Latest Posts

As new vehicle prices continue to rise, more consumers are turning to leasing as a cost-effective auto financing option.

Whether you’re a small business owner or a global corporation, the cost of being without cyber insurance after an incident can be extreme.

Whether its new regulations and enforcement actions from the Consumer Financial Protection Bureau or emerging legislation in Congress, the public policy environment for consumer and commercial credit is dynamic and increasingly complex. If you are interested to learn more about how to navigate an increasingly choppy regulatory environment, consider joining a breakout session at Experian’s Vision 2016 Conference that I will be moderating. I’ll be joined by several experts and practitioners, including: John Bottega, Enterprise Data Management Conor French, Funding Circle Troy Dennis, TD Bank Don Taylor, President, Automated Collection Services During our session, you’ll learn about some of the most trying regulatory issues confronting the consumer and commercial credit ecosystem. Most importantly, the session will look at how to turn potential challenges into opportunities. This includes learning how to incorporate new alternative data sets into credit scoring models while still ensuring compliance with existing fair lending laws. We’ll also take a deep dive into some of the coming changes to debt collection practices as a result of the CFPB’s highly anticipated rulemaking. Finally, the panel will take a close look at the challenges of online marketplace lenders and some of the mounting regulations facing small business lenders. Learn more about Vision 2016 and how to register for the May conference.

A recent Experian study reveals that tax filing, document collection and refund processing are done online more often, yet only 6% of consumers file taxes on a computer with up-to-date antivirus software. 79% filed their most recent tax return online, up from 73% in 2011 18% scan and save their tax documents electronically, up from 6% in 2011 More than 75% of respondents have used EFT for tax refunds As electronic filing continues to grow, identity theft is likely to increase. While consumers should take steps to protect themselves, businesses also need to employ identity theft protection solutions to safeguard consumer information. >> Identify and prevent fraud

Ensuring the quality of reported consumer credit data is a top priority for regulators, credit bureaus and consumers, and has increasingly become a frequent headline in press outlets when consumers find their data is not accurate. Think of any big financial milestone moment – securing a mortgage loan, auto loan, student loan, obtaining low-interest rate interest credit cards or even getting a job. These important transactions can all be derailed with an unfavorable and inaccurate credit report, causing consumers to hit social media, the press and regulatory entities to vent it out. Add in the laws and increased scrutiny from the Consumer Financial Protection Bureau (CFPB), and Federal Trade Commission (FTC) and it is clear data furnishers are seeking ways to manage their data in more effective ways. At Vision 2016, I am hosting a session, Achievements in data reporting accuracy – maximizing data quality across your organization, with several panel guests willing to share their journeys and learnings attached to the topic of data accuracy. Our diverse panel features leaders from varying industries: Jodi Cook, DriveTime Alissa Hess, USAA Bank Tom Danchik, Citi Julie Moroschan, Experian Each will speak to how they’ve overcome challenges to introduce a data quality program into their respective organizations, as well as best practices around assessing, monitoring and correcting credit reporting issues. One speaker will even touch on the challenging topic of securing funding for a data quality program, considering budgets are most often allocated to strategies, products and marketing directly tied to driving revenue. All lenders are advised to maintain a full 360-degree view of data reporting, from raw data submissions to the consumer credit profile. Better data input equals fewer inaccuracies, and an overarching data integrity program, can deliver a comprehensive view that satisfies regulators, improves the customer experience and provides better insight for internal decision making. To learn more about implementing a data quality plan for your organization, check out Vision 2016.

Device emulators are devices that pretend to be another. Innovative technology used for site testing for Web developers, attackers use to wreak havoc across industries

Below are some key strategies that will help financial institutions build and continue banking to millennials.

As automotive leasing trends to new heights, a rapid influx of off-lease vehicles are returning to market. Experian Automotive’s latest infographic explores the surge in off-lease vehicles, including which models and vehicle segments are most popular. Click here to download this infographic.

In today’s interconnected world, reaching consumers should be as simple as sending a text or calling their cell phone. However, complying with the Telephone Consumer Protection Act (TCPA) can create an almost insurmountable mountain. While the law has been in place since 1991, TCPA litigation continues to be a considerable source of potential legal and compliance risk for companies communicating with consumers. There were 1,908 TCPA lawsuits in 2014, an increase of 30 percent over the previous year, and a 231 percent increase in the last four years. Is your business facing challenges in complying with TCPA? Do you want to learn more about the changing and challenging TCPA legal and regulatory framework? Are you looking for best practices on how to win the battle of right party contact? Then you should join us for a breakout session solely focused on TCPA at Experian’s Vision 2016 Conference. The panel features a number of subject matter experts who will be able to provide attendees with a look at this law and some of the best practices to manage risk and ensure compliance. Panelists include: Mary Anne Gorman, Experian Tony Hadley, Experian Tom Gilbertson, Venable LLC To learn more more about TCPA best practices, check out Experian’s annual Vision Conference in May.

April is Financial Literacy Month, a special window of time dedicated to educating Americans about money management. But as stats and studies reveal, financial education is always needed.

Experian’s State of the Automotive Finance Market report shows the new auto loan amount financed in Q4 2015 was the highest on record since 2008.

