Customer Targeting & Segmentation

Artificial intelligence is here to stay, and businesses who are adopting the newest AI technology are ahead of the game. From targeting the right prospects to designing effective collections efforts, AI-driven strategies across the entire customer lifecycle are no longer a nice to have - they are a must. Many organizations are late to the game of AI and/or are spending too much time and money designing and redesigning models and deploying them over weeks and months. By the time these models are deployed, markets may have already shifted again, forcing strategy teams to go back to the drawing board. And if these models and strategies are not being continuously monitored, they can become less effective over time and lead to missed opportunities and lost revenue. By implementing artificial intelligence in predictive modeling and strategy optimization, financial institutions and lenders can design and deploy their decisioning strategies faster than ever before and make incremental changes on the fly to adapt to evolving market trends. While most organizations say they want to incorporate artificial intelligence and machine learning into their business strategy, many do not know where to start. Targeting, portfolio management, and collections are some of the top use cases for AI/ML strategy initiatives. Targeting One way businesses are using AI-driven modeling is for targeting the audiences that will most likely meet their credit criteria and respond to their offers. Financial institutions need to have the right data to inform a decisioning strategy that recognizes credit criteria, can respond immediately when prospects meet that criteria and can be adjusted quickly when those factors change. AI-driven response models and optimized decision strategies perform these functions seamlessly, giving businesses the advantage of targeting the right prospects at the right time. Credit portfolio management Risk models optimized with artificial intelligence and machine learning, built on comprehensive data sets, are being used by credit lenders to acquire new revenue and set appropriate balance limits. Strategies built around AI-driven risk models enable businesses to send new offers and cross-sell offers to current customers, while appropriately setting initial credit limits and managing limits over time for increased wallet share and reduced risk. Collections AI- and ML-driven analytics models are also optimizing collections strategies to improve recovery rates. Employing AI-powered balance and response models, credit lenders can make smarter collections decisions based on the most predictive and accurate information available. For lending businesses who are already tight on resources, or those whose IT teams cannot meet the demand of quickly adapting to ever-changing market conditions and decisioning criteria, a managed service for AI-powered models and strategy design might be the best option. Managed service teams work closely with businesses to determine specific use cases, develop models to meet those use cases, deploy models quickly, and monitor models to ensure they keep producing and predicting optimally. Experian offers Ascend Intelligence Services, the only managed service solution to provide data, analytics, strategy and performance monitoring. Experian’s data scientists provide expert guidance as they collaborate with businesses in developing and deploying models and strategies around targeting, acquisitions, limit-setting, and collections. Once those strategies are deployed, Experian continually monitors model health to ensure scores are still predictive and presents challenger models so credit lenders can always have the most accurate decisioning models for their business. Ascend Intelligence Services provides an online dashboard for easy visibility, documentation for regulatory compliance, and cloud capabilities to deliver scores and decisions in real-time. Experian’s Ascend Intelligence Services makes getting into the AI game easy. Start realizing the power of data and AI-driven analytics models by using our ROI calculator below: initIframe('611ea3adb1ab9f5149cf694e'); For more information about Ascend Intelligence Services, visit our webpage or join our upcoming webinar on October 21, 2021. Learn more Register for webinar

