codes, you're able to use that to segment the market and then be able to promote effectively. And Gary, you also mentioned that with the economic state, CMOs have to watch their budgets and be as efficient as possible these days. So again, by doing very good segmenting of your target audience, you are making sure that your finance and financial output to a campaign are as efficient as possible. [Gary Stockton]: Excellent, regulators, they're focusing on diversity, equity, and inclusion. How can Experian help clients in that effort? [Tony Romero]: You know? Yeah. That's a very key point and definitely more than ever. It's important to focus on identifying your existing portfolio and seeing how many customers in your portfolio are minority-led or women-led businesses. So you can do benchmarking, you can see how you fare against other businesses in your market space. And that helps you to determine how much more do you need to market to these minority or women-led businesses. So what's number one is the benchmarking, but secondly, you need to be able to go out and look at your prospective target list and find out who are minority-led or women-led. And there, getting an indicator about a Woman-led or Minority-led business allows you to promote specifically to those types of businesses to help increase your portfolio. [Gary Stockton]: That's good. So if all I have is a name and an email address, and in a lot of cases, you know, if we're driving a newsletter, can I still profile this contact? Or are there other ways to do that with minimal info? [Tony Romero]: Yes, there is. You know, even just having a name and address is enough data to go through our type of service and be able to append all of the other information that we talked about, whether it's firmographic with SIC or NAICS codes, it could be demographic information where we look at the business and find out who the consumers that are tied to that business are? So that's called a B2C linkage. And from that now, you know who the actual individual is and go target those specific individuals. So that's also another key point to bring out [Gary Stockton]: Excellent stuff, Tony. Well, folks, if you enjoyed this chat and want to go a level deeper, don't miss Tony's campaign targeting Sip and Solve webinar – Fine Tuning B2b Campaign Targeting. He goes into greater detail on targeting B2B prospects, just click the image to be taken over to the recording.

We’re talking B2B marketing data hygiene with Tony Romero from our product team today on Business Chat.

Experian can be your trusted provider to supercharge B2B marketing campaigns with powerful data, analytics and consulting services.

As data privacy regulations become more strict and tech firms implement change, we share how marketers can remain effective while remaining compliant.

Experian Business Information Services recently introduced a powerful new marketing platform called Business TargetIQ. Product Manager, Kelly DeBoer answered a few questions about the product and described use cases that promote greater collaboration between credit and marketing departments. What does Business TargetIQ do? Business TargetIQ is our new marketing platform so it's a B2B marketing platform where clients can access data for marketing applications. How is it different from other business marketing platforms? It is unique in that it not only includes your standard or core firmagraphic information but also includes Experian's credit attributes. Does it have credit data? What does that mean to marketing or collaboration? Typically marketing data and credit data are housed in separate silos of information. With this tool the information will be combined together which will allow the tool not only to be used in traditional marketing applications for targeting but can also be in that risk factor which applies to different divisions within our client's applications or use cases of the data. Who would most benefit from Business TargetIQ? The thing about Business TargetIQ is it truly applies to all different verticals, as well as all different contacts within the company. So whether it's a financial vertical or a trade vertical, retail, just across the board all clients can utilize this. Anybody that's doing marketing can utilize this platform. What core problems does Business TargetIQ solve? It solves a lot of different problems, so, the most common client issues that are brought to our attention are gaps in data, as well as in the marketing initiatives. So they may have data in-house but they have holes within the data. Our tool will allow them to not only upload their client records and fill in a lot of those gaps that they may have, whether it be contact information, or firmagraphics or address information. It will standardize that data and fill in those gaps. But will also provide the means to again use that data. Our business database which has over 16 million records. They can then utilize that information for prospecting, for data append, for analytics, for research applications, so it solves a lot of problems with regard to marketing and data concerns. How does credit data help with prospecting? So what we find is clients come to us and they may say you know I have an idea of what our clients look like, they're in this SIC or in this industry code, or they have this sales volume or employee size, but what they may not know is on the back end which really helps identify and target those businesses is the credit attributes, so the risk factors around those. So do they have delinquencies in their payments? Have they filed bankruptcies? Do they have UCC filings? So it allows them to take it that next step and not only really define what their clients look like, but identify clients that look like that. Learn More About Business TargetIQ

