Telecommunications, Cable & Utilities

Telecommunications, Cable & Utilities

Everyone loves a story. Correction, everyone loves a GOOD story. A customer journey map is a fantastic tool to help you understand your customer’s story from their perspective. Perspective being the operative word. This is not your perspective on what YOU think your customer wants. This is your CUSTOMER’S perspective based on actual customer feedback – and you need to understand where they are from those initial prospecting and acquisition phases all the way through collections (if needed). Communication channels have expanded from letters and phone calls to landlines, SMS, chat, chat bots, voicemail drops, email, social media and virtual negotiation. When you create a customer journey map, you will understand what channel makes sense for your customer, what messages will resonate, and when your customer expects to hear from you. While it may sound daunting, journey mapping is not a complicated process. The first step is to simply look at each opportunity where the customer interacts with your organization. A best practice is to include every department that interacts with the customer in some way, shape or form. When looking at those touchpoints, it is important to drill down into behavior history (why is the customer interacting), sociodemographic data (what do you know about this customer), and customer contact patterns (Is the customer calling in? Emailing? Tweeting?). Then, look at your customer’s experience with each interaction. Again, from the customer’s viewpoint: Was it easy to get in touch with you? Was the issue resolved or must the customer call back? Was the customer able to direct the communication channel or did you impose the method? Did you offer self-serve options to the right population? Did you deliver an email to someone who wanted an email? Do you know who prefers to self-serve and who prefers conversation with an agent, not an IVR? Once these two points are defined: when the customer interacts and the customer experience with each interaction, the next step is simply refining your process. Once you have established your baseline (right channel, right message, right time for each customer), you need to continually reassess your decisions. Having a system in place that allows you to track and measure the success of your communication campaigns and refine the method based on real-time feedback is essential. A system that imports attribute – both risk and demographic – and tracks communication preferences and campaign success will make for a seamless deployment of an omnichannel strategy. Once deployed, your customer’s experience with your company will be transformed and they will move from a satisfied customer to one that is a fan and an advocate of your brand.

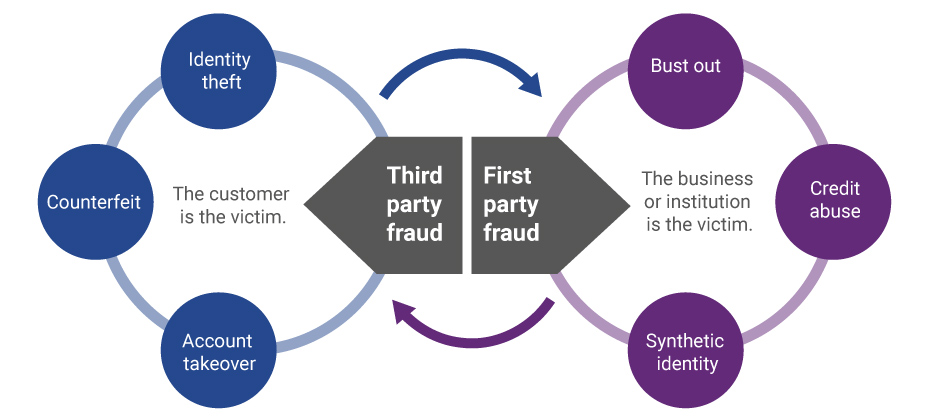

Evolution of first-party fraud to third Third-party and first-party schemes are now interchangeable, and traditional fraud detection practices are less effective in fighting these evolving fraud types. Fighting this shifting problem is a challenge, but it isn’t impossible. To start, incorporate new and more robust data into your identity verification program and provide consistent fraud classification and tagging. Learn more>

