All posts by Traci Krepper

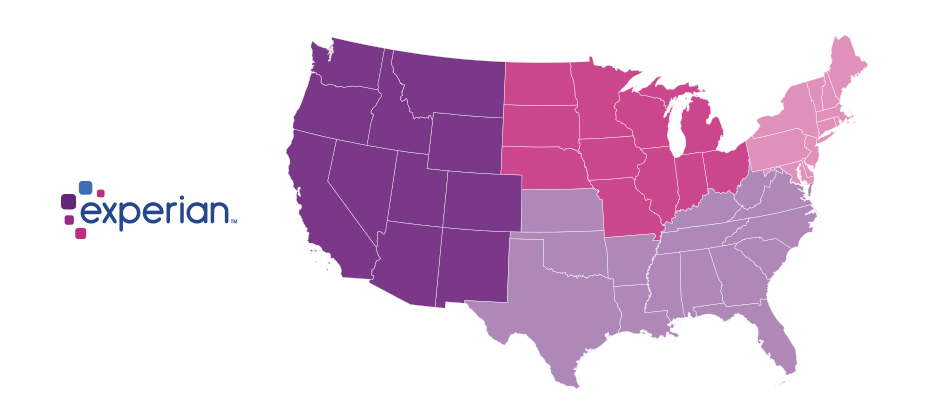

With 16.7 million reported victims of identity fraud in 2017 (that’s 6.64 percent of the U.S. population), it was another record year for the number of fraud victims. And as online and mobile transaction growth continued to significantly outpace brick-and-mortar growth, criminal attacks also grew rapidly. This past year, we saw an increase of more than 30 percent in e-commerce fraud attacks compared with 2016. As we’ve done over the past three years, Experian® analyzed millions of online transactions to identify fraud attack rates for both shipping and billing locations across the United States. We looked at several data points, including geography and IP address, to help businesses better understand how and where fraud is being perpetrated so they can better protect against it. The 2017 e-commerce fraud attack rate analysis shows: Delaware and Oregon continue to be the riskiest states for both billing and shipping fraud. Delaware; Oregon; Washington, D.C.; Florida; and Georgia are the top five riskiest states for billing fraud. Delaware, Oregon, Florida, New York and California are the top five riskiest states for shipping fraud, accounting for 50 percent of total fraud attacks. South El Monte, Calif., is the riskiest city overall, with an increase in shipping fraud of approximately 230 percent. Shipping fraud most often occurs near major airports and seaports due to reshippers and freight forwarders that receive domestic goods and often send them overseas. When a transaction originates from an international IP address, shipping fraud is 6.7 times likelier than the average, while billing fraud becomes 7.1 times likelier. Where is e-commerce fraud happening? Typically, the highest-risk areas for fraud are in ZIP™ codes and cities near large ports of entry or airports. These are ideal locations to reship fraudulent merchandise, enabling criminals to move stolen goods more effectively. Top 10 riskiest billing ZIP™ codes Top 10 riskiest shipping ZIP™ codes 97252 Portland, OR 97079 Beaverton, OR 33198 Miami, FL 33122 Miami, FL 33166 Miami, FL 91733 South El Monte, CA 33122 Miami, FL 97251 Portland, OR 77060 Houston, TX 97250 Portland, OR 33195 Miami, FL 33166 Miami, FL 97250 Portland, OR 97252 Portland, OR 97251 Portland, OR 33198 Miami, FL 33191 Miami, FL 33195 Miami, FL 97253 Portland, OR 33192 Miami, FL Source: Experian.com Source: Experian.com What’s more, many of the riskiest ZIP™ codes and cities experience a high volume of transactions originating from international IP addresses. In fact, the top 10 riskiest ZIP codes overall tend to experience fraudulent activity from numerous countries overseas, including China, Venezuela, Taiwan and Hong Kong, and Argentina. These fraudsters tend to implement complex fraud schemes that can cost businesses millions of dollars in fraud losses. Additionally, the analysis shows that traffic coming from a proxy server — which could originate from domestic and international IP addresses — is 74 times riskier than the average transaction. The problem The increase in e-commerce fraud attacks shouldn’t come as a huge surprise. The uptick in data breaches, merchants’ continued adoption of EMV-enabled terminals to protect against counterfeit card fraud and the abundance of consumer data on the dark web means that information is even more accessible to criminals. This enables them to open fraudulent accounts, take over legitimate accounts and submit fraudulent transactions. Another reason for the increase is automation. In the past, criminals needed a strong understanding of fraud methods and technology, but they can now bring down an entire organization by simply downloading a file and automating the submission of thousands of applications or transactions simultaneously. Since fraudsters need to make these transactions appear as normal as possible, they often leverage the cardholder’s actual billing details with slight differences, such as e-mail address or shipping location. Unfortunately, the mass availability of compromised data and the abundance of fraudsters makes it increasingly challenging to identify and separate legitimate customers from attackers across the country. Because of the widespread prevalence of fraud and data compromises, we don’t see billing fraud concentrated in just one region of the country. In fact, the top five states for billing fraud make up only about 18 percent of overall fraud attacks. Top 5 riskiest billing fraud states Top 5 riskiest shipping fraud states State Fraud attack rate State Fraud attack rate Delaware 93.4 Delaware 195.9 Oregon 86.1 Oregon 170.1 Washington, D.C. 46.5 Florida 45.1 Florida 39.2 New York 37.3 Georgia 31.5 California 32.6 Source: Experian.com Source: Experian.com Prevention and protection need to be the priority As businesses get a better understanding of how and where fraud is perpetrated, they can implement proactive strategies to detect and prevent attacks, as well as protect payment information. While no one single strategy can address the entire scope of fraud, there are advanced data sets and technology — such as device intelligence, behavioral and physical biometrics, document verification and entity resolution — that can help businesses make better fraud decisions. Fortunately, consumers can also play a major role in safeguarding their information. In addition to regularly checking their credit reports and bank/credit card statements for fraudulent activity, consumers can limit the data they share on social networking sites, where attackers often begin when perpetrating identity fraud. While we continue to help both organizations and consumers limit their exposure to e-commerce fraud, we anticipate that criminals will attempt more sophisticated fraud schemes. But businesses can stay ahead of the curve. This comes down to having a keen understanding of how fraud is being perpetrated, as well as leveraging data, technology and multiple layered strategies to better recognize legitimate customers and make more precise fraud decisions. View our e-commerce fraud heat map and download the top 100 riskiest ZIP codes in the United States. Experian is a nonexclusive full-service provider licensee of the United States Postal Service®. The following trademark is owned by the United States Postal Service®: ZIP. The price for Experian’s services is not established, controlled or approved by the United States Postal Service.