So you’ve created the perfect campaign with great creatives and an unbeatable offer. You deploy the campaign and sit on the edge of your seat waiting for all the leads to flood in. After a couple of days, you notice a couple of responses but nowhere near the volume of what you were hoping for, and you’re stuck asking yourself “why?” Here are a couple of hypotheses: 1.) the people you reached out to aren’t the right audience so they don’t care about your offer, or 2.) your target audience didn’t see your efforts because you used the wrong channel. The process of finding new business customers can be expensive and sometimes unpredictable, but it doesn’t have to be. Here are 3 tips to help improve your prospecting efforts: Tip #1: Define your ideal customer One of the most fundamental ways you can help grow your current customer base is to have a clear understanding of what they actually look like (or defining what they should look like). What’s their job title? What are their biggest business challenges? Are they web savvy? How do they prefer to get industry news? Addressing discovery questions like these allows you to better understand who you’re talking to and how to talk to them. Additionally, you’ll be able to use this profile to help you mimic your best customers and target look-a-likes. Tip #2: Target new businesses Get your products/services in front of new businesses before your competitors. Not surprisingly, many marketers overlook targeting new businesses because of the lack of data — how do you know a new company is in business? How do you know if they’re the right business for you to even target? Fortunately, there are many services in today's market that can help fill in the gaps. Using something like Experian’s US Business Database, which is a database of more than 16 million active U.S. companies, can help you discover new businesses sooner and beat out your competitors to reach them first. Tip #3: Find the decision-makers Identifying the right businesses to target is important, but ensuring that your offer gets in front of the right person – the decision maker – is even better. By finding the decision maker and directing your marketing efforts towards them, you can rest assure that your message lands in the hands of the person that matters most. Want to take it one step further? Once you know who you’re talking to, you can tailor the message and offer to be more relevant for that specific audience, which ultimately helps increase your chances of getting a response. Finding and reaching new business customers can be a daunting and expensive tasks, especially if you don’t target your prospecting efforts. Be sure to keep these tips in mind when approaching your marketing strategy and don’t let today’s data challenges hold you back. Learn more about Experian's US Business Database or our other marketing capabilities.

I had the pleasure of speaking with Kelly DeBoer recently. She is a Product Manager at Experian working in Business Information Services. Kelly leads product strategy for our business marketing products. In this Business Q&A we talk about B2B marketing trends and how Experian is helping business clients get the most out of their marketing initiatives. Gary: B2B marketing has changed significantly in the last five years. What are some of the important trends that you're seeing? Kelly: What we're seeing in the B2B space is really what we've seen in the B2C space for years, and that is, our clients are really trying to gain as much insight into their not only existing clients but potential clients as well? So you know additional firmographic information, credit information, anything that gives them a fuller picture of their clients, and then not only how to retain their existing clients and cross-sell, but also in terms of prospecting, how to best reach these targets once we've identified them what's the best channels to reach those prospects to get the best response. Gary: Kelly, most of our clients think of Experian Business Information Services as firstly business data and credit risk management. So how are we helping clients with their marketing initiatives? Kelly: With regard to B2B marketing, Experian has a tremendous amount of marketing assets including not only our U.S. Business Database which has over 16 million businesses. We also overlay that with our credit information, so clients can come and tap into this this huge resource to help them with their targeting in terms of selecting by firmographics, employee size, sales volume, as well as credit attributes, UCC filings, bankruptcies, information that can be translated to marketing campaigns. It can be utilized for direct marketing, for telemarketing, for digital applications – social media, email campaigns, analytical solutions, modeling. So it's a vast amount of resources that we can tap into to help with marketing campaigns. Gary: Can you share about some B2B marketing solutions we can look forward to from Experian? Kelly: Experian has a lot on the horizon with regard to B2B marketing. But one thing I'm particularly excited about is our new B2C linkage business to consumer linkage. Ultimately our clients have been coming to us saying you know, we're looking for a way to link our consumer records to any businesses that they may be associated with. So we create a customized linkage system that allows us to take in those consumer records, match them to our commercial repositories, and then provide back information that allows our clients to then not only target that consumer at their residential address but also their business address. So it gives them a chance to cross-sell and up-sell commercial offers as well as their consumer offers. Experian Business Marketing Solutions