It should come as no surprise that the process of trying to collect on past-due accounts has been evolving. We’ve seen the migration from traditional mail and outbound calls, to offering an electronic payment portal, to digital collections and virtual negotiators. Being able to get consumers who have past-due debt on the phone to discuss payments is almost impossible. In fact, a recent informal survey divulged a success rate of a 15% contact rate to be considered the best by several first-party collectors; most reported contact rates in the 8%-range. One can only imagine what it must be like for collection agencies and debt buyers. Perhaps, inviting the consumer to establish a non-threatening dialog with an online system can be a better approach? Now that collectors have had time to test virtual collections, we’ve collected some data points. Conversion rates, revisits, and time of day An analysis of several clients found that on average 52% of consumers that visit a digital site will proceed to a payment schedule if the right offer is made. 21% of the visits were outside the core hours of 8 a.m. to 8 p.m., an indication that consumers were taking advantage of the flexibility of reaching out at any time of the day or night to explore their payment and settlement options. The traditional business hours don’t always work. Here is where it really gets interesting, and invites a clear comparison to the traditional phone calls that collectors make trying to get the consumer to commit to a payment plan on the line. Of the consumers that committed to a payment plan, only 56% did it in a single visit. The remaining 44% that committed to payments did so mostly later that day, or on a subsequent day. This strongly suggests they either took time to check their financial status, or perhaps asked a friend or family to help with the payment. In other words, rather than refusing to agree to an instantaneous agreement pressured by a collector, the consumer took time to reflect and decide what was the best course of action to settle the amount due. On a similar note, the attrition rate of “Promises to Pay” were 24% lower using online digital solutions versus the traditional collector phone call. This would be consistent with more time to agree to a payment plan that could be met, rather than weakly agreeing to a collector phone call just to get the collector off the phone. Another possible reason for a lower attrition rate may be that a well-defined digital collection solution can send out reminders to consumers via email or text in advance of the next scheduled payment, so that the consumer can be reminded to have the funds available when the next payment hits their account. For accounts where settlement offers are part of the mix, a higher percentage of balances is being resolved versus the collection floor. In fact, the average payment improvement is 12% over what collectors tend to get on the collections floor. The reason for this significant change is unclear, but the suspicion is that a digital collection solution will negotiate stronger than a collector, who is often moving to the bottom of an acceptable range too soon. What's next? Further assessing the consumer’s needs and capabilities during the negotiation session will undoubtedly be a theme going forward. Logical next steps will include a “behind-the-scenes” look at the consumer’s entire credit picture to help the creditor craft an optimal settlement amount that both the consumer can meet, and at the same time optimizes recovery. Potential impact to credit scores will also come into the picture. Depending on where the consumer and his past-due debt is in the credit lifecycle, being able to reasonably forecast the negative impact of a missed payment can act as an additional argument for making a past-due or delinquent payment now. As more financial institutions test this new virtual approach, we anticipate customer satisfaction and resolutions will continue to climb.

We regularly hear from clients that charge-offs are increasing and they’re struggling to keep up with the credit loss. Many clients use the same debt collection strategy they’ve used for years – when businesses or consumers can’t repay a loan, the creditor or collection agency aggressively contacts them via phone or mail to obtain repayment – never considering the customer experience for the debtor. Our data shows that consumers accounted for $37.24 billion in bankcard charge-offs in Q2 2017, a 17.1 percent increase from Q2 2016. Absorbing credit losses at such a high rate can impact the sustainability of the institution. Clearly the process could use some adjusting. Traditionally, debt collection has been solely about the money. The priority was ensuring that as much of the outstanding debt as possible was repaid. But collecting needs to be about more than that. It also should focus on the customer and his or her individual situation. When it comes to debt collection, customers should not all be treated the same way. I recently shared some tips in Credit Union Business Magazine about how to actively engage and collect from members. The same holds true for other financial institutions – they need to know the difference between a customer who has simply forgotten to make a payment and one who is dealing with financial hardship. As an example, if a person is current on his or her mortgage payment but has slipped behind on his or her credit card payment, that doesn’t necessarily signify financial hardship. It’s an opportunity to work with the customer to manage the debt and get back to current. Modern financial institutions build acquisition and customer management strategies targeted at individuals, so why should the collection process be any different? The challenge is keeping the customer at the center while also managing against potential increases in delinquencies. This holistic approach may be slightly more complex, but technology and analytics will simplify the process and bring about a more engaging experience for customers. The Power of Data and Technology Instead of relying on the same outdated collections approach – which results in uncomfortable exchanges on the phone that don’t ensure repayment –leverage data to your advantage. The data and technology exists to help you make more informed decisions, such as: What’s the most effective communication channel to reach the defaulting customer? When should you contact him or her? How often? The best course of action could be high-touch outreach, but sometimes doing nothing is the right approach. It all depends on the situation. Data and analytics can help uncover which customers are most likely to pay on their own and those who may need a little more help, allowing you to adjust your treatment strategy accordingly. By catering to the preferences of the customer, there’s a greater chance for a positive experience on both sides. The results: less charge-off debt, higher customer satisfaction and a stronger relationship. Explore the Digital Age In 2016, 36 million Americans made some form of mobile payment—paying a bill, purchasing something online, or paying for fast food, or making a Mobile Wallet purchase at a retailer. By 2020, nearly 184 million consumers will have done so, according to Aite. Consumers expect and deserve convenience. In the digital world, financial institutions have an opportunity to provide that expectation and then some. Imagine a customer being able to negotiate and manage his or her past-due account virtually, in the privacy of his or her own home, when it’s most convenient, to set their payment dates and terms. Luckily, the technology exists to make this vision a reality. Customers, not money, need to be at the heart of every debt collections strategy. Gone are the days of mass phone calls to debtors. That strategy made consumers unhappy, embarrassed and resentful. Successful debt collection comes down to a basic philosophy: Treat customers and his or her unique situation individually rather than as a portfolio profile. The creditors who live by that philosophy have an opportunity to reap the rewards on the back-end.