I recently sat down with Kathleen Peters, SVP and Head of Fraud and Identity, to discuss the state of fraud and identity, the pace of change in the space and her recent inclusion in the Top 100 influencers in Identity by One World Identity. ----------- Traci: Congratulations on being included on the Top 100 influencers list. What a nice honor. Kathleen: Yes, thank you. It is a nice honor and inspiring to be included among some great innovators in the industry. The list includes entrepreneurs to leaders of large organizations like us. It’s a nice mix across all facets of identity. T: Tell me about your role. How long have you been at Experian? K: I lead the team that defines the product strategy for our global fraud and ID portfolio. I’ve been with Experian just over four years, joining soon after we acquired 41st Parameter®. T: What was your first job? K: My first job out of college was with Motorola in Chicago. I was an electrical engineer, working on advanced cellphone technology. T: They were not able to keep up with the market? K: The entire industry was caught by the introduction of the iPhone. All the major cellphone companies were impacted — Nokia, Ericsson, Siemens and others. Talk about disrupting an industry. T: Yeah. These are great examples of how the disrupters have taken out the initial companies. Certainly, Motorola, Nokia, those companies. Even RIM Blackberry, which redefined the digital or cellular space, has all but disappeared. K: Yes, exactly. It was interesting to watch RIM Blackberry when they disrupted Motorola’s pager business. Motorola had a very robust pager line. Even then they had a two-way pager with a keyboard. They just missed the idea of mobile email completely. It’s really, really fascinating to look back now. T: Changing the subject a little, what motivates you to get out of bed in the morning? K: One of my favorite questions. I’m a very purpose-driven person. One of the things I really like about my role and one of the reasons I came to Experian in the first place is that I could see this huge potential within the company to combine offline and online identity information and transaction information to better recognize people and stop fraud. T: What do you see as the biggest threat to organizations today? K: I would have to say the pace of change. As we were just talking about, major industries can be disrupted seemingly overnight. We’re in the midst of a real digital transformation in how we live, how we work, how we share information and even how we share money. The threat to companies is twofold. One is the “friendly fire” threat, like the pace of change, disrupters to the market, new ways of doing things and keeping pace with that innovation. The second threat is that with digitization comes new types of security and fraud risks. Today, organizations need to be ever-vigilant about their security. T: How do you stay ahead of that pace of change? K: Well, my husband and I have lived in Silicon Valley since 1997. Technology and innovation are all around us. We read about it and we hear about it in the news. We engage with our neighbors and other people who we meet socially and within our networks. You can’t help but be immersed in it all the time. It certainly influences the way we go about our lives and how we think and act and engage as a family. We’re all technically curious. We have two kids, and our neighborhood high school, Homestead High, is the same high school Steve Jobs went to. It’s fun that way. T: Definitely. What are some of the most effective ways for businesses to combat the threat of fraud? K: I firmly believe that nowadays it all needs to start with identity. What we’ve found — and confirmed through research in our recent Global Fraud Report, plus conversations I’ve had with clients and analysts — is that if you can better recognize someone, you’ll go a long way to prevent fraud. And it does more than prevent fraud; it provides a better experience for the people you’re engaged with. Because once you recognize an individual, that initiates a trusted relationship between the two of you. Once people feel they’re in a trusted relationship, whether it’s a social relationship or a financial transaction, whatever the relationship is — once you feel trusted, you feel safe, you feel protected. And you’re more likely to want to engage again in the future. I believe the best thing organizations can do is take a multilayered approach to authenticating and identifying people upfront. There are so many ways to do this digitally without disrupting the consumer, and this is the best opportunity for businesses. If we collectively get that right, we’ll stop fraud. T: What are some of the things Experian is focusing on to help businesses stop fraud? K: We’ve focused on our CrossCore® platform. CrossCore is a common access and decisioning capability platform that allows the combining and layering of many different approaches — some active, some passive — to identify a customer in a transaction. You can incorporate things like biometrics and behavioral attributes. You can incorporate digital information about the device you’re engaging with. You can layer in online and offline identity information, like that from our Precise ID® product. CrossCore also enables you to layer in other digital attributes and alternative data such as email address, phone number and the validity of that phone number. CrossCore provides a great opportunity for us to showcase innovation, whether that comes from a third-party partner or even from our own Experian DataLabs. T: How significant do you see machine learning moving forward? K: Machine learning, it has all kinds of names, right? I think of machine learning, artificial intelligence, data robotics, parallel computing — all these things are related to what we used to call big data processing, but that’s not really the trendy term anymore. The point is that there is so much data today. There’s a wealth of data from all different sources, and as a society we’re producing it in exponential volumes. Having more and more and more data is not useful if you can’t derive insights from it. That’s why machine learning, augmented with human intervention or direction, is the best way forward, because there’s so much data out there available in the world now. No matter what problem we’re trying to solve, there’s a wealth of data we can amass, but we need to make sense of it. And the way to make sense of massive amounts of data in a reasonable amount of time is by using some sort of artificial intelligence, or machine learning. We’re going to see it in all kinds of applications. We already are today. So, while I think of machine learning as a generic term, I do think it’s going to be with us for a while to quickly compute and derive meaningful insights from the massive amounts of data all around us. T: Thanks, okay. Last question, and I hope a little fun. How would you describe yourself in one word? K: Curious. T: Ah, that’s a good choice. K: I am always curious. That’s why I love living where I live. It’s why I like working in technology. I’ve always wondered how things work, how we might improve on them, what’s under the hood. Why people make the decisions they do. How does someone come up with this? I’m always curious. T: Well, thank you for the time, and congrats again on being included in the Top 100 influencers in Identity.

