Fintech

Fintech

Juniper Research recently recognized Experian as a Fraud Detection and Prevention Market Leader in its Online Payment Fraud Whitepaper. Juniper also shared important market insights in the report.

With so much data being generated by our social media obsession, should lenders consider social media insights to assess credit risk?

The collections space has been migrating from traditional mail and outbound calls to electronic payment portals, digital collections and virtual negotiators. Now that collectors have had time to test virtual collections, we’ve collected some data points. Here are a few:

Creating a customer journey map, and seeing it through from acquisitions to collections, can help you better define messaging and channels to best reach your audience.

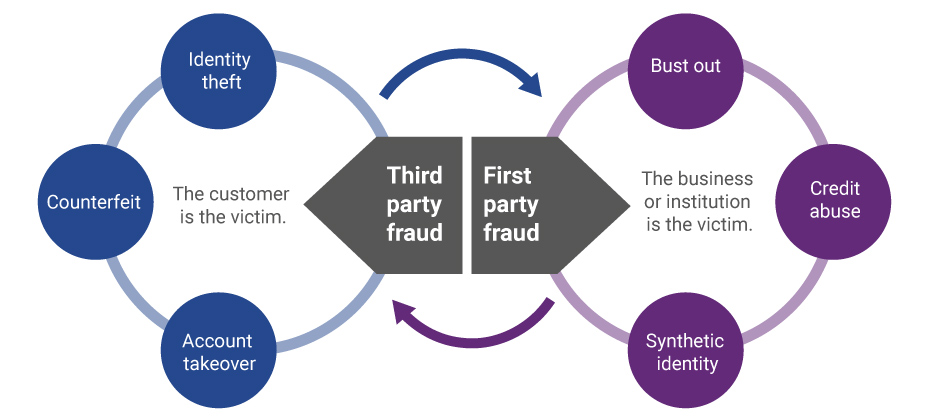

Third-party and first-party schemes are now interchangeable, and traditional fraud detection practices are less effective in fighting these evolving fraud types.

As more collectors transition from "dialing for dollars" to digital solutions, they are seeing early results and success with virtual negotiation tools.

APIs--Application Programming Interfaces--are the hidden backbone of our modern world which allow software programs to communicate with one another.

In Experian’s latest State of Student Lending report, we dive into how the $1.4 trillion in student loan debt for Americans is impacting all generations in regards to credit scores, debt load and delinquencies.

Many institutions take a “leap of faith” when it comes to developing prospecting strategies as it pertains to credit marketing. How can a data-driven approach help?

Student loan debt — outstanding debt grew 21 percent since 2013 to reach a high of $1.49 trillion in the fourth quarter of 2016.

The first wave of Gen Z are coming onto the credit file. Here is a first look at how they are behaving, and what this means for businesses and finance companies.

Synthetic identity fraud is an epidemic that does more than negatively affect portfolio performance. It can hurt your reputation as a trusted organization.

New CFPB study demonstrates the importance of moving forward with inclusion of new sources of high-quality financial data — like on-time payment data from rent, utility and telecommunications providers — into a consumer’s credit file.

Later this year, FICO will retire its Score V1, making it mandatory for those lenders still using the old software to find another solution.

There are about as many definitions for people-based marketing as there are companies using the term. Each company seems to skew the definition to fit their particular service offering. The distinctions are vast, and especially for financial services companies running regulated campaigns, they can be incredibly important. At Experian, we define people-based marketing in its purest form: targeting at the individual level across channels. This is a practice we’re very familiar with in offline marketing, having honed arguably one of the most accurate views of U.S. consumers over the past three decades. And now we’re taking those tried and true principals and applying them to digital channels. It’s not as easy as it sounds. The challenge with people-based marketing With direct mail, people-based marketing was easy. Jane Doe lives at 123 Main St. If I want to reach her, I can simply send her a direct mail piece at that address. To help, I can utilize any number of services, including the National Change of Address database, to know where to reach her if she ever moves. People-based marketing through digital channels is exponentially more difficult. While direct mail has one signal with which you use to identify a consumer (the address), digital channels offer countless signals. And not all of those signals can be used, either individually or in conjunction with other signals, to reliably tie a consumer to a persistent offline ID. A prime example of this is cookies. The problem with cookies A cookie, in and of itself, isn’t the problem. The problem is the linkage. How was a cookie associated with the person to whom the ad is being served? As marketers, we need to make sure that we are reaching the right people with the right ad … and more importantly not reaching those people who have opted out. This is especially true in the world of regulated data, where you need to know who you are targeting. And cookie-based linkage is controlled by a handful of companies, many of which are walled gardens who don’t share how they link offline people to online cookies and don’t collect this information directly. They rely on other third-party websites to gather PII, and connect it to their cookies. In some cases, the data is very accurate (especially with transaction data). In some cases, it is not (think websites that collect PII when giving surveys, offering coupons, etc.). In short, in order for you to use cookie-based targeting accurately, you need to have insight into the source of the base linkage data that was used to connect the offline consumer record to the online cookie. This same concept applies to all forms of digital linkage that drive people-based marketing. Why does people-based marketing matter in digital credit marketing? With campaigns that utilize non-regulated data, such as “Invitation to Apply” campaigns that are driven from demographic and psychographic data, the consequences of not reaching the consumer you meant to target are negligible. But with campaigns that utilize regulated data, you must ensure you’re targeting the exact consumer you meant to reach. More importantly, you must make sure you’re not targeting an ad to a consumer who had previously opted out of receiving offers driven with regulated data (prescreen offers, for example). Even if you’ve already delivered a direct mail piece with the same offer, this doesn’t negate your responsibility to reach only approved consumers who have not opted out. --- Bottom line, the world of 1:1 marketing is growing more sophisticated, and that’s a good thing. Marketers just need to understand that while regulated data can be powerful, they must also take great responsibility when handling it. The data exists to deliver firm offers of credit to your very specific target in all-new mediums. People-based marketing has its place, and it can now be done in a compliant, digitally-savvy way – in the financial services space, nonetheless. Register for our webinar on Credit Marketing Strategies to Drive Today's Digital Consumer.