Millennials have long been the hot topic over the course of the past few years with researchers, brands and businesses all seeking to understand this large group of people. As they buy homes, start families and try to conquest their hefty student loan burdens, all will be watching. Still, there is a new crew coming of age. Enter Gen Z. It is estimated that they make up ¼ of the U.S. population, and by 2020 they will account for 40% of all consumers. Understanding them will be critical to companies wanting to succeed in the next decade and beyond. The oldest members of this next cohort are between the ages of 18 and 20, and the youngest are still in elementary school. But ultimately, they will be larger than the mystical Millennials, and that means more bodies, more buying power, more to learn. Experian recently took a first look at the oldest members of this generation, seeking to gain insights into how they are beginning to use credit. In regards to credit scores, the eldest Gen Z members sported a VantageScore® credit score of 631 in 2016. By comparison, younger Millennials were at 626 and older Millennials were at 638. Given their young age, Gen Z debt levels are low with an average debt-to-income at just 5.7%. Their tradelines largely consist of bankcards, auto and student loans. Their average income is at $33.8k. Surprisingly, there was a very small group of Gen Z already on file with a mortgage, but this figure was less than .5%. Auto loans were also small, but likely to grow. Of those Gen Z members who have a credit file, an estimated 12% have an auto trade. This is just the beginning, and as they age, their credit files will thicken, and more insights will be gained around how they are managing credit, debt and savings. While they are young today, some studies say they already receive about $17 a week in allowance, equating to about $44 billion annually in purchase power in the U.S. Factor in their influence on parental or household purchases and the number could be closer to $200 billion! For all brands, financial services companies included, it is obvious they will need to engage with this generation in not just a digital manner, but a mobile manner. They are being raised in an era of instant, always-on access. They expect a quick, seamless and customized mobile experience. Retailers have 8 seconds or less — err on the side of less — to capture their attention. In general, marketers and lenders should consider the following suggestions: Message with authenticity Maintain a long-term vision Connect them with something bigger Provide education for financial literacy and of course Keep up with technological advances. Learn more by accessing our recorded webinar, A First Look at Gen Z and Credit.

Mitigating synthetic identities Synthetic identity fraud is an epidemic that does more than negatively affect portfolio performance. It can hurt your reputation as a trusted organization. Here is our suggested 4-pronged approach that will help you mitigate this type of fraud: Identify how much you could lose or are losing today to synthetic fraud. Review and analyze your identity screening operational processes and procedures. Incorporate data, analytics and cutting-edge tools to enable fraud detection through consumer authentication. Analyze your portfolio data quality as reported to credit reporting agencies. Reduce synthetic identity fraud losses through a multi-layer methodology design that combats both the rise in synthetic identity creation and use in fraud schemes. Mitigating synthetic identity fraud>

The creation of synthetic identities (synthetic id) relies upon an ecosystem of institutions, data aggregators, credit reporting agencies and consumers. All of which are exploited by an online and mobile-driven market, along with an increase in data breaches and dark web sharing. It’s a real and growing problem that’s impacting all markets. With significant focus on new customer acquisition and particular attention being paid to underbanked, emerging, and new-to-country consumers, this poses a large threat to your onboarding and customer management policies, in addition to overall profitability. Synthetic identity fraud is an epidemic that does more than negatively affect portfolio performance. It can hurt your reputation as a trusted organization and expose institutions, like yours, as paths of lesser resistance for fraudsters to use in the creation and farming of synthetic identities. Here is a suggested four-pronged approach to mitigate this type of fraud: The first step is knowing your risk exposure to synthetic identity fraud. Identify how much you could lose or are losing today using a targeted segmentation analysis to examine portfolios or customer populations. Next, review your front- and back-end identity screening operational processes and procedures and analyze that information to ensure you have industry best practices, procedures and verification tools deployed. Then incorporate data, analytics and some of the industry’s cutting edge tools. This enables you to perform targeted consumer authentication and identify opportunities to better capture the majority of fraud and operational waste. Lastly, ensure your organization is part of the solution – not the problem. Analyze your portfolio data quality as reported to credit reporting agencies and then minimize your exposure to negative compliance audit results and reputational risk. Our fraud and identity management consultants can help you reduce synthetic identity fraud losses through a multilayer methodology design that combats the rise in synthetic identity creation and use in fraud schemes.