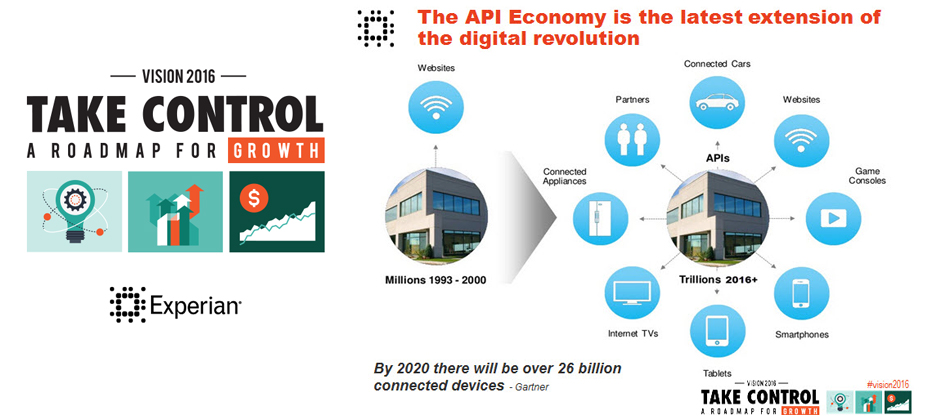

There is a revolution going on! We are in the midst of the second phase of the digital revolution and it is being fueled by API’s. API’s provide the access and mapping that allow access to and integration of the myriad of existing and new data sources available today. They do really helpful things like allow Uber to revolutionize the connection of riders to drivers as well as allow for quick, self-service credit decisions by integrating Experian data within Salesforce.com. Digital disruptors like Uber have scaled their business to massive size at breakneck speed because they can design, build and deploy solutions quickly. API’s and cloud computing play a central role in all of this. You will hear representatives from Uber share how API’s enabled the flow of Experian data through Salesforce.com enabling them to launch new business models, and enter new markets. Listen to Mike Myers as he shares a short overview of his Vision 2016 breakout session in this short video. Don’t miss this innovative Vision 2016 session! See you there.

Small business trade payment delinquencies can signal the beginning of business financial duress. However, sometimes these delinquencies are isolated events. Understanding the trade payment priorities of a business can lead to better business risk assessment. Experian understands commercial payment behaviors and can help clients more accurately interpret the risk of payment delinquencies for different kinds of trades. In his Vision 2016 breakout session “Which creditors get priority when businesses face a financial burden”, Sung Park, Analytics Consultant with Experian’s Decision Sciences discusses the types of trades or financial obligations that become delinquent first, and the conditions that most commonly signal overall business stress. What the audience will learn: The audience will have a better understanding of which type of trade delinquencies are likely isolated incidents and which ones are precursors of businesses facing a financial burden, and what actions can be taken proactively to mitigate risk. Don't miss your opportunity to catch these informative breakout sessions during Vision 2016.

According to a recent Experian study, women have higher credit scores and overall handle money, debt and financial decisions better than men.

Whether it is an online marketplace lender offering to refinance the student loan debt of a recent college graduate or an online small-business lender providing an entrepreneur with a loan when no one else will, there is no doubt innovation in the online lending sector is changing how Americans gain access to credit. This expanding market segment takes great pride in using “next-generation” underwriting and credit scoring risk models. In particular, many online lenders are incorporating noncredit information such as income, education history (i.e., type of degree and college), professional licenses and consumer-supplied information in an effort to strike the right balance between properly assessing credit risk and serving consumers typically shunned by traditional lenders because of a thin credit history. Regulatory concerns The exponential growth of the online lending sector has caught the attention of regulators — such as the U.S. Treasury Department, the Federal Deposit Insurance Corporation, Congress and the California Business Development Office — who are interested in learning more about how online marketplace lenders are assessing the credit risk of consumers and small businesses. At least one official, Antonio Weiss, a counselor to the Treasury secretary, has publicly raised concerns about the use of so-called nontraditional data in the underwriting process, particularly data gleaned from social media accounts. Weiss said that “just because a credit decision is made by an algorithm, doesn’t mean it is fair,” citing the need for lenders to be aware of compliance with fair lending obligations when integrating nontraditional credit data. Innovative and “tried and true” are not mutually exclusive Some have suggested the only way to assuage regulatory concerns and control risk is by using tried-and-true legacy credit risk models. The fact is, however, online marketplace lenders can — and should — continue to push the envelope on innovative underwriting and business models, so long as these models properly gauge credit risk and ensure compliance with fair lending rules. It’s not a simple either-or scenario. Lenders always must ensure their scoring analytics are based upon predictive and accurate data. That’s why lenders historically have relied on credit history, which is based upon data consumers can dispute using their rights under the Fair Credit Reporting Act. Statistically sound and validated scores protect consumers from discrimination and lenders from disparate impact claims under the Equal Credit Opportunity Act. The Office of the Comptroller of the Currency guidance on model risk management is an example of regulators’ focus on holding responsible the entities they oversee for the validation, testing and accuracy of their models. Marketplace lenders who want to push the limit can look to credit scoring models now being used in the marketplace without negatively impacting credit quality or raising fair lending risk. For example, VantageScore® allows for the scoring of 30 million to 35 million more people who currently are unscoreable under legacy credit score models. The VantageScore® credit score does this by using a broader, deeper set of credit file data and more advanced modeling techniques. This allows the VantageScore® credit score model to capture unique consumer behaviors more accurately. In conclusion, online marketplace lenders should continue innovating with their own “secret sauce” and custom decisioning systems that may include a mix of noncredit factors. But they also can stay ahead of the curve by relying on innovative “tried-and-true” credit score models like the VantageScore® credit score model. These models incorporate the best of both worlds by leaning on innovative scoring analytics that are more inclusive, while providing marketplace lenders with assurances the decisioning is both statistically sound and compliant with fair lending laws. VantageScore® is a registered trademark of VantageScore Solutions, LLC.