Tag: consumer attitudes

With the new year comes new goals, new accomplishments and new opportunities. And while new things are often associated with growth and success, nurturing what you already have should be just as important. The same goes for customer retention — although many financial institutions mainly focus on expanding their customer base, statistics show that a 5% increase in customer retention can lead to a company’s profits growing by 25% to 95% over time.1 What’s more, acquiring a new customer can cost five to seven times more than retaining an old one.2 What can your organization do to improve your customer retention efforts? Let’s first dive into recent consumer behavior trends. Consumer behaviors are changing High prices hit consumers, but service spending continues. Consumers are still seeing short-term price pressures. While spending on goods decreased by 0.9% in December, service spending remained flat. Consumers are starting to pull back. As economic uncertainty persists and excess savings from the pandemic dwindle further, consumers are saving more. Consumers aren’t completely satisfied when interacting with businesses digitally. 58% of consumers don’t feel that businesses completely meet their expectations for a digital online experience. With these trends in mind, how can your organization improve customer retention in 2023? Here are three tips to help you get started: Stay informed. Keeping up with your customers’ changing interests, behaviors, and life events enables you to identify cross-sell opportunities and create relevant credit marketing campaigns. With a large and comprehensive consumer database, like Experian’s ConsumerView®, you can better understand your customers, including the types of products they like to purchase and if they’re likely to buy a new or used vehicle in the next six months. To further enhance your customer retention efforts, you can also leverage Prospect TriggersSM, which allow you to stay alert whenever a customer is actively shopping for credit and extend preapproved credit offers to customers within hours or minutes, helping increase response rates. Be more than a business – be human. As consumers save more, financial institutions can build lifetime loyalty by serving as trusted financial partners and advisors. To do this, organizations can launch credit education programs and services that empower their customers to make smarter financial decisions. Helping consumers take control of their finances is especially important in today’s changing economy providing them with educational tools and resources, customers will learn how to strengthen their financial profiles while continuing to trust and lean on your organization for their credit needs. Think outside the mailbox. While direct mail is still an effective way to reach consumers, forward-thinking lenders are now meeting their customers online. To ensure you’re getting in front of your customers where they spend most of their time, consider leveraging digital channels, such as email or mobile applications when presenting and representing credit offers. This way, you can better connect with your customers and stay competitive. Importance of customer retention Rather than centering most of your growth initiatives around customer acquisition, your organization should focus on holding on to your most profitable customers, especially now with consumer behaviors changing and an abundance of credit options in the market. To learn more about how your organization can develop an effective customer retention strategy, explore our customer loyalty solutions. Improve customer retention today 1 Customer Retention Versus Customer Acquisition, Forbes, December 2022.

As more consumers apply for credit and increase their spending1, lenders and financial institutions have an opportunity to expand their portfolios and improve profitability. The challenge is ensuring they’re extending credit responsibly and inclusively. Millions of Americans, many of whom are creditworthy, lack access to mainstream credit options. This may be because they have limited or no credit history, negative information within their credit file, or are a part of a historically disadvantaged group. To say “yes” to consumers they otherwise couldn’t or wouldn’t lend to, lenders must gain a deeper understanding of an individual’s stability, ability and willingness to pay. That’s where expanded FCRA-regulated and trended data come in. While traditional credit data has long been the primary means of gauging creditworthiness, it doesn’t tell the full story of a consumer’s financial situation. Let’s explore how differentiated data can help lenders make more informed credit decisions. Using differentiated data for deeper lending Expanded FCRA-regulated data provides supplemental credit data to help lenders gain a more holistic view of their current and prospective customers. Some examples of expanded FCRA-regulated data include alternative financial services data from nontraditional lenders, consumer-permissioned account data, rental payments and full-file public records. Because this data drives greater visibility and transparency around inquiry and payment behaviors, lenders can more accurately determine a consumer’s ability to pay and distinguish between reliable and high-risk applicants. In turn, lenders can approve more creditworthy consumers, grow their portfolios and increase financial opportunities for underserved communities, all while preventing and mitigating risk. 89% of lenders agree that expanded FCRA-regulated data allows them to extend credit to more consumers. Trended data empowers lenders with predictive insights into consumers by providing key balance and payment data for the previous 24 months. This is important as lenders can determine if a consumer’s credit behavior has improved or deteriorated over time. In turn, lenders can: Identify creditworthy customers: Establish if a consumer has a demonstrated ability to pay, is consistently paying more than the minimum payment, or shows no signs of payment stress. Increase response rates: Match the right products with the right prospects. Determine upsell and cross-sell opportunities: Present relevant offers based on anticipated needs and behaviors. Limit loss exposure: Understand the direction and velocity of payment performance to effectively manage risk exposure. Trended data helps lenders better predict future behavior, manage portfolio risk and design the best marketing offers. Turning insights into action Together, trended and expanded FCRA-regulated data benefit lenders and consumers alike. With a more holistic view of their customers, lenders gain powerful insights to lend deeper, ultimately helping them to expand their portfolios and drive greater access to credit for underserved communities. Learn more 1 The Recovery of Credit Applications to Pre-Pandemic Levels, Consumer Financial Protection Bureau, 2021.