At some point a lender may need to issue an RFI or an RFP for a credit decisioning system. In this latest installment of “working with vendors” let’s dive into some best practices for writing RFIs and RFPs that will help you more quickly and efficiently understand the capabilities of a vendor. First, have one person (or at most a very small group) review the document before it goes out to vendors. Too often these kinds of documents seem like they’re just cut and pasted together without any concern if they paint a coherent picture. If it’s worth the time to write an RFI/RFP, then it’s worth the time to get it right so that the vendor responses make sense. If your document paints an inconsistent picture, a vendor may not know what products will best serve your requirements. In turn, precious time will be wasted in discussions around what’s being proposed. Here are some things to make clear in the document: For what part of the credit life cycle does this RFI/RFP apply (prospecting, origination, account management or collections)? If the request covers more than one part of the life cycle, make clear which questions apply to which part of the life cycle. Do you need a system that processes in batch or real-time requests (or both)? For example, a credit card account management solution can process accounts in batch (for proactive line management), in real time (for reactive requests) or possibly even both. Let the vendor know what it is you’re trying to do, as there may be different systems involved in processing these requests. Do you want this system hosted at the vendor, a third party (like AWS, Azure, etc.) or installed on premises? If you have a preference, let the vendor know. If you have no preference, ask the vendor what they can support. In general, consider playing down or skip detailed pricing questions. There’s nothing wrong with asking for a price range. For credit decisioning systems, detailed pricing is difficult for the vendor since there are often high levels of unknown customization to do. A better question might be, “What things will the vendor have to know in order to accurately price the solution? What are the logical next steps to get more accurate pricing? What’s the typical range of pricing in a solution such as this and what drives that range?” Will you be acting as an aggregator? Sometimes systems are created as front ends to several lenders. For example, a client may want to create a website where a borrower can “shop” among several lenders. This is certainly doable but carries with it a whole host of legal, compliance, business and technical questions. In my opinion, I’d skip the RFI/RFP in this situation and have a robust sit down directly with the vendors. This option will likely be far more productive. Ask more open-ended questions. “How does the solution perform task X?” as opposed to, “Do you support Y?” Often, there’s more than one way to accomplish a task. Asking more open-ended questions will yield a more comprehensive answer from the vendor rather than a simple yes or no response. It also gives you the opportunity to learn about the latest decisioning techniques. Be careful that you have not copied old RFP questions that are no longer relevant. I’ve had clients ask if we support Bernoulli Boxes (a mid-80s kind of floppy disk), or whether we support OS/2, etc. I’ve even had questions about supporting a particular printer. These kinds of questions are centered on the support of the operating system and not a particular vendor’s credit decisioning software. Instead of asking yes/no technology questions, ask for a typical sample architecture. Ask what kinds of APIs are supported (REST, SOAP/XML, etc.). Ask about the solution’s capabilities to call third-party systems (both internal and external). Ask fewer, but more in-depth questions. If the solution needs screens, be clear which screens you’re talking about. Do you need screens to make rule adjustments or configuration changes? Do you need screens for manual review or some sort of case management? Do you need consumer-facing screens where borrowers can type in their application data? If you need screens, be clear on the task the screens should perform. If you have particular concerns, ask them in an open-ended way. For example, “The solution will have to exchange file-based data with a mainframe. How can your solution best satisfy this requirement?” In general, state your requirement not the technology to use. A preamble or brief executive summary is useful to get the big picture across before the vendor delves into any questions. A paragraph or two can go a long way to help the vendor better assess your requirements and provide more meaningful answers to you. This works well because it’s easier to give the big picture in a few paragraphs as opposed to sprinkled around in multiple questions. To summarize, be clear on your requirements and provide a more open-ended format for the vendor to respond. This will save both you and the vendor a lot of time. In section three, I’ll cover evaluating vendors.

Perhaps your loan origination system (LOS) doesn’t have the flexibility that you require. Perhaps the rules editor can’t segment variables in the manner that you need. Perhaps your account management system can’t leverage the right data to make decisions. Or perhaps your existing system is getting sunset. These are just some of the many reasons a company may want to investigate the marketplace for new credit decisioning software. But RFIs and RFPs aren’t the only way to find new decisioning software. After working in credit services decisioning for over 20 years — and seeing hundreds of RFPs and presenting thousands of solutions and proposed architectures — I’ve formed a few opinions about how I would go about things if I were in the customer’s seat and have broken that into a three-part series. Part 1 will cover everything up to issuing an RFI or RFP. Part 2 will discuss writing an RFP or RFI. Part 3 will cover evaluating vendors. Let’s go. If you’re looking to buy new decisioning software, your first inclination might be to issue an RFI or an RFP. However, that may not be the best idea. Here’s an issue that I frequently see. Vendors are constantly evolving their products. How a product did feature X two years ago might be completely different now. The terminology that the industry uses might have changed, and new capabilities (like machine learning) might have come about and changed whole sets of functionalities. The first decision point is to ask yourself a question, “Do I know exactly what I want or am I trying to generally learn what is out there?” An RFI or RFP isn’t always the greatest way to exchange information about a product. From a vendor’s standpoint, a feature-rich, complex system has to be reduced down to a few text answers or (worst yet) a series of yes or no answers. It all boils down to nuance. On many occasions, I’ve faced a dilemma when answering an RFP question, “This question is unclear; if the customer means X, the answer is yes; if they mean Y, the answer is no.” If I were in a room with the customer, I could ask them the question, they could provide clarification and I could then provide the accurate answer. There would be more opportunity to have a back and forth, “Oh when you said X, this is what you meant ….” All of that back and forth is lost with an RFI or RFP, or at least delayed until the (hopefully selected) vendor gets a chance to present in front of a live audience. Also, consider that vendors are eager to educate you about their product. They know exactly how the product works and they’re happy to answer your questions. It’s perfectly reasonable to go to a vendor with prewritten questions and thoughts and to pose those questions during a call or demonstration with the vendor. Nothing would prevent a customer from using the same questions for each vendor and evaluating them based on their answers. All of this can be done without issuing an RFI or RFP. In conclusion, I’d offer the following points to think about before issuing an RFI or RFP: A customer can provide questions that they want answered during a demonstration of a credit decisioning product. These same questions can be used to provide an initial assessment of several vendors. A customer’s understanding of a vendor’s capabilities is likely 10x faster and deeper with an interactive session versus reading the answers in a questionnaire. Nuanced and follow-up questions can be asked to gather a complete understanding. Alternative solutions can be explored. This exercise doesn’t have to replace an RFP but instead can better inform the customer about the questions they need answered in order to issue an RFP. Don’t be afraid to talk to a vendor, even if you’re not sure what you want in a new product. In fact, talk to several vendors. More than likely, you’ll learn a lot more via a discussion than you will via an RFI questionnaire. What’s good about an RFI or RFP is coming in with prepared questions. That way, you can judge each vendor using the same criteria but, if possible, get the answers to those questions via an interactive session with the vendors. Next: How to write an effective RFP or RFI.