Traditional credit attributes provide immense value for lenders when making decisions, but when used alone, they are limited to capturing credit behavior during a single moment of time. To add a deeper layer of insight, Experian® today unveiled new trended attributes, aimed at giving lenders a wider view into consumer credit behavior and patterns over time. Ultimately, this helps them expand into new risk segments and better tailor credit offers to meet consumer needs. An Experian analysis shows that custom models developed using Trended 3DTM attributes provide up to a 7 percent lift in predictive performance when compared with models developed using traditional attributes only. “While trended data has been shown to provide additional insight into a consumer’s credit behavior, lack of standardization across different providers has made it a challenge to gain those insights,” said Steve Platt, Experian’s Group President of Decision Analytics and Data Quality. “Trended 3D makes it easy for our clients to get value from trended data in a consistent manner, so they can make more informed decisions across the credit life cycle and, more importantly, give consumers better access to lending options.” Experian’s Trended 3D attributes help lenders unlock valuable insights hidden within credit reports. For example, two people may have similar balances, utilization and risk scores, but their paths to that point may be substantially different. The solution synthesizes a 24-month history of five key credit report fields — balance, credit limit or original loan amount, scheduled payment amount, actual payment amount and last payment date. Lenders can gain insight into: Changes in balances over time Migration patterns from one tradeline or multiple tradelines to another Variations in utilization and credit limits Changes in payment activity and collections Balance transfer and debt consolidation behavior Behavior patterns of revolving trades versus transactional trades Additionally, Trended 3D leverages machine learning techniques to evaluate behavioral data and recognize patterns that previously may have gone undetected. To learn more information about Experian’s Trended 3D attributes, click here.