On June 7, the Consumer Financial Protection Bureau (CFPB) released a new study that found that the ways “credit invisible” consumers establish credit history can differ greatly based on their economic background. The CFPB estimated in its May 2015 study "Data Point: Credit Invisibles" that more than 45 million American consumers are credit invisible, meaning they either have a thin credit file that cannot be scored or no credit history at all. The new study reviewed de-identified credit records on more than one million consumers who became credit visible. It found that consumers in lower-income areas are 240 percent more likely to become credit visible due to negative information, such as a debt in collection. The CFPB noted consumers in higher-income areas become credit visible in a more positive way, with 30 percent more likely to become credit visible by using a credit card and 100 percent more likely to become credit visible by being added as a co-borrower or authorized user on someone else’s account. The study also found that the percentage of consumers transitioning to credit visibility due to student loans more than doubled in the last 10 years. CFPB’s research highlights the need for alternative credit data The new study demonstrates the importance of moving forward with inclusion of new sources of high-quality financial data — like on-time payment data from rent, utility and telecommunications providers — into a consumer’s credit file. Experian recently outlined our beliefs on the issue in comments responding to the CFPB’s Request for Information on Alternative Data. As a brand, we have a long history of using alternative credit data to help lenders make better lending decisions. Extensive research has shown that there is an immense opportunity to facilitate greater access to fair and affordable credit for underserved consumers through the inclusion of on-time telecommunications, utility and rental data in credit files. While these consumers may not have a traditional credit history, many make on-time payments for telephone, rent, cable, power or mobile services. However, this data is not typically being used to enhance traditional credit files held by the nationwide consumer reporting agencies, nor is it being used in most third-party or custom credit scoring models. Further, new advances in financial technology and data analytics through account aggregation platforms are also integral to the credit granting process and can be applied in a manner to broaden access to credit. Experian is currently using account aggregation software to obtain consumer financial account information for authentication and income verification to speed credit decisions, but we are looking to expand this technology to increase the collection and utilization of alternative data for improving credit decisions by lenders. Policymakers should act to help credit invisible consumers While Experian continues to work with telecommunications and utility companies to facilitate the furnishing of on-time credit data to the nationwide consumer reporting agencies, regulatory barriers continue to exist that deter utility and telecommunications companies from furnishing on-time payment data to credit bureaus. To help address this issue, Congress is currently considering bipartisan legislation (H.R. 435, The Credit Access and Inclusion Act of 2017) that would amend the FCRA to clarify that utility and telecommunication companies can report positive credit data, such as on-time payments, to the nation' s credit reporting bureaus. The legislation has bipartisan support in Congress and Experian encourages lawmakers to move forward with this important initiative that could benefit tens of millions of American consumers. In addition, Experian believes policymakers should more clearly define the term alternative data. In public policy debates, the term "alternative data" is a broad term, often lumping data sources that can or have been proven to meet regulatory standards for accuracy and fairness required by both the Fair Credit Reporting Act and the Equal Credit Opportunity Act with data sources that cannot or have not been proven to meet these standards. In our comment letter, Experian encourages policymakers to clearly differentiate between different types of alternative data and focus the consumer and commercial credit industry on public policy recommendations that will increase the use of those sources of data that have or can be shown to meet legal and societal standards for accuracy, validity, predictability and fairness. More info on Alternative Credit Data More Info on Alternative Financial Services