When I worked as a junior analyst for one of the largest credit card issuers in the United States, the chief credit risk officer required the development of a “light switch report” and strongly encouraged everyone in her organization to read the report every day. She called it the light switch report because every morning when she walks into her office and the lights switch on, she would read the report and understand what’s going on with the business. I took her advice and developed the habit of reading the light switch report every morning — for more than a decade while I was with the organization. I knew the volume of applications, the approval rate and the average line of credit of approvals. I developed an informed idea of how delinquency rates would look six months into the future based on the average credit score of approvals today. Her advice was valuable, and the discipline she shared helped me develop my skill sets as a junior analyst, a people manager and head of a retail business line. Performance reports are foundational and are one of the key elements of a sound and prudent risk management framework. Regulators require effective monitoring reports and provide guidance on report generation as part of its examination process. (Office of the Comptroller of the Currency. Comptroller’s Handbook, Retail Lending Safety and Soundness. April 2017. Page 15.) While supporting lender clients on strategy designs and development, I have an opportunity to review various performance reports. I’d like to take this time to reiterate some of the basic components of a good performance report. Knowledge of audience is primary. Good performance reports are tailored for specific audiences who can make decisions that will affect specific outcomes. Performance reports for day-to-day monitoring would be different from reports designed for executive leadership. Transparency and accuracy are required and when reports are designed in support of areas of responsibility, those reports become meaningful and transformative. Relevant metrics matter. Once you identify the report’s audience, the metrics you choose to appear in the report become the next important exercise. Metrics should be relevant and consistent with the audience who’s expected, upon reviewing the report, to make statements such as the business is doing well and stable, or corrective action is needed. For example, a report on the predictive power of credit risk scores intended for model developers will likely contain metrics such Kolmogorov-Smirnov (KS), Gini index or worst scoring capture rate. Such reports won’t include the average handling time of an application, which will be more appropriate for an operations team. Metrics become even more powerful for decision-makers when calculated at a segment level. I’m a big fan of vintage reports. They tell the story of current lending practices (e.g., approval rates, average loan amount, average booked credit risk score), and more significantly they often foretell future performance (e.g., delinquency rates, charge-off rates). These foresights allow analysts and managers to plan and develop strategies today to manage the future state. If approve or decline decisions use a dual score matrix, generate a report showing the volume of applications on the dual score matrix. It’s quicker to spot unusual distributions compared to expectations when data is presented at this sublevel. The benefit is swifter modification or new actions when needed. If statistical designs are utilized, such as test or control segments and champion or challenger segments, metrics calculated at these levels become insightful. They allow validation of a randomized process and support statistical analysis and statements. Timeliness of reports is critical. Some reports for operational or technology purposes require constant and continuous reporting. Daily reports are important especially when new strategies are implemented. Sometimes daily reports are far more relevant within the first two or three weeks of a new strategy implementation. When daily reports show stabilization and alignment to expectations, switching to weekly or monthly reports is acceptable. Most retail products are designed for review on a cycle or monthly basis. Monthly and quarterly reports are milestones and provide good health checks of the business. Don’t forget formats. If a picture is worth a thousand words, then use charts and graphs to display data and capture audience attention. We’re all used to seeing data presented in tables, but there are far more applications today that allow us to read reports with compelling graphics, trendlines and patterns that grab our curiosity and draw us into the story. I like narratives even if they appear as headlines on a report. Succinct comments show discipline and convey understanding of a report’s contents. Effective performance reports evolve as the business changes. Audience, metrics and segments will change, but the basic components provide general guidelines on developing consistent and relevant reports.