Experian® is honored to be an MRC Technology Award nominee. But we can’t win the MRC People’s Choice Award without your help! The annual MRC Technology Awards recognize the most elite solution providers making significant contributions in the fraud, payments and risk industries. CrossCore® is the first smart, open, plug-and-play platform for fraud and identity services. We know, and our clients agree, that it delivers a better way to modify strategies quickly, catch fraud faster, improve compliance and enhance the customer experience. Need further convincing? Here are the top 3 reasons you should vote for CrossCore. Reason 1: common access Manage your entire fraud and identity portfolio. Start immediately by turning on Experian services through a single integration. Connect to services quickly with a common, flexible API. Reason 2: open approach Control the data being used in decisions. CrossCore supports a best-in-class approach to managing a portfolio of services that work together in any combination — including Experian solutions, third-party services and client systems — delivering the level of confidence needed for each transaction. Reason 3: workflow decisioning Act quickly and adapt to new risks with built-in strategy design and workflow capabilities. You can precisely tailor strategies based on transaction type or risk threshold. Make changes dynamically, with no downtime. We hope you’ll vote for CrossCore as a better way to manage fraud prevention and identity services.

Subprime vehicle loans When discussing automotive lending, it seems like one term is on everyone’s lips: “subprime auto loan bubble.” But what is the data telling us? Subprime auto lending reached a 10-year record low for Q1. The 30-day delinquency rate dropped 0.5% from Q1 2016 to Q1 2017. Super-prime share of new vehicle loans increased from 27.4% in Q1 2016 to 29.12% in Q1 2017. The truth is, lenders are making rational decisions based on shifts in the market. When delinquencies started going up, the lending industry shifted to more creditworthy customers — average credit scores for both new and used vehicle loans are on the rise. Read more>

Knowing where e-commerce fraud takes place matters We recently hosted a Webinar with Mike Gross, Risk Strategy Director at Experian and Julie Conroy, Research Director at Aite Research Group, looking at the current state of card-not-present fraud, and what to prepare for in the coming year. Our biannual analysis of fraud attacks, served as a backdrop for the trends we’ve been seeing. I wanted to share some observations from the Webinar. Of course, if you prefer to hear it firsthand, you can download the archive recording here. I’ll start with the current landscape of card-not-present fraud. Julie shared 5 key trends her firm has identified regarding e-commerce fraud: Rising account take-over fraud Loyalty points targeted Increasingly global transactions Frustrating false declines Increasingly mobile consumers One particularly interesting note that Julie made was regarding consumer frustration levels towards forgotten passwords. While consumers are more frustrated when they’re locked out of access to their banking accounts (makes sense, it’s their money), forgotten passwords are more detrimental to e-commerce retailers since consumers are likely to go to another site. This equates to a frustrated consumer, and lost revenue for the business. Next, Mike went through the findings from our 2016 e-commerce fraud attack analysis. Fraud attack rates show the attempted fraudulent e-commerce transactions against the population of overall e-commerce orders. Overall, e-commerce attack rates spiked 33% in 2016. The biggest trends we saw included: Increased EMV adoption is driving a shift from counterfeit to card-not-present fraud 2B breached records disclosed in 2016, more than 3x any previous year Consumers reporting credit card fraud jumped from 15% in 2015 to over 32% in 2016 Attackers shifting locations slightly and international orders rely on freight forwarders 10 states saw an increase of over 100% in fraudulent orders Over 70 of the top 100 riskiest postal codes were not in last year’s list So, what will 2017 bring? Be prepared for more attacks, more global rings, more losses for businesses, and the emergence of IoT fraud. Businesses need to anticipate an increase of fraud over time and to be prepared. The value of employing a multi-layered approach to fraud prevention especially when it comes to authenticating consumers to validate transactions cannot be understated. By looking at all the points of the customer journey, businesses can better protect themselves from fraud, while maintaining a good consumer experience. Most importantly, having the right fraud solution in place can help businesses prevent losses both in dollars and reputation.

Turns out, Americans still don’t know much about CyberSecurity. That’s according to new research from the Pew Data Center, which conducted a cybersecurity knowledge quiz. The 13 question quiz was designed to test American’s knowledge on a number of cybersecurity issues and terms. A majority of online adults can identify a strong password and recognize the dangers of using public Wi-Fi. However, many struggle with more technical cybersecurity concepts, such as how to identify true two-factor authentication or determine if a webpage they are using is encrypted. As we in the industry know, cybersecurity is a complicated and diverse subject, but given the pervasiveness of news around cybersecurity, I was still a little surprised by the lack of knowledge. The typical (median) respondent answered only five of the 13 questions correctly (with a mean of 5.5 correct answers). 20% answered more than eight questions accurately, and just 1% received a “perfect score” by correctly answering all 13 questions. The study showed that public knowledge of cybersecurity is low on some relatively technical issues, like identifying the correct example of multi-factor authentication, understanding how VPNs minimize risk and knowing what a botnet is. On the flip side, the two questions that the majority of respondents answered correctly included identifying the strongest password from a list of four options and understanding that public Wi-Fi networks have risk even when they are password protected. Given the median scores, I was proud of missing only one question – guess I have more reading to do on Botnets. As an industry, it is our duty to not only create systems and securities to improve the tactical effectiveness of fraud prevention, but to educate consumers on many of these topics as well. They often are the first line of defense in stopping fraud and reducing the threat of breaches.

