Credit Lending

It's the holiday season - you've been breached. Fraudsters and other criminals can make one of the busiest shopping times of the year, a miserable one.

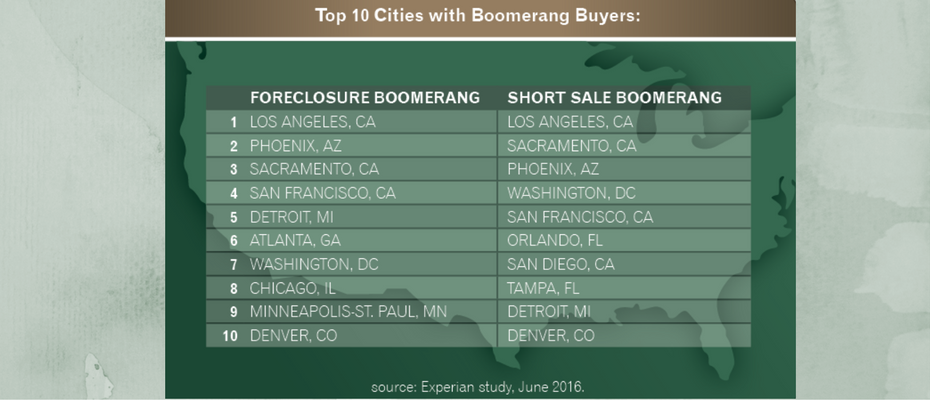

Which part of the country has bragging rights when it comes to sporting the best consumer credit scores? Drum roll please … Honors go to the Midwest. In fact, eight of the 10 cities with the highest consumer credit scores heralded from Minnesota and Wisconsin. Mankato, Minn., earned the highest ranking with an average credit score of 708 and Greenwood, Miss., placed last with an average credit score of 622. Even better news is that the nation’s average credit score is up four points; 669 to 673 from last year and is only six points away from the 2007 average of 679, which is a promising sign as the economy continues to rebound. Experian’s annual study ranks American cities by credit score and reveals which cities are the best and worst at managing their credit, along with a glimpse at how the nation and each generation is faring. “All credit indicators suggest consumers are not as ‘credit stressed’ — credit card balances and average debt are up while utilization rates remained consistent at 30 percent,” said Michele Raneri, vice president of analytics and new business development at Experian. As for the generational victors, the Silents have an average 730, Boomers come in with 700, Gen X with 655 and Gen Y with 634. We’re also starting to see Gen Z emerge for the first time in the credit ranks with an average score of 631. Couple this news with other favorable economic indicators and it appears the country is humming along in a positive direction. The stock market reached record highs post-election. Bankcard originations and balances continue to grow, dominated by the prime borrower. And the housing market is healthy with boomerang borrowers re-emerging. An estimated 2.5 million Americans will see a foreclosure fall of their credit report between June 2016 and June 2017, creating a new pool of potential buyers with improved credit profiles. More than 12 percent who foreclosed back in the Great Recession have already boomeranged to become homeowners again, while 29 percent who experienced a short sale during that same time have also recently taken on a mortgage. “We are seeing the positive effects of economic recovery with the rise in income and low unemployment reflected in how Americans are managing their credit,” said Raneri. Which means all is good in the world of credit. Of course there is always room for improvement, but this year’s 7th annual state of credit reveals there is much to be thankful for in 2016.

Experian Data Breach Resolution releases its fourth annual Data Breach Industry Forecast report with five key predictions on the 2017 data breach landscape

FinCEN and email-compromise fraud sheds additional light on the threats of Email Account Compromise and Business Email Compromise.