The ongoing COVID-19 crisis and the associated rise in online transactions have made it more important than ever to keep customer information accurate and company databases up to date. By ensuring your organization’s data quality, you can allocate resources more effectively, minimize costs and safely serve your customers. As part of our recently launched Q&A perspective series, Suzanne Pomposello, Experian’s Strategic Account Director for CEM vertical markets, and William Palmer, Senior Sales Engineer, provided insight on how utility providers can manage and maintain accurate client data during system migrations and modernizations, achieve a single customer view and implement an operational data quality program. Check out what they had to say: Q: What are the best practices for effective data quality management that utility providers should follow? SP: To ensure data quality, we advise starting with a detailed understanding of the data your organization is currently maintaining and how new data entering your systems is being utilized. Conducting a baseline assessment and being able to properly validate the accuracy of your data is key to identifying areas that require cleansing and enrichment. Once you know what improvements and corrections need to be made, you can establish a strategy that will empower your organization to unlock the full potential of your data. Q: How does Experian help clients improve their data hygiene? SP: Experian has over 30 years of expertise in data cleansing, which is tapped to help clients deploy tactics and strategies to ensure an acceptable level of data integrity. First, we obtain a complete picture of each organizations objectives and challenges. We then assess the quality of their data and identify sources that require remediation. Armed with insight, we work alongside organizations to develop a phased action plan to standardize and enhance their data. Our data management solutions satisfy a wide range of needs and can be consumed in real-time, bulk and batch form. Q: Are there any protection regulations to be aware of when obtaining updated data? WP: Unlike Experian’s regulated divisions, most Experian Data Quality data elements are not burdened by complex regulations and restrictions. Our focus is on organizations’ main customer data points (e.g., address, email address and phone). We reference this data against unregulated source systems to validate, append and complete customer profiles. Experian’s data quality management tools can serve as a foundation for many regulatory, compliance and governance requirements, including, Metro 2 reporting, TCPA and CCPA. Q: Are demos of Experian’s data management solutions available? If so, where can they be accessed? WP: Yes, you can visit our website to view product functionality clips and recorded demonstrations. Additionally, we welcome the opportunity to explore our comprehensive data quality management tools via tests and live demonstrations using actual client data to gain a better understanding of how our solutions can be used to improve operational efficiency and the customer experience. For more insight on how to cleanse, standardize, and enhance your data to make sure you get the most out of your information, watch our Experian Symposium Series event on-demand. Watch now Learn more About Our Experts: Suzanne Pomposello, Strategic Account Director, Experian Data Quality, North America Suzanne manages the energy vertical for Experian’s Data Quality division, supporting North America. She brings innovative solutions to her clients by leveraging technology to deliver accurate and validated contact data that is fit for purpose. William Palmer, Senior Sales Engineer, Experian Data Quality, North America William is a Senior Sales Engineer for Experian’s Data Quality division, supporting North America. As an expert in the data quality space, he advises utility clients on strategies for immediate and long-term data hygiene practices, migrations and reporting accuracy.