2017 data breach landscape Experian Data Breach Resolution releases its fourth annual Data Breach Industry Forecast report with five key predictions What will the 2017 data breach landscape look like? While many companies have data breach preparedness on their radar, it takes constant vigilance to stay ahead of emerging threats and increasingly sophisticated cybercriminals. To learn more about what risks may lie ahead, Experian Data Breach Resolution released its fourth annual Data Breach Industry Forecast white paper. The industry predictions in the report are rooted in Experian's history helping companies navigate more than 17,000 breaches over the last decade and almost 4,000 breaches in 2016 alone. The anticipated issues include nation-state cyberattacks possibly moving from espionage to full-scale cyber conflicts and new attacks targeting the healthcare industry. "Preparing for a data breach has become much more complex over the last few years," said Michael Bruemmer, vice president at Experian Data Breach Resolution. "Organizations must keep an eye on the many new and constantly evolving threats and address these threats in their incident response plans. Our report sheds a light on a few areas that could be troublesome in 2017 and beyond." "Experian's annual Data Breach Forecast has proven to be great insight for cyber and risk management professionals, particularly in the healthcare sector as the industry adopts emerging technology at a record pace, creating an ever wider cyber-attack surface, adds Ann Patterson, senior vice president, Medical Identity Fraud Alliance (MIFA). "The consequences of a medical data breach are wide-ranging, with devastating effects across the board - from the breached entity to consumers who may experience medical ID fraud to the healthcare industry as a whole. There is no silver bullet for cybersecurity, however, making good use of trends and analysis to keep evolving our cyber protections along with forecasted threats is vital." "The 72 hour notice requirement to EU authorities under the GDPR is going to put U.S.-based organizations in a difficult situation, said Dominic Paluzzi, co-chair of the Data Privacy & Cybersecurity Practice at McDonald Hopkins. "The upcoming EU law may just have the effect of expediting breach notification globally, although 72 hour notice from discovery will be extremely difficult to comply with in many breaches. Organizations' incident response plans should certainly be updated to account for these new laws set to go in effect in 2017." Omer Tene, Vice President of Research and Education for International Association of Privacy Professionals, added "Clearly, the biggest challenge for businesses in 2017 will be preparing for the entry into force of the GDPR, a massive regulatory framework with implications for budget and staff, carrying stiff fines and penalties in an unprecedented amount. Against a backdrop of escalating cyber events, such as the recent attack on Internet backbone orchestrated through IoT devices, companies will need to train, educate and certify their staff to mitigate personal data risks." Download Whitepaper: Fourth Annual 2017 Data Breach Industry Forecast Learn more about the five industry predictions, and issues such as ransomware and international breach notice laws in our the complimentary white paper. Click here to learn more about our fraud products, find additional data breach resources, including webinars, white papers and videos.

U.S. Communities national contract awarded to Experian to use their data and analytic solutions in order to enable state and local government agencies to help consumers and better serve their communities for the future.

