Apply DA Tag

A robust segmentation analysis contains two components: first is generation of potential segments, and the second is generation of potential segments.

On May 11, 2018, financial institutions will be required to perform Customer Due Diligence routines for their legal entity customers. Here are 3 facts that you should know

In 2017, we saw an increase of more than 30 percent in e-commerce fraud attacks compared with 2016.

With a maximized approach to collections, you can see an uplift in performance of 5% to 30% in Key Performance Indicators against traditional techniques.

Implement identity management and account management procedures that are effective and don't affect user experience

Recognizing customers is more than good service. Identify your customers to spot fraud. It’s a simple concept, but it’s not so simple to do. Consumers expect to be recognized and welcomed wherever and whenever they do business. Here's more insights on recognition and fraud.

From malware and phishing to expansive distributed denial-of-service attacks, the sophistication, scale and impact of cyberattacks have evolved significantly in recent years. Mitigate risk by employing these best practices:

Mitigate synthetic ID fraud before they enter your portfolio with these steps.

Trended attributes and consumer lending Digging deeper into consumer credit data can help provide new insights into trending behavior, providing more than just point-in-time credit evaluation. The information derived through trended attributes can help you understand your customers’: Payment rates and account migration behavior. Slope of balance changes. Delinquency patterns over time. Today’s consumer lending environment is more dynamic and competitive than ever. Trended attributes can give additional lift in your segmentation strategies and custom models and provides a high-definition lens that opens a world of opportunity. Learn more

Federal agencies are most directly impacted by new NIST standards but is a shift in identity proofing for consumers, businesses and public sector agencies.

Current debt collection process is outdated. The process is driven by the measurement of delinquency and loss and doesn't consider the customer.

Kathleen Peters, SVP of Product Management for Global Fraud and Identity, and recently included in the Top 100 influencers in Identity.

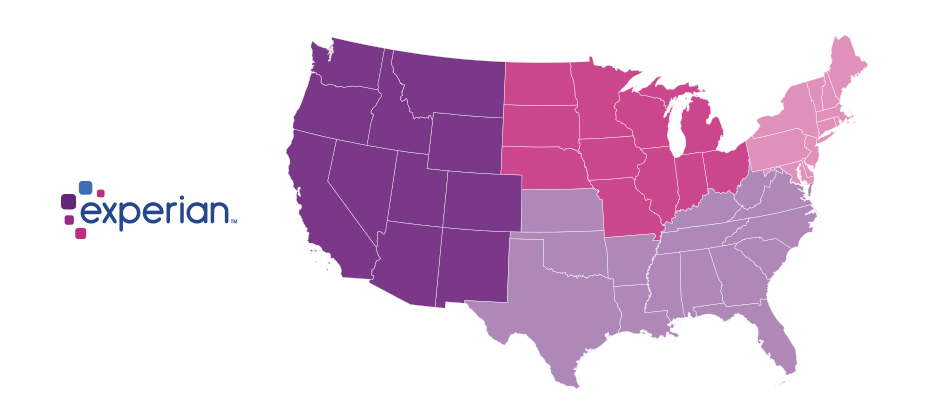

The average number of retail trades per consumer has been trending down since 2007. But the average consumer retail debt is trending up, roughly $73 year-over-year. When analyzing single-store credit card debt by state in 2017, we found these states had the highest retail debt

Experian introduces new trended attributes to help lenders better serve consumers across the credit life cycle

Credit card balances grew to $786.6 billion at the end of 2017, a 6.7% increase to the previous year and the largest outstanding balance in over a decade. And while the delinquency rate increased slightly to 2.26%, it is significantly lower than the 4.73% delinquency rate in 2008 when outstanding balances were $737 billion.