With 2020 firmly behind us and multiple COVID-19 vaccines being dispersed across the globe, many of us are entering 2021 with a bit of, dare we say it, optimism. But with consumer spending and consumer confidence dipping at the end of the year, along with an inversely proportional spike in coronavirus cases, it’s apparent there’s still some uncertainty to come. This leaves businesses and consumers alike, along with fintechs and their peer financial institutions, wondering when the world’s largest economy will truly rebound. But based on the most recent numbers available from Experian, fintechs have many reasons to be bullish. In this unprecedented year, marked by a global pandemic and a number of economic and personal challenges for both businesses and consumers, Americans are maintaining healthy credit profiles and responsible spending habits. While growth expectedly slowed towards the end of the year, Q4 of 2020 saw solid job gains in the US labor market, with 883,000 jobs added through November and the US unemployment rate falling to 6.7%. Promisingly, one of the sectors hit hardest by the pandemic, the leisure and hospitality industry added back the most jobs of all sectors in October: 271,000. Additionally, US home sales hit a 14-year high fueled by record low mortgage rates. And finally, consumer sentiment rose to the highest level (81.4%) since March 2020. Not only are these promising signs of continued recovery, they illustrate there are ample market opportunities now for fintechs and other financial institutions. “It’s been encouraging to see many of our fintech partners getting back to their pre-COVID marketing levels,” said Experian Account Executive for Fintech Neil Conway. “Perhaps more promising, these fintechs are telling me that not only are response rates up but so is the credit quality of those applicants,” he said. More plainly, if your company isn’t in the market now, you’re missing out. Here are the four steps fintechs should take to reenter the lending marketing intelligently, while mitigating as much risk as possible. Re-do Your Portfolio Review Periodic portfolio reviews are standard practice for financial institutions. But the health crisis has posted unique challenges that necessitate increased focus on the health and performance of your credit portfolio. If you haven’t done so already, doing an analysis of your current lending portfolio is imperative to ensure you are minimizing risk and maximizing profitability. It’s important to understand if your portfolio is overexposed to customers in a particularly hard-hit industry, i.e. entertainment, or bars and restaurants. At the account level there may be opportunities to reevaluate customers based on a different risk appetite or credit criteria and a portfolio review will help identify which of your customers could benefit from second chance opportunities they may not have otherwise been able to receive. Retool Your Data, Analytics and Models As the pandemic has raged on, fintechs have realized many of the traditional data inputs that informed credit models and underwriting may not be giving the complete picture of a consumer. Essentially, a 720 in June 2020 may not mean the same as it does today and forbearance periods have made payment history and delinquency less predictive of future ability to pay. To stay competitive, fintechs must make sure they have access to the freshest, most predictive data. This means adding alternative data and attributes to your data-driven decisioning strategies as much as possible. Alternative data, like income and employment data, works to enhance your ability to see a consumer’s entire credit portfolio, which gives lenders the confidence to continue to lend – as well as the ability to track and monitor a consumer’s historical performance (which is a good indicator of whether or not a consumer has both the intention and ability to repay a loan). Re-Model Your Lending Criteria One of the many things the global health crisis has affirmed is the ongoing need for the freshest, most predictable data inputs. But even with the right data, analytics can still be tedious, prolonging deployment when time is of the essence. Traditional models are too slow to develop and deploy, and they underperform during sudden economic upheavals. To stay ahead in times recovery or growth, fintechs need high-quality analytics models, running on large and varied data sets that they can deploy quickly and decisively. Unlike many banks and traditional financial institutions, fintechs are positioned to nimbly take advantage of market opportunities. Once your models are performing well, they should be deployed into the market to actualize on credit-worthy current and future borrowers. Advertising/Prescreening for Intentional Acquisition As fintechs look to re-enter the market or ramp up their prescreen volumes to pre-COVID levels, it’s imperative to reach the right prospects, with the right offer, based on where and how they’re browsing. More consumers than ever are relying on their phones for browsing and mobile banking, but aligning messaging and offers across devices and platforms is still important. Here’s where data-driven advertising becomes imperative to create a more relevant experience for consumers, while protecting privacy. As 2021 rolls forward, there will be ample chance for fintechs to capitalize on new market opportunities. Through up-to-date analysis of your portfolio, ensuring you have the freshest, predictive data, adjusting your lending criteria and tweaking your approach to advertising and prescreen, you can be ready for the opportunities brought on by the economic recovery. How is your fintech gearing up to re-enter the market? Learn more

Despite the constant narrative around “unprecedented times” and the “new normal,” if the current market volatility tells us anything, it’s to go back to basics. As financial institutions navigate COVID-19’s economic impact, and challenges that are likely to be different or more extreme than in the past, the best credit portfolio management practices are fundamental. The global pandemic impacts today’s data as existing data and analytics may not accurately reflect what is happening now, resulting in inaccurate portfolio assessment. In order to successfully navigate loss forecasting, predicting borrower behavior and controlling loss ratios, lenders must engage new data, analytics and economic scenarios suited for today’s changing times. In Experian’s latest white paper, “Credit Portfolio Management After the COVID-19 Recession,” we’ll explore best practices to combat the following challenges: Forecasting credit losses despite increased economic volatility Businesses have long used a variety of data, analytics and models to anticipate and project the future direction of their organization based on a number of data points; however, with the onset of the global pandemic, long-standing scenarios became suddenly irrelevant. Predicting borrower behavior given increased financial disparities The post-pandemic and pre-pandemic worlds are very different places for some borrowers. Pandemic-related job losses and other economic effects will not be spread evenly and this variability may be reflected in lenders’ portfolios. Controlling loss ratios In the post-COVID world, it will be mission critical for lenders to use high-quality and up-to-date data to balance priorities and identify which areas of their portfolio need attention now. Whether your portfolio is doing better than expected, as expected, or worse than expected, now is the time to refresh portfolio management strategy. Lenders should be watching for early indicators in loan portfolios to better navigate a fluctuating economy and that requires new resources and better tools. Take control of your business’ trajectory. Download now