The 1990s brought us a wealth of innovative technology, including the Blackberry, Windows 98, and Nintendo. As much as we loved those inventions, we moved on to enjoy better technology when it became available, and now have smartphones, Windows 10 and Xbox. Similarly, technological and modeling advances have been made in the credit scoring arena, with new software that brings significant benefits to lenders who use them. Later this year, FICO will retire its Score V1, making it mandatory for those lenders still using the old software to find another solution. Now is the time for lenders to take a look at their software and myriad reasons to move to a modern credit score solution. Portfolio Growth As many as 70 million Americans either have no credit score or a thin credit file. One-third of Millennials have never bothered to apply for a credit card, and the percentage of Americans under 35 with credit card debt is at its lowest level in more than 25 years, according to the Federal Reserve. A recent study found that Millennials use cash and debit cards much more than older Americans. Over time, Millennials without credit histories could struggle to get credit. Are there other data sets that provide a window into whether a thin file consumer is creditworthy or not? Modern credit scoring models are now being used in the marketplace without negatively impacting credit quality. For example, the VantageScore® credit score allows for the scoring of 30 million to 35 million more people consumers who are typically unscoreable by other traditional generic credit models. The VantageScore® credit score does this by using a broader, deeper set of credit file data and more advanced modeling techniques. This allows the VantageScore® credit score model to more accurately predict unique consumer behaviors—is the consumer paying his utility bill on time?—and better evaluate thin file consumers. Mitigate Risk In today’s ever-changing regulatory landscape, lenders can stay ahead of the curve by relying on innovative credit score models like the VantageScore® credit score. These models incorporate the best of both worlds by leaning on innovative scoring analytics that are more inclusive, while providing marketplace lenders with assurances the decisioning is both statistically sound and compliant with fair lending laws. Newer solutions also offer enhanced documentation to ease the burden associated with model risk management and regulatory compliance responsibilities. Updated scores Consumer credit scores can vary depending on the type of scoring model a lender uses. If it's an old, outdated version, a consumer might be scored lower. If it's a newer, more advanced model, the consumer has a better shot at being scored more fairly. Moving to a more advanced scoring model can help broaden the base of potential borrowers. By sticking to old models—and older scores—a sizable number of consumers are left at a disadvantage in the form of a higher interest rate, lower loan amount or even a declined application. Introducing advanced scoring models can provide a more accurate picture of a consumer. As an example, for many of the newest consumer risk models, like FICO Score 9, a consumer’s unpaid medical collection agency accounts will be assessed differently from unpaid non-medical collection agency accounts. This isn't true for most pre-2012 consumer risk score versions. Each version contains different nuances for increasing your score, and it’s important to understand what they are. Upgrading your credit score to the latest VantageScore® credit score or FICO solution is easier than you think, with a switch to a modern solution taking no longer than eight weeks and your current business processes still in place. Are you ready to reap the rewards of modern credit scoring?

The final day of Vision 2017 brought a seasoned group of speakers to discuss a wide range of topics. In just a few short hours, attendees dove into a first look at Gen Z and their use of credit, ecommerce fraud, the latest in retail, the state of small business and leadership. Move over Millennials – Gen Z is coming of credit age Experian Analytics leaders Kelley Motley and Natasha Madan gave audience members an exclusive look at how the first wave of Gen Z is handling and managing credit. Granted most of this generation is still under the age of 18, so the analysis focused on those between the ages of 18 to 20. Yes, Millennials are still the dominant generation in the credit world today, standing strong at 61 million individuals. But it’s important to note Gen Z is sized at 86 million, so as they age, they’ll be the largest generation yet. A few stats to note about those Gen Z individuals managing credit today: Their average debt is $12,679, compared to younger Millennials (21 to 27) who have $65,473 in debt and older Millennials (28 to 34) who sport $121,460. Given their young age, most of Gen Z is considered thin-file (less than 5 tradelines) Average Gen Z income is $33,000, and average debt-to-income is low at 5.7%. New bankcard balances are averaging around $1,574. As they age, acquire mortgages and vehicles, their debt and tradelines will grow. In the meantime, the speakers provided audience members a few tips. Message with authenticity. Think long-term with this group. Maintain their technological expectations. Build trust and provide financial education. State of business credit and more on the economy Moody’s Cris deRitis reiterated the U.S. economy is looking good. He quoted unemployment at 4.5%, stating “full employment is here.” Since the recession, he said we’ve added 15 million jobs, noting we lost 8 million during the recession. The great news is that the U.S. continues to add about 200,000 jobs a month, and that job growth is broad-based. Small business loans are up 10% year-to-date vs. last year. While there has been a tremendous amount of buzz around small business, he adds that most job creation has come from mid0size business (50 to 499 employees). The case for layered fraud systems Experian speaker John Sarreal shared a case study that revealed by layering on fraud products and orchestrating collaboration, a business can go from a string 75% fraud detection rate to almost 90%. Additionally, he commented that Experian is working to leverage dark web data to mine for breached identity data. More connections for financial services companies to make with mobile and social Facebook speaker Olivia Basu reinforced the need for all companies to be thinking about mobile. “Mobile is not about to happen,” she said. “Mobile is now. Mobile is everything. You look at the first half of 2017 and we’re seeing 40% of all purchases are happening on mobile devices.” Her challenge to financial services companies is to make marketing personal again, and of course leverage the right channels. Experian Sr. Director of Credit Marketing Scott Gordon commented on Experian’s ability to reach consumers accurately – whether that be through direct or digital delivery channels. A great deal of focus has been around person-based marketing vs. leveraging the cookie. -- The Vision conference was capped off with a keynote speech from legendary quarterback and Super Bowl MVP Tom Brady. He chatted about the details of this past season, and specifically the comeback Super Bowl win in February 2017. He additionally talked about leadership and what that means to creating a winning team and organization. -- Multiple keynote speeches, 65 breakout sessions, and hours of networking designed to help all attendees ready themselves for growing profits and customers, step up to digital, regulatory and fraud challenges, and capture the latest data insights. Learn more about Experian’s annual Vision conference.