New industry report highlights the convergence of business growth and fraud prevention strategies Experian has published its first annual global fraud report covering the convergence of growth strategies and fraud prevention. The report, Global Business Trends: Protecting Growth Ambitions Against Rising Fraud Threats, is designed as a guide for senior executives and fraud prevention professionals, offering new insights on how the alignment of strategies for business growth and fraud prevention can help a business grow revenues while managing risks in an increasingly virtual world. The report identifies five trends that businesses should assess and take action on to mitigate fraud and improve the customer experience in today's fast-paced, consumer-centric environment: Applying right-sized fraud solutions to reduce unnecessary customer disruption: It's time to move on from a one-size-fits-all approach that creates more customer friction than necessary. Instead, companies should apply fraud solutions that reflect the value and level of confidence needed for each transaction. This means right-sizing your fraud solutions to align with true fraud rates and commercial strategy. Having a universal view of the consumer is the core of modern fraud mitigation and marketing: Achieving a universal profile of consumer behavior — beyond the traditional 360-degree view — requires access to a combination of identity data, device intelligence, online behavior, biometrics, historical transactions and more, for consumer interactions not only with you, but across other businesses and industries as well. Companies that translate this knowledge and use it to identify consumers can distinguish a fraudster from a real customer more easily, building trust along the way. Expanding your view through a blended ecosystem: In addition to using your own first-party data sources, companies need to participate in a blended ecosystem, working across businesses and even industries. Fraudsters have access to more data than ever before, including data traditionally used to verify identities, and they use that data to create an entire digital profile. Therefore, you can no longer get to the digital interaction data you need by managing the process in a siloed manner. Achieving an expansive view of the universal consumer requires multiple data sources working together. Achieving agility and scale using service-based models: Today, more and more companies are choosing subscription-based systems rather than building in-house or implementing on-premise solutions. Continuous upgrades and the access to new risk logic that come with subscription models provide more agility and faster response to emerging threats, no matter how fast your volume grows or what products, channels or geographies you pursue. Future-proofing fraud solution choices: Companies need access to a wide variety of traditional and emerging technologies and information sources to fill in knowledge gaps and blind spots where fraudsters try to hide. The ability to modify strategies quickly and catch fraud faster while improving the customer experience is a critical aspect of fraud prevention moving forward. Bringing together these key trends, the report provides business leaders with the insight they need to fight fraud using the same consumer-focused approach currently being used to attract new customers and grow revenue. "There is a persistent mindset that fraud loss is just the cost of doing business," said Steve Platt, global EVP, Fraud and Identity, Experian. "But as fraudsters evolve, those losses are climbing, and the status quo is no longer effective or acceptable. We all need to be as forward-looking in fighting fraud as we are in business operations and marketing, and a real understanding of consumers is critical for success. We're talking about the convergence of business growth and fraud prevention, and we're pleased to provide the first report in the marketplace covering this topic." Download the full report here. The report also features an interactive Fraud Prevention Benchmark tool that companies can use to explore how these trends impact their business and how the performance of their approach measures up against industry practices. The report is relevant to functions spanning the enterprise, including C-suite executives such as chief marketing officers (CMOs), chief risk officers (CROs) and chief data officers (CDOs). The report focuses on business processes where fraud infiltrates, including new account opening, account access, money movement transactions, and emerging trends combating fraud, such as advanced fraud analytics. In each area, the report details how multiple business functions can apply responses to create business growth. Steve Platt added: "We hear from our clients that they are most successful when CMOs along with CDOs and CROs all work together to understand the customer and develop fraud management solutions that create a better overall experience." Experian was recently cited in Forrester's 2016 Vendor Landscape: Mobile Fraud Management Solutions1 report and listed as having nine out of a possible 10 capabilities needed to combat mobile fraud. Experian was also identified as one of three leading players in the fraud detection and prevention space in a new study from Juniper Research.2 Experian applied best practices to create a global report on providing fraud management solutions that allow companies to maximize profitability while providing secure, hassle-free customer interactions. Learn more about Experian’s Fraud and Identity business. 1Vendor Landscape: Mobile Fraud Management Solutions, Forrester Research, Inc., June 2016. 2Online Payment Fraud: Key Vertical Strategies & Management 2016–2020, Juniper Research, June 2016.

Is the speed of fraud threatening your business? Like many other fraud and compliance teams, your teams may be struggling to keep up with new business dynamics. The following trends are changing the way consumers do business with you: 35 percent year-over-year growth in mobile commerce More than $27 billion forecasted value of mobile payment transactions in 2016 45 percent of smartphone owners using a mobile device to make a purchase every month More than 1 billion mobile phone owners will use their devices for banking purposes by the end of 2015 In an attempt to stay ahead of fraud, systems have become more complex, more expensive and even more difficult to manage, leading to more friction for your customers. How extensive is this impact? 30 percent of online customers are interrupted to catch one fraudulent attempt One in 10 new applicants may be an imposter using breached data $40 billion of legitimate customer sales are declined annually because of tight rules, processes, etc. This rapid growth only reinforces the need for aggressive fraud prevention strategies and adoption of new technologies to prepare for the latest emerging cybersecurity threats. Businesses must continue their efforts to protect all parties’ interests. Fraudsters have what they need to be flexible and quick. So why shouldn’t businesses? Introducing CrossCore™, the first smart plug-and-play platform for fraud and identity services. CrossCore uses a single access point to integrate technology from different providers to address different dangers. When all your fraud and identity solutions work together through a single application program interface, you reduce friction and false positives — meaning more growth for your business. View our recent infographic on global fraud trends