No one can deny that the mortgage and real estate industries have been uniquely affected by COVID-19. Social distancing mandates have hindered open house formats and schedules. Meanwhile, historically low-interest rates, pent-up demand and low housing inventory created a frenzied sellers’ market with multiple offers, usually over-asking. Added to this are the increased scrutiny of how much borrowers will qualify and get approved for with tightened investor guidelines, and the need to verify continued employment to ensure a buyer maintains qualifying status through closing. As someone who’s spent more than 15 years in the industry and worked on all sides of the transaction (as a realtor and for direct lenders), I’ve lived through the efforts to revamp and digitize the process. However, it wasn’t until recently that I purchased my first home and experienced the mortgage process as a consumer. And it was clear that, for most lenders, the pandemic has only served to shine a light on a still somewhat fragmented mortgage process and clunky consumer experience. Here are three key components missing from a truly modernized mortgage experience: Operational efficiency Knowing that the industry had made moves toward a digital mortgage process, I hoped for a more streamlined and seamless flow of documents, loan deliverables and communication with the lender. However, the process I experienced was more manual than expected and disjointed at times. Looking at a purchase transaction from end to end, there are at least nine parties involved: buyer, seller, realtors, lender, home inspectors/inspection vendors, appraiser, escrow company and notary. With all those touchpoints in play, it takes a concerted effort between all parties and no unforeseen issues for a loan to be originated faster than 30 days. Meanwhile, the opposite has been happening, with the average time to close a loan increasing to 49 days since the beginning of the pandemic, per Ellie Mae’s Origination Insights Report. Faster access to fresher data can reduce the time to originate a mortgage. This saves resource hours for the lender, which equates to savings that can ultimately be passed down to the borrower. Digital adoption There are parts of the mortgage process that have been digitized, yes. However, the mortgage process still has points void of digital connectivity for it to truly be called an end-to-end digital process. The borrower is still required to track down various documents from different sources and the paperwork process still feels very “manual.” Printing, signing and scanning documents back to the lender to underwrite the loan add to the manual nature of the process. Unless the borrower always has all documents digitally organized, requirements like obtaining your W-2’s and paystubs, and continuously providing bank and brokerage statements to the lender, make for an awkward process. Modernizing the mortgage end-to-end with the right kind of data and technology reduces the number of manual processes and translates into lower costs to produce a mortgage. Turn times are being pushed out when the opposite could be happening. A streamlined, modernized approach between the lender and consumer not only saves time and money for both parties, it ultimately enables the lender to add value by providing a better consumer experience. Transparency Digital adoption and better digital end-to-end process are not the only keys to a better consumer experience; transparency is another integral part of modernizing the mortgage process. More transparency for the borrower starts with a true understanding of the amount for which one can qualify. This means when the loan is in underwriting, there needs to be a better understanding of the loan status and the ability to better anticipate and be proactive about loan conditions. Additionally, the lender can profit from gaining more transparency and visibility into a borrower’s income streams and assets for a more efficient and holistic picture of their ability to pay upfront. This allows for a more streamlined process and enables the lender to close efficiently without sacrificing quality underwriting. A multitude of factors have come into play since the beginning of the pandemic – social distancing mandates have led to breakdowns in a traditionally face-to-face process of obtaining a mortgage, highlighting areas for improvement. Can it be done faster, more seamlessly? Absolutely. In ideal situations, mortgage originators can consistently close in 30 days or less. Creating operational efficiencies through faster, fresher data can be the key for a lender to more accurately assess a borrower’s ability to pay upfront. At the same time, a digital-first approach enhances the consumer experience so they can have a frictionless, transparent mortgage process. With technology, better data, and the right kind of innovation, there can be a truly end-to-end digital process and a more informed consumer. Learn more

As industry experts are still unsure when the economy will fully recover, re-entry into marketing preapproved credit offers seems like a far-off proposal. However, several of the top credit card issuers are already mailing prescreen offers, with many other lenders following suit. When the time comes for organizations to resume, or even expand this type of targeting, odds are that the marketing budget will be tighter than in the past. To make the most of the limited available marketing spend, lenders will need to be more prescriptive with their selection process to increase response rates on fewer delivered offers. Choosing the best candidates to receive these offers, from a credit risk perspective, will be critical. With delinquencies being suppressed due to CARES Act reporting guidelines, identifying consumers with the ability to repay will require additional assessment of recent credit behavior metrics, such as actual payment amounts and balance migration. Along with the presence of explicit indicators of accommodated trades (trades affected by natural disaster, trades with a balance but no scheduled payment amount) on a prospect’s credit file, their recent trends in payments and balance shifts can be integral in determining whether a prospect has been adversely impacted by today’s economic environment. Once risk criteria have been developed using a mix of bureau scores (like the VantageScore® credit score), traditional credit attributes and trended attributes measuring recent activity, additional targeting will be critical for selecting a population that’s most likely to open the relevant trade type. For credit cards and personal installment loans, response performance can be greatly improved by aligning product offers with prospects based on their propensity to revolve, pay in full each month or consolidate balances. Additionally, the process to select final prospects should integrate a propensity to open/respond assessment for the specific offering. While many lenders have custom models developed on previous internal response performance, off-the-shelf propensity to open models are also available to provide an assessment of a prospect’s likelihood to open a particular type of trade in the coming months. These models can act as a fast-start for lenders that intend to develop internal custom models, but don’t have the response performance within a particular product/geography/risk profile. They are also commonly used as a long-term solution for lenders without an internal model development team or budget for an outsourced model. Prescreen selection best practices Identify geography and traditional credit risk assessment of the prospect universe. Overlay attributes measuring accommodated trades and recent payment/balance trends to identify prospects with indications of ability to pay. Segment the prospect universe by recent credit usage to determine products that would resonate. Make final selections using propensity to open model scores to increase response rates by only making offers to consumers who are likely looking for new credit offers. While the best practices listed above don’t represent a risk-free approach in these uncertain times, they do provide a framework for identifying prospects with mitigated repayment risk and insights into the appropriate credit offer to make and when to make it. Learn about in the market models Learn about trended attributes VantageScore® is a registered trademark of VantageScore Solutions, LLC.