In just a few short hours, Vision attendees immersed themselves into the depths of the economy, risk models, specialty finance data, credit invisibles, student loan data, online marketplace lending and more. The morning kicked off with one of the most respected and trusted macroeconomists in the U.S., Diane Swonk. With a rap sheet filled with advising central banks and multinational companies, Swonk treated a packed house to a look back on what has transpired in the U.S. economy since the Great Recession, as well as launching into current state and speculating on the months ahead. She described the past decade not as “lost, but rather lagging.” She went onto to say this past year was transitional, and while markets slowed slightly during the months leading up the U.S. presidential election, good things are happening: We’ve finally broken out of the 2% wage rut Recruiting on college campuses has picked up The labor force is growing Debt-to-income levels have returned to where they were prerecession and Investment is coming back. “I believe we’ll see growth over 2% this year,” said Swonk. Still, change is underway. She commented on how the way U.S. consumer spending is changing, and of course we’re seeing a restructuring in the retail space. While JC Penney announces store closings, you simultaneously see Amazon moving from “click to brick,” dabbling in the opening of some actual storefronts. Globally, she said the economy is the strongest it has been in eight years. She closed by noting there is a great deal of political change and unrest in the world today, but says, “Never underestimate our abilities when we tap our human capital.” -- More than 100 attendees filled a room to hear about the current trends and the future of online lending with featured guests from Oliver Wyman, Marlette Funding and Lending USA. While speakers commented on the “hiccup” in the space last year with some layoffs and mergers, volume has continued to double every year for the past several years with roughly $40 billion in cumulative originations today. Panelists discussed the use of alternative data to decision, channel bias, the importance of partnerships and how the market will see fewer and fewer players offering just one product specialty. “It is expensive to acquire customers, so you don’t just want to have one product to sell, but rather a range,” said Sharat Shankar of Lending USA. -- The numbers in the student lending universe are astounding. In a session focused on the U.S. student loan market, new Experian data reveals there is $1.49 billion in total student loan outstandings. In fact, total outstandings have grown 21% over the past four years, while the number of trades have only grown 4%. Costs are skyrocketing. The average balance per trade has grown 17% over the past four years. “We don’t ration education in this country,” said Joe DePaulo of College Ave. Student Loans. “We give everyone access to liquidity when it comes to federal student loans – and it’s not like that in other countries.” While DePaulo notes the access is great, offering many students the opportunity to obtain higher education, he says the problem is with disclosures. Guardians are often the individuals filling out the FAFSA, but the students inherit the loans. Students, he says, rarely understand how much their monthly payment will ultimately be after graduation. For every $10,000 in student loans, he says that will generally equate to a $100 monthly payment. -- Tomorrow, Vision attendees will be treated to more breakout sessions and a concluding keynote with legendary quarterback Tom Brady.