As lenders and consumers emerge from the pandemic, predicting the attributes of the “new normal” will be difficult. Consumer demand, credit characteristics and economic conditions have all been affected by the pandemic – changing the way we think about doing business. Regulators and legislators have also developed new priorities and expectations for financial institutions. Clint Ivester, Experian’s Solutions Consultant and VP of Sales, joined Lee Gilley and Jonathan Kkolodziej, Partners for Bradley, to share their observations from the past year at AFSA’s 2021 Independents Conference. They also discussed recommendations financial institutions should consider to achieve the best possible posture with respect to compliance and business readiness. Here are a few Q&A highlights: Q: How are stimulus packages and increased government spending affecting economic conditions? A: [Ivester]: Our Experian forecast shows that the economy will grow 6% in 2021. That is well above the 2.5% average we have seen over the last four decades and highest rate since 1983. While the economy is oriented toward growth, how strong that growth is going to be will really depend on how well things go when the “training wheels” are taken off, how robust the recovery is for lower-income workers, and how consumer spending habits have been altered by the pandemic. *Data sources include Bureau of Economic Analysis and Experian’s “COVID-19 Economics Scenarios” April 2021 Report Q: How should businesses be assessing future consumer demand, conditions, and broader economic conditions over the next few quarters? A: [Ivester]: To answer this question, we should consider some factors including unemployment. What happens with lower income workers will have a big impact on where consumer spending goes post-stimulus. While the overall economy is set for solid growth there are still 8 million people out of work with the vast majority being lower income workers. Employment for lower income workers is still down more than 20%. These workers are set to lose the most by the phase out of the federal pandemic unemployment programs and are the highest risk to lose all unemployment benefits. However, if we see a strong jobs recovery – as is very possible – in bars, restaurants, hotels and other industries, these individuals will return to more normal spending habits and consumer spending should remain robust. *Data source includes Opportunity Insights Economic Tracker Watch the full session to hear more about the discussion. For more resources and content on this topic, please visit our Look Ahead Resources page or contact us for more information.