Achieving collection results within the subprime population was challenging enough before the current COVID-19 pandemic and will likely become more difficult now that the protections of the Coronavirus Aid, Relief, and Economic Security (CARES) Act have expired. To improve results within the subprime space, lenders need to have a well-established pre-delinquent contact optimization approach. While debt collection often elicits mixed feelings in consumers, it’s important to remember that lenders share the same goal of settling owed debts as quickly as possible, or better yet, avoiding collections altogether. The subprime lending population requires a distinct and nuanced approach. Often, this group includes consumers that are either new to credit as well as consumers that have fallen delinquent in the past suggesting more credit education, communication and support would be beneficial. Communication with subprime consumers should take place before their account is in arrears and be viewed as a “friendly reminder” rather than collection communication. This approach has several benefits, including: The communication is perceived as non-threatening, as it’s a simple notice of an upcoming payment. Subprime consumers often appreciate the reminder, as they have likely had difficulty qualifying for financing in the past and want to improve their credit score. It allows for confirmation of a consumer’s contact information (mainly their mobile number), so lenders can collect faster while reducing expenses and mitigating risk. When executed correctly, it would facilitate the resolution of any issues associated with the delivery of product or billing by offering a communication touchpoint. Additionally, touchpoints offer an opportunity to educate consumers on the importance of maintaining their credit. Customer segmentation is critical, as the way lenders approach the subprime population may not be perceived as positively with other borrowers. To enhance targeting efforts, lenders should leverage both internal and external attributes. Internal payment patterns can provide a more comprehensive view of how a customer manages their account. External bureau scores, like the VantageScore® credit score, and attribute sets that provide valuable insights into credit usage patterns, can significantly improve targeting. Additionally, the execution of the strategy in a test vs. control design, with progression to successive champion vs. challenger designs is critical to success and improved performance. Execution of the strategy should also be tested using various communication channels, including digital. From an efficiency standpoint, text and phone calls leveraging pre-recorded messages work well. If a consumer wishes to participate in settling their debt, they should be presented with self-service options. Another alternative is to leverage live operators, who can help with an uptick in collection activity. Testing different tranches of accounts based on segmentation criteria with the type of channel leveraged can significantly improve results, lower costs and increase customer retention. Learn About Trended Attributes Learn About Premier Attributes

In today’s uncertain economic environment, the question of how to reduce portfolio volatility while still meeting consumers’ needs is on every lender’s mind. With more than 100 million consumers already restricted by traditional scoring methods used today, lenders need to look beyond traditional credit information to make more informed decisions. By leveraging alternative credit data, you can continue to support your borrowers and expand your lending universe. In our most recent podcast, Experian’s Shawn Rife, Director of Risk Scoring and Alpa Lally, Vice President of Data Business, discuss how to enhance your portfolio analysis after an economic downturn, respond to the changing lending marketplace and drive greater access to credit for financially distressed consumers. Topics discussed, include: Making strategic, data-driven decisions across the credit lifecycle Better managing and responding to portfolio risk Predicting consumer behavior in times of extreme uncertainty Listen in on the discussion to learn more. Experian · Effective Lending in the Age of COVID-19