James W. Paulsen, Chief Investment Strategist for Wells Capital Management, kicked off the second day of Experian’s Vision 2016, sharing his perspective on the state of the economy and what the future holds for consumers and businesses alike. Paulsen joked this has been “the most successful, disappointing recovery we’ve ever had.” While media and lenders project fear for a coming recession, Paulsen stated it is important to note we are in the 8th year of recovery in the U.S., the third longest in U.S. history, with all signs pointing to this recovery extending for years to come. Based on his indicators – leverage, restored household strength, housing, capital spending and better global growth – there is still capacity to grow. He places recession risk at 20 to 25 percent – and only quotes those numbers due the length of the recovery thus far. “What is the fascination with crisis policies when there is no crisis,” asks Paulsen. “I think we have a good chance of being in the longest recovery in U.S. history.” Other noteworthy topics of the day: Fraud prevention Fraud prevention continues to be a hot topic at this year’s conference. Whether it’s looking at current fraud challenges, such as call-center fraud, or looking to future-proof an organization’s fraud prevention techniques, the need for flexible and innovative strategies is clear. With fraudsters being quick, and regularly ahead of the technology fighting them, the need to easily implement new tools is fundamental for you to protect your businesses and customers. More on Regulatory The Military Lending Act has been enhanced over the past year to strengthen protections for military consumers, and lenders must be ready to meet updated regulations by fall 2016. With 1.46 million active personnel in the U.S., all lenders are working to update processes and documentation associated with how they serve this audience. Alternative Data What is it? How can it be used? And most importantly, can this data predict a consumer’s credit worthiness? Experian is an advocate for getting more entities to report different types of credit data including utility payments, mobile phone data, rental payments and cable payments. Additionally, alternative data can be sourced from prepaid data, liquid assets, full file public records, DDA data, bill payment, check cashing, education data, payroll data and subscription data. Collectively, lenders desire to assess someone’s stability, ability to pay and willingness to repay. If alternative data can answer those questions, it should be considered in order to score more of the U.S. population. Financial Health The Center for Financial Services Innovation revealed insights into the state of American’s financial health. According to a study they conducted, 57 percent of Americans are not financially healthy, which equates to about 138 million people. As they continue to place more metrics around defining financial health, the center has landed on four components: how people plan, spend, save and borrow. And if you think income is a primary factor, think again. One-third of Americans making more than $60k a year are not healthy, while one-third making less than $60k a year are healthy. --- Final Vision 2016 breakouts, as well as a keynote from entertainer Jay Leno, will be delivered on Wednesday.

Best practices and innovative strategies for banking to millennials Before we begin, a disclaimer: Banking to millennials is a long-term strategy. Many marketing campaigns will not drive immediate returns on investment, but they lay the groundwork for a lifelong, mutually beneficial relationship. Now, some good news. Millennials are just beginning their financial journey — getting ready to embark on a life that includes homes, cars, families and small businesses. Connecting with this generation today can bode well for a financial institution’s success tomorrow. With a strong relationship in place, millennials will turn to that organization when they are ready to fund their life events. Below are some key strategies that will help financial institutions build and continue banking to millennials. Keeping up with technological expectations Millennials were raised in the digital age, and therefore mobile devices are the hubs of their digital lives. They expect real-time access to their accounts for peer-to-peer payments, deposits, paying bills and customer service. Not meeting their digital expectations could drive them to seek another — more technology-oriented — financial institution that embraces CNP, mobile apps and social media. Authentic and targeted marketing messaging Millennials expect targeted messaging. Generic, catchall offers of the past fall flat for them. They want banks to figure out who they are, what they need and how they can access it with the tap of a finger. Additionally, messages to millennials should have a genuine voice that advises and supports them in achieving their goals. Many millennials are interested in taking control of their financial lives but are not prepared to do so. This is a great opportunity for financial institutions to introduce themselves. Connect millennials to something bigger Earning a millennial’s trust is one of the greatest challenges for financial institutions. While money is important, millennials are motivated by becoming a part of something bigger than themselves. Institutions can connect with millennials by creating opportunities to give back or pay-it-forward. Examples include encouraging growth in underbanked markets, such as lending circles, peer-to-peer lending and small-business lending, or partnering with local universities and nonprofits. Strategic segmentation Millennials are the most diverse population group — yet strategic segmentation is still possible. One ideal segment is recent college graduates. As a group, they yield a much different profile than their counterparts without degrees. These ambitious millennials are more likely to focus on life choices that require major financial considerations, such as getting married, having children, buying their first home and earning higher salaries. These life events will require a diverse set of financial services products, and millennials will turn to the institution that has gained their trust first. Millennials are one of the most important markets as financial institutions look to invest in future, long-term growth. Financial institutions need to show millennials that they’re committed to listening and to laying the groundwork for relationships that will help them achieve their dreams. Remember, though, reaching this audience is not about an immediate return on investment but rather a long-term strategy to develop trust and brand preference. Begin the relationship now to reap the rewards later. For more insights and innovative strategies on how to best market and develop a strong relationship with millennials, download our recent white paper, Building lasting relationships with millennials.