Ten years ago movie night at our house would usually include a run to the video store where we would pick out a selection from the New Arrivals section, some candy, perhaps some popcorn and we would have our fingers crossed the selection was a good one. Nowadays it’s not uncommon to find us binge watching streamed episodes of “House of Cards” or “Mad Men on weekends.” What’s even more gratifying is after watching “House of Cards” unprompted, Netflix now recommends “The Newsroom” and other shows we invariably like. How do they know we would like these shows? This is predictive marketing at work, driven by big data. Netflix has developed sophisticated propensity models around each member’s viewing habits, and the net result is a better viewing experience with the service. We make amazing entertainment discoveries every week. In business marketing propensity models will determine which prospects or customers are likely to respond to a particular offer. For example, the marketing department of a large financial institution seeking to expand their commercial small business loan portfolio, might want to segment and target commercial lending offers to a concentration of customers most likely to accept a particular offer. When applied in business, propensity models can unlock opportunities for increased profit, share of wallet and deeper engagement with prospects and customers. At Experian, in a typical propensity modeling engagement we will first meet with our customers to understand their goals and objectives. We talk first about pre-screen criteria that enable us to screen out prospects that would not fit into the criteria. A sporting equipment manufacturer would probably not sell to companies in the mining or agriculture industries, so we weed out the ones least likely to lead to a successful conversion. Our data scientists and statisticians get to work on large data sets and evaluate a number of factors. Experian will then develop a customized response model that will identify significant characteristics of responders vs. non responders and therefore will maximally differentiate responders from non responders. Since (holding other factors constant) a higher response rate is preferred, a response model can help lower the cost per response. The response model will generate a “score” that can be used to rank order the prospects base in terms of response likelihood. The response model can be used in two different ways to achieve maximum effectiveness. It can be used to optimize the number of responders for a given sized solicitation, or it may be used to minimize the number of solicitations in order to achieve a budgeted number of responders. A high response score will indicate someone who is likely to respond, as is shown graphically in Exhibits 1 and 2. This work results in a model of the ideal target to which an offer would most likely resonate with. This is called a lookalike. The marketing department at our large financial institution might start off with a large list of potential candidates to send the offer via direct mail, 1 million for example. But mailing an offer to that many people may be cost prohibitive. A propensity model can identify prospects most likely to accept the offer, so your direct mail campaign is more targeted, thereby increasing ROI. A highly targeted mailing to your ideal targets is a safer bet, and would make for a much more predictable outcome. The marketer can feel more confident mailing an offer to lookalike prospects because the chances of successful conversion are that much higher. That’s the case for Woodland Hills based ForwardLine, who have been providing alternative short-term financing to small businesses since 2003. Working with Experian Decision Analytics, ForwardLine did an analysis of their direct marketing program and determined that 22 percent of direct mail was generating 68 percent of their underwriting approvals, exposing a significant gap in wasted marketing funds. The Experian Decision Analytics team developed a custom model which enabled ForwardLine to algorithmically target lookalike prospects with a higher propensity to convert into a successful loan engagement. Michael Carlson, V.P Marketing, ForwardLine ForwardLine Vice President of Marketing, Michael Carlson is thrilled with the initial results. “Working with Experian we were not only able to improve performance, but we are able to reduce our marketing spend, while achieving the same results. We have taken our direct marketing effort from a small program that was profitable, but not meaningful in terms of generating significant volume, to working with Experian to achieve remarkable results. It’s largely why we enjoyed 20 percent growth this year.” Best in Industry Credit Attributes Experian clients use our archived Biz AttributesSM along with collection specific data elements as independent variables for propensity model development. Experian’s Biz AttributesSM are a set of commercial bureau attribute definitions (includes several key demographic attributes as well) which are accurately developed off Experian’s Commercial BizSourceSM credit bureau. When used for response model development, Biz AttributesSM provides significant performance lift over other credit attributes. Biz AttributesSM are also effective in segmentation, as overlay to scores and policy rules definition, providing greater decisioning accuracy. Additionally, at Experian we are constantly monitoring our growing data warehouse looking for ways to develop new attributes. We live in an ever changing market place which requires us to develop new credit and demographic attributes as well as making enhancements to existing attributes. This process takes a disciplined, rigorous, and comprehensive approach based on experience guided by data intelligence. Our goal is to provide world-class service and the industry’s best practices for modeling attributes. To keep pace with market changes, new attributes are developed as new data elements become available, while raw data elements and existing attributes are monitored and managed following rigorous and comprehensive attribute governance protocols to ensure continued integrity of attributes. If you would like to learn more about propensity models, contact your Experian representative today.