So many insights and learnings to report after the first full day of 2017 Vision sessions. From the musings shared by tech engineer and pioneer Steve Wozniak, to a panel of technology thought leaders, to countless breakout sessions on a wide array of business topics … here’s a look at our top 10 from the day. A mortgage process for the digital age. At last. In his opening remarks, Experian President of Credit Services Alex Lintner asked the audience to imagine a world when applying for a mortgage simply required a few clicks or swipes. Instead of being sent home to collect a hundred pieces of paper to verify employment, income and assets, a consumer could click on a link and provide a few credentials to verify everything digitally. Finally, lenders can make this a reality, and soon it will be the only way consumers expect to go through the mortgage process. The global and U.S. economies are stable. In fact, they are strong. As Experian Vice President of Analytics Michele Raneri notes, “the fundamentals and technicals look really solid across the countries.” While many were worried a year ago that Brexit would turn the economy upside down, it appears everything is good. Consumer confidence is high. The Dow Jones Index is high. The U.S. unemployment rate is at 4.7%. Home prices are up year-over-year. While there has been a great deal of change in the world – politically and beyond – the economy is holding strong. The rise of the micropreneur. This term is not officially in the dictionary … but it will be. What is it? A micropreneur is a business with 0 to 4 employees bringing in no more than $200k in annual revenue. But the real story is that numbers show microbusiness are improving on many fronts when it comes to contribution to the economy and overall performance compared to other small businesses. Keep an eye on these budding business people. Fraud is running fierce. Synthetic identity losses are estimated in the hundreds of millions annually, with 50% year-over year growth. Criminals are now trying to use credit cleaners to get tradelines removed from used Synthetic IDs. Oh, and it is essential for businesses to ready themselves for “Dark Web” threats. Experts advise to harden your defenses (and play offense) to keep pace with the criminal underground. As soon as you think you’ve protected everything, the criminals will find a gap. The cloud is cool and so are APIs. A panel of thought leaders took to the main stage to discuss the latest trends in tech. Experian Global CIO Barry Libenson said, “The cloud has changed the way we deliver services to our customers and clients, making it seamless and elastic.” Combine that with API, and the goal is to ultimately make all Experian data available to its customers. Experian President of Decision Analytics Steve Platt added, “We are enabling you to tap into what you need, when you need it.” No need to “rip and replace” all your tech. Expect more regulation – and less. A panel of regulatory experts addressed the fast-changing regulatory environment. With the new Trump administration settling in, and calls for change to Dodd-Frank and the Consumer Financial Protection Bureau (CFPB), it’s too soon to tell what will unfold in 2017. CFPB Director Richard Cordray may be making a run for governor of Ohio, so he could be transitioning out sooner than the scheduled close of his July 2018 term. The auto market continues to cruise. Experian’s auto expert, Malinda Zabritski, revealed the latest and greatest stats pertaining to the auto market. A few numbers to blow your mind … U.S. passenger cars and light trucks surpassed 17 million units for the second consecutive year Most new vehicle buyers in the U.S. are 45 years of age or older Crossover and sport utility vehicles remain popular, accounting for 40% of the market in 2016 – this is also driving up finance payments since these vehicles are more expensive. There are signs the auto market is beginning to soften, but interest rates are still low, and leasing is hot. Defining alternative data. As more in the industry discuss the need for alternative data to decision, it often gets labeled as something radical. But in reality, alternative data should be simple. Experian Sr. Director of Government Affairs Liz Oesterle defined it as “getting more financial data in the system that is predicted, validated and can be disputed.” #DeathtoPasswords – could it be a reality? It’s no secret we live in a digital world where we are increasingly relying on apps and websites to manage our lives, but let’s throw out some numbers to quantify the shift. In 2013, the average U.S. consumer had 26 online accounts. By 2015, that number increased to 118 online accounts. By 2020, the average person will have 207 online accounts. When you think about this number, and the passwords associated with these accounts, it is clear a change needs to be made to managing our lives online. Experian Vice President David Britton addressed his session, introducing the concept of creating an “ultimate consumer identity profile,” where multi-source data will be brought together to identify someone. It’s coming, and all of us managing dozens of passwords can’t wait. “The Woz.” I guess you needed to be there, but let’s just say he was honest, opinionated and notes that while he loves tech, he loves it even more when it enables us to live in the “human world.” Too much wonderful content to share, but more to come tomorrow …

In a May 4 speech before the ACA International Conference in Washington, FCC Commissioner Michael O’Rielly criticized the FCC’s past decisions on Telephone Consumer Protection Act (TCPA) and outlined his vision on the direction that the new Commission should head to provide more certainty to businesses. Commissioner O’Rielly noted that prior decisions by the FCC and courts have “expanded the boundaries of TCPA far beyond what I believe Congress intended.” He said that the new leadership at the Commission and a new Bureau head overseeing TCPA, provides the FCC with the opportunity to “undo the misguided and harmful TCPA decisions of the past that exposed legitimate companies to massive legal liability without actually protecting consumers.” O’Rielly laid out three principles that he thought would help to frame discussions and guide the development of replacement rules. First, he said that legitimate businesses need to be able to contact consumers to communicate information that they want, need or expect to receive. This includes relief for informational calls, as well as valid telemarketing calls or texts. Second, Commissioner O’Rielly said that FCC should change the definition of an autodialer so that valid callers can operate in an efficient manner. He went on to say that if FCC develops new rules to clarify revocation of consent, it should do so in a clear and convenient way for consumers, but also does not upend standard best practices of legitimate companies. Third, O’Rielly said that the FCC should focus on actual harms and bad actors, not legitimate companies. While Commissioner O’Rielly’ s comments signal his approach to TCPA reform, it is important to note that FCC action on the issue us unlikely to happen overnight. A rule must be considered by the Commission, which will have to allow for public notice and comment. Experian will continue to monitor regulatory and legislative developments on TCPA.