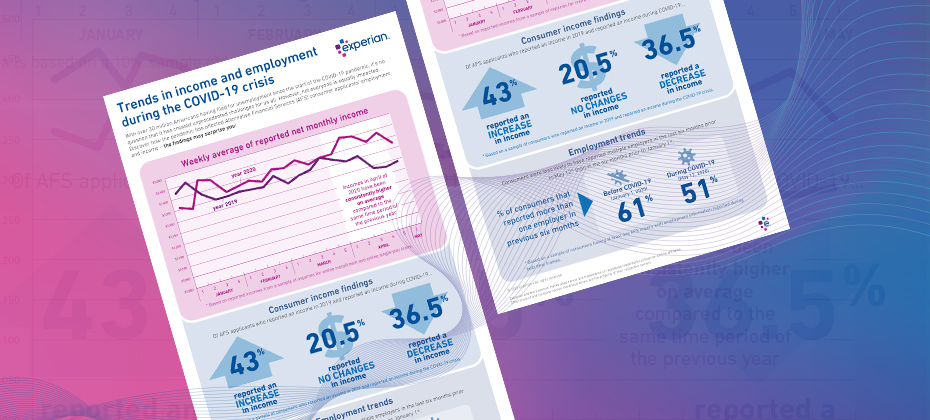

With many individuals finding themselves in increasingly vulnerable positions due to COVID-19, lenders must refine their policies based on their consumers’ current financial situations. Alternative Financial Services (AFS) data helps you gain a more comprehensive view of today's consumer. The COVID-19 pandemic has had far-reaching economic consequences, leading to drastic changes in consumers’ financial habits and behavior. When it comes to your consumers, are you seeing the full picture? See if you qualify for a complimentary hit rate analysis Download AFS Trends Report

It's been over 10 years since the start of the Great Recession. However, its widespread effects are still felt today. While the country has rebounded in many ways, its economic damage continues to influence consumers. Discover the Great Recession’s impact across generations: Americans of all ages have felt the effects of the Great Recession, making it imperative to begin recession proofing and better prepare for the next economic downturn. There are several steps your organization can take to become recession resistant and help your customers overcome personal financial difficulties. Are you ready should the next recession hit? Get started today

With the number of consumer visits to bank branches having declined from 52% of people visiting their bank branch on a monthly basis to 32% since 2015, the shift in banking to digital is apparent. Rather than face-to-face interaction, today’s financial consumers value remote, on-demand, services. They expect instant credit decisioning, immediate account funding, and around-the-clock customer assistance. To adapt, financial service providers see the necessity to respond to consumers’ growing expectations and become part of their overall digital lifestyle. Here are a few ways that financial services can adjust to changing consumer behavior: Drive mobile app activity With more than 50% of the world’s population actively using smartphones, the popularity of mobile banking apps has soared. Mobile apps have revolutionized the banking sector by facilitating easier communication between clients and institutions, offering value-added services, and introducing blockchain technologies. Consumers use mobile banking apps to pay bills, transfer funds, deposit checks, and make person-to-person payments. In fact, according to a study by Bank of America, more than 60% of millennials use mobile apps to make person-to-person payments on a regular basis! Financial institutions who launch new, or invest in enhancing existing mobile apps, can lower their overall costs, increase ROI, and maintain customer loyalty. Provide convenience and rewards CGI conducted a survey on emerging financial consumer trends, focusing on bank customers’ top requirements. Results confirmed that 81% of respondents expected to receive some form of an incentive from their primary banks. Today’s financial consumers may reasonably be won over by service offerings. They want rewards, limited fees, and convenience. As an example, Experian’s Text for CreditTM simplifies the credit process by providing customers with instant credit decisioning through their mobile devices. Personalized offers based on customer behavior can help enhance your brand and attract new customers. Stay connected Today’s consumers expect instant service and gratification. Consumers prefer to work with banks who offer accessible and responsive customer service. According to a recent NGDATA consumer banking survey, 41% of banking customers report that poor customer service is the primary reason they would leave their bank. Mintel suggests developing an omnichannel experience aligned with consumer media consumption. Stay connected with consumers through mobile apps, chatbots, social media, and email. Ensure that all interactions are relevant and helpful and immediately alert customers of any institutional issues or changes. The growing digital demands of consumers are influencing how people purchase banking, lending, and credit services. These changes are driving increased urgency for financial service institutions to adopt real-time financial processes that meet demands for convenience and speed. Interested in more best practices? Watch our On-Demand Webinar

Electric vehicles are here to stay – and will likely gain market share as costs reduce, travel ranges increase and charging infrastructure grows.