Proven identity and device authentication to minimize identity tax return fraud Identity fraud places an enormous burden on its victims and presents a challenge to businesses, organizations and government agencies, including the IRS and all state revenue authorities. Tax return fraud occurs when an attacker uses a consumer’s stolen Social Security number and other personal information to file a tax return, often claiming a significant refund. The IRS is challenged by innovative fraudsters continually trying to outsmart its current risk strategies around prevention, detection, recovery and victim assistance. And with the ever-increasing number of identity data compromised and tax return fraud victims, it’s necessary to question whether tax preparation companies are doing all they can to keep personally identifiable information (PII) secure and screen for fraud before forms are submitted. “ID theft isn’t just credit card fraud,” said Rod Griffin, Director of Public Education for Experian. A recent Experian online survey indicated that nearly 76 percent of consumers are familiar with ID theft and tax fraud — up significantly from the past two years. And 28 percent of those surveyed have been a victim or know a victim of tax fraud. To protect all parties’ interests, tax preparation agencies are challenged by today’s savvy fraudsters who have reaped the benefits of recent breaches. In order to protect consumers, organizations need to apply comprehensive, data-driven intelligence to help thwart identity fraud and the use of stolen identity data via fraudulent returns. The key to securing transactions, reducing friction and providing a consistently satisfying customer experience, online and offline, is authenticating consumers in a clear and frictionless environment. As a result, it’s necessary to have reliable customer intelligence based on both high-quality contextual identity and device attributes alongside other authentication performance data. Comprehensive customer intelligence means having a holistic, bound-together view of devices and identities that equips companies and agencies with the tools to balance cost and risk without increasing transactional friction. Businesses and agencies must not rely on a singular point of customer intelligence gathering and decisioning, but must move to more complex device identification and out-of-wallet verification procedures. Effective solutions typically involve a layered approach with several of the following: Identity transaction link analysis and risk attribute derivation Device intelligence and risk assessment Credit and noncredit data and risk attributes Multifactor authentication, using one-time passcodes via SMS messaging Identity risk scores Dynamic knowledge-based authentication questions Traditional PII validation and verification Biometrics and remote document verification Out-of-band alerts, communications and confirmations Contextual account, transaction and channel purview Additionally, government agencies must adhere to recognized standards, such as those prescribed by the National Institute of Standards and Technology to establish compliance. The persistent threat of tax fraud highlights the urgent need for businesses and agencies to continue educating consumers and more importantly, to improve the strategic effectiveness of their current solutions processes. Learn more about Experian Fraud and Identity Solutions, including government-specific treatments, and how the most effective fraud prevention and identity authentication strategy leverages multiple detection capabilities to highlight attackers while enabling a seamless, positive experience for legitimate consumers.

Ensure you’re protecting consumer data privacy Data Privacy Day is a good reminder for consumers to take steps to protect their privacy online — and an ideal time for organizations to ensure that they are remaining vigilant in their fight against fraud. According to a new study from Experian Consumer Services, 93 percent of survey respondents feel identity theft is a growing problem, while 91 percent believe that people should be more concerned about the issue. Online activities that generate the most concern include making an online purchase (73 percent), using public Wi-Fi (69 percent) and accessing online accounts (69 percent). Consumers are vigilant while online Most respondents are concerned they will fall victim to identity theft in the future (71 percent), resulting in a generally proactive approach to protecting personal information. In fact, almost 50 percent of respondents say they are taking more precautions compared with last year. Ninety-one percent take steps to secure physical information, such as shredding documents, while also securing digital information (using passwords and antivirus software). Many consumers also make sure to check their credit report (33 percent) and bank account statements (76 percent) at least once per month. There’s still room for consumers to be safer Though many consumers are practicing good security habits, some aren’t: More than 50 percent do not check to see if a Website is secure Fifty percent do not have all their Web-enabled devices password-protected because it is a hassle to enter a password (30 percent) or they do not feel it is necessary (25 percent) Fifty-five percent do not close the Web browser when they are finished using an online account Additionally, 15 percent keep a written record of passwords and PINs in their purse or wallet or on a mobile device or computer Businesses need to be responsible when it comes data privacy Customer-facing businesses must continue efforts to educate consumers about their role in breach and fraud prevention. They also need to be responsible and apply comprehensive, data-driven intelligence that helps thwart both breaches and the malicious use of breached information and protect all parties’ interests. Nearly 70 percent of those polled in a 2015 Experian–Ponemon Institute study said that the increased visibility and media reporting of breaches, including payment-related incidents, have caused their organizations to step up data security efforts. Experian Fraud & ID is uniquely positioned to provide true customer intelligence by combining identity authentication with device assessment and monitoring from a single integrated provider. This combination provides the only true holistic view of the customer and allows organizations to both know and recognize customers and to provide them with the best possible experience. By associating the identities and the devices used to access services, the true identity can be seen across the customer journey. This unique and integrated view of identity and device delivers proven superior performance in authentication, fraud risk segmentation and decisioning. For more insights into how businesses are responding to breach activities, download our recent white paper, Data confidence realized: Leveraging customer intelligence in the age of mass data compromise. For more findings from the study, view the results here.