Do consumers pay certain types of credit accounts before others during financial distress? For instance, do they prioritize paying mortgage bills over credit card bills or personal loans? During the Great Recession, the traditional notion of payment priority among multiple credit accounts was upended, throwing strategies employed by financial institutions into disarray. Similarly, current circumstances in the context of COVID-19 might cause sudden shifts in prioritization of payments which might have a dramatic impact on your credit portfolio. Financial institutions would be better able to forecast and control exposure to credit risk, and to optimize servicing practices such as forbearance and collections treatments if they could understand changing customer payment behaviors and priorities of their existing customers across all open trades. Unfortunately, financial institutions’ data—including their own behavioral data and refreshed credit bureau data--are limited to information about their own portfolio. Experian data provides insight which complements the financial institutions’ data expanding understanding of consumer payment behavior and priorities spanning all trades. Experian recently completed a study aimed at providing financial institutions valuable insights about their customer portfolios prior to COVID-19 and during the initial months of COVID-19. Using the Experian Ascend Technology Platform™, our data scientists evaluated a random 10% sample of U.S. consumers from its national credit file. Data from multiple vintages were pulled (June 2006, June 2008 and February 2018) and the payment trends were studied over the subsequent performance period. Experian tabulated the counts of consumers who had various combinations of open and active trade types and selected several trade type combinations with volume to differentiate performance by trade type. The selected combinations collectively span a variety of scenarios involving six trade types (Auto Loans, Bankcard, Student Loan, Unsecured Personal Loans, Retail Cards and First Mortgages). The trade combinations selected accommodate a variety of lenders offering different products. For each of the consumer groups identified, Experian calculated default rates associated with each trade type across several performance periods. For brevity, this blog will focus on customers identified as of February 2018 and their subsequent performance through February 2020. As the recession evolves and when the economy eventually recovers, we will continue to monitor the impacts of COVID-19 on consumer payment behavior and priorities and share updates to this analysis. Consumers with Bankcard, Mortgage, Auto and Retail accounts Among consumers having open and recently active Bankcard, Mortgage, Auto and Retail accounts, bankcard delinquency was highest throughout the 24-month performance window, followed by Retail. Delinquency rates for Auto and Mortgage were the lowest. During the pre-COVID-19 period, consumers paid their secured loans before their unsecured loans. As demonstrated in the table below, customer payment priority was stable across the entire 24-month period, with no significant shift in payment priorities between trade types. Consumers with Unsecured Personal Loan, Retail Card and Bankcard accounts. Among consumers having open and recently active Unsecured Personal Loan, Retail Card and Bankcard accounts, consumers are likely to pay unsecured personal loans first when in financial distress. Retail is the second priority, followed by Bankcard. KEY FINDINGS From February 2018 through April 2020, relative payment priority by trade type has been stable Auto and Mortgage trades, when present, show very high payment priority Download the full Payment Hierarchy Report here. Download Now Learn more about how Experian can create a custom payment hierarchy for the customers in your own portfolio, contact your Experian Account Executive, or visit our website.

Consumer sentiment can help automotive marketers create a more human connection with consumers.

Experian recently released its Q1 2020 Market Trends report, which provides insights about the vehicles on the road and the most popular vehicle segments.

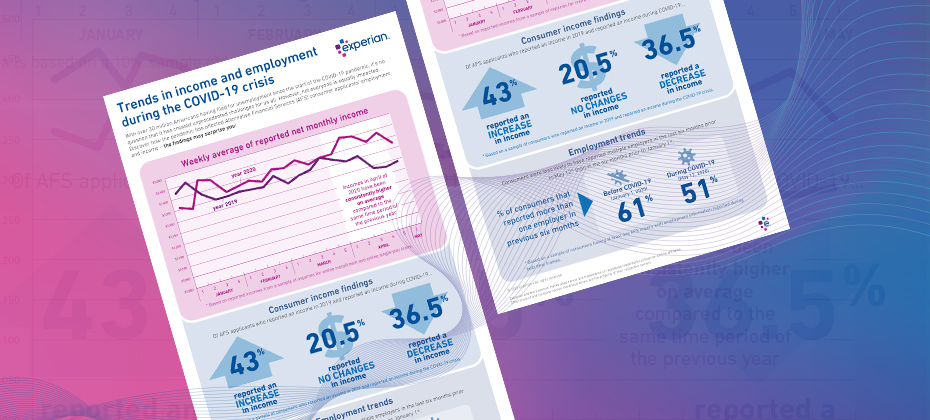

With many individuals finding themselves in increasingly vulnerable positions due to COVID-19, lenders must refine their policies based on their consumers’ current financial situations. Alternative Financial Services (AFS) data helps you gain a more comprehensive view of today's consumer. The COVID-19 pandemic has had far-reaching economic consequences, leading to drastic changes in consumers’ financial habits and behavior. When it comes to your consumers, are you seeing the full picture? See if you qualify for a complimentary hit rate analysis Download AFS Trends Report