It should come as no surprise that reaching consumers on past-due accounts by traditional dialing methods is increasingly ineffective. The new alternative, of course, is to leverage digital channels to reach and collect on debts. The Past: Dialing for dollars. Let’s take a walk down memory lane, shall we? The collection approach used for many years was to initially send the consumer a collection letter recapping the obligation and requesting payment, usually when an account was 30 days late. If the consumer failed to respond, a series of dialing attempts were then made, trying to reach the consumer and resolve the debt. Unfortunately, this approach has become less effective through the years due to several reasons: The use of traditional landlines continues to drop as consumers shift to cell and Voice Over Internet Protocol (VOIP) services. The cost of reaching consumers by cell is more costly since predictive dialers can’t be used without prior consent, and the obtaining and maintaining consent presents its own set of tricky challenges. Consumers simply aren’t answering their phones. If they think a bill collector is calling, they don’t pick up. It’s that simple. In fact, here is a breakdown by age group that Gallup published in 2015, highlighting the weakness of traditional phone-dialing. The Present: Hello payment portal. With the ability to get the consumer on the phone to negotiate a payment on the wane, the logical next step is to go digital and use the Internet or text messaging to reach the consumer. With 71 percent of consumers now using smartphones and virtually everyone having an Internet connection, this can be a cost-effective approach. Some companies have already implemented an electronic payment portal whereby a consumer can make a payment using his or her PC or smartphone. Usually this is prompted by a collection letter, or if permitted by consumer consent, a text message to their smartphone. The Future: Virtual negotiation. But what if the consumer wants to negotiate different terms or payment plans? What if they want to try and settle for less than the full amount? In the past – and for most companies operating today – this translates into a series of emails or letters being exchanged, or the consumer must actually speak to a debt collector on the phone. And let’s be honest, the consumer generally does not want to speak to a collector on the phone. Fortunately, there is a new technology involving a virtual negotiator approach coming into the market now. It works like this: The credit grantor or agency contacts the consumer by letter, email, or text reminding them of their debt and offering them a link to visit a website to negotiate their debt without a human being involved. The consumer logs onto the site, negotiates with the site and hopefully comes to terms with what is an acceptable payment plan and amount. In advance, the site would have been fed the terms by which the virtual negotiator would have been allowed to use. Finally, the consumer provides his payment information, receives back a recap of what he has agreed to and the process is complete. This is the future of collections, especially when you consider the younger generations rarely wanting to talk on the phone. They want to handle the majority of their matters digitally, on their own terms and at their own preferred times. The collections process can obviously be uncomfortable, but the thought is the virtual negotiator approach will make it less burdensome and more consumer-friendly. Learn more about virtual negotiation.

Knowing where e-commerce fraud takes place matters We recently hosted a Webinar with Mike Gross, Risk Strategy Director at Experian and Julie Conroy, Research Director at Aite Research Group, looking at the current state of card-not-present fraud, and what to prepare for in the coming year. Our biannual analysis of fraud attacks, served as a backdrop for the trends we’ve been seeing. I wanted to share some observations from the Webinar. Of course, if you prefer to hear it firsthand, you can download the archive recording here. I’ll start with the current landscape of card-not-present fraud. Julie shared 5 key trends her firm has identified regarding e-commerce fraud: Rising account take-over fraud Loyalty points targeted Increasingly global transactions Frustrating false declines Increasingly mobile consumers One particularly interesting note that Julie made was regarding consumer frustration levels towards forgotten passwords. While consumers are more frustrated when they’re locked out of access to their banking accounts (makes sense, it’s their money), forgotten passwords are more detrimental to e-commerce retailers since consumers are likely to go to another site. This equates to a frustrated consumer, and lost revenue for the business. Next, Mike went through the findings from our 2016 e-commerce fraud attack analysis. Fraud attack rates show the attempted fraudulent e-commerce transactions against the population of overall e-commerce orders. Overall, e-commerce attack rates spiked 33% in 2016. The biggest trends we saw included: Increased EMV adoption is driving a shift from counterfeit to card-not-present fraud 2B breached records disclosed in 2016, more than 3x any previous year Consumers reporting credit card fraud jumped from 15% in 2015 to over 32% in 2016 Attackers shifting locations slightly and international orders rely on freight forwarders 10 states saw an increase of over 100% in fraudulent orders Over 70 of the top 100 riskiest postal codes were not in last year’s list So, what will 2017 bring? Be prepared for more attacks, more global rings, more losses for businesses, and the emergence of IoT fraud. Businesses need to anticipate an increase of fraud over time and to be prepared. The value of employing a multi-layered approach to fraud prevention especially when it comes to authenticating consumers to validate transactions cannot be understated. By looking at all the points of the customer journey, businesses can better protect themselves from fraud, while maintaining a good consumer experience. Most importantly, having the right fraud solution in place can help businesses prevent losses both in dollars and reputation.