In order to compete for consumers and to enable lender growth, creating operational efficiencies such as automated decisioning is a must. Unfortunately, somewhere along the way, automated decisioning unfairly earned a reputation for being difficult to implement, expensive and time consuming. But don’t let that discourage you from experiencing its benefits. Let’s take a look at the most popular myths about auto decisioning. Myth #1: Our system isn’t coded. If your system is already calling out for Experian credit reporting data, a very simple change in the inquiry logic will allow your system to access Decisioning as a ServiceSM. Myth #2: We don’t have enough IT resources. Decisioning is typically hosted and embedded within an existing software that most credit unions currently use – thus eliminating or minimizing the need for IT. A good system will allow configuration changes at any time by a business administrator and should not require assistance from a host of IT staff, so the demand on IT resources should decrease. Decisioning as a Service solutions are designed to be user friendly to shorten the learning curve and implementation time. Myth #3: It’s too expensive. Sure, there are highly customized products out there that come with hefty price tags, but there are also automated solutions available that suit your budget. Configuring a product to meet your needs and leaving off any extra bells and whistles that aren’t useful to your organization will help you stick to your allotted budget. Myth #4: Low ROI. Oh contraire…Clients can realize significant return-on-investment with automated decisioning by booking more accounts … 10 percent increase or more in booked accounts is typical. Even more, clients typically realize a 10 percent reduction in bad debt and manual review costs, respectively. Simply estimating the value of each of these things can help populate an ROI for the solution. Myth #5: The timeline to implement is too long. It’s true, automation can involve a lot of functions and tasks – especially if you take it on yourself. By calling out to a hosted environment, Experian’s Decisioning as a Service can take as few as six weeks to implement since it simply augments a current system and does not replace a large piece of software. Myth #6: Manual decisions give a better member experience. Actually, manual decisions are made by people with their own points of view, who have good days and bad days and let recent experiences affect new decisions. Automated decisioning returns a consistent response, every time. Regulators love this! Myth #7: We don’t use Experian data. Experian’s Decisioning as a Service is data agnostic and has the ability to call out to many third-party data sources and configure them to be used in decisioning. --- These myth busters make a great case for implementing automated decisioning in your loan origination system instead of a reason to avoid it. Learn more about Decisioning as a Service and how it can be leveraged to either augment or overhaul your current decisioning platforms.

Panel discussion on Reinventing Identity for the Digital Age at Electronic Signature & Records Association (ESRA) conference

Under the updated requirements for Customer Due Diligence, financial institutions must expand programs.

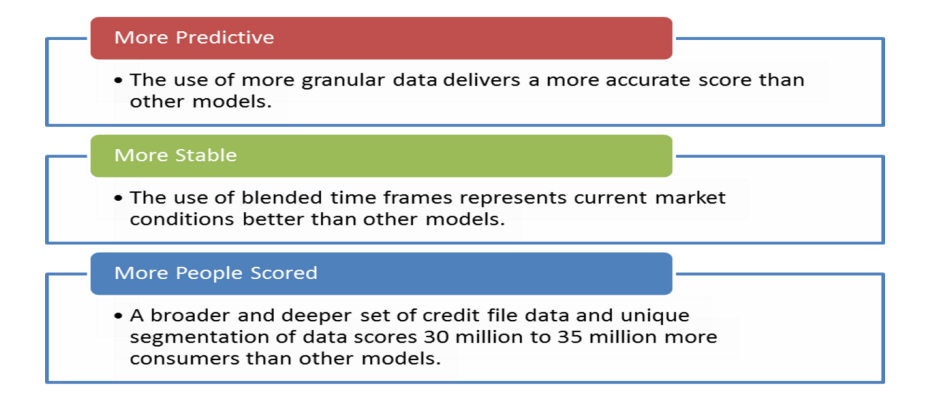

More lenders are turning to VantageScore® to help achieve their goals and reduce risk

For members of the U.S. military, relocating often, returning home following a lengthy deployment and living with uncertainty isn’t easy. It can take an emotional and financial toll, and many are unprepared for their economic reality after they separate from the military. As we honor those who have served our country this Veterans Day, we are highlighting some of the special financial benefits and safeguards available to help veterans. Housing Help One of the best benefits offered to service members is the Veteran’s Administration (VA) home-loan program. Loan rates are competitive, and the VA guarantees up to 25 percent of the payment on the loan, making it one of the only ways available to buy a home with no down payment and no private mortgage insurance. Debt Relief Having a VA loan qualifies military members for a Military Debt Consolidation Loan (MDCL) that can help with overcoming financial difficulties. The MDCL is similar to a debt consolidation loan: take out one loan to pay off all unsecured debts, such as credit cards, medical bills and payday loans, and make a single payment to one lender. The advantage of a MDCL? Paying a lower interest rate and closing costs than civilians and far less interest than paying the same bills with credit cards. These refinancing loans can be spread out over 10, 15 and sometimes 30 years. Education Benefits The GI Bill is arguably the best benefit for veterans and members of the armed forces. It helps service members pay for higher education for themselves and their dependents, and is one of the top reasons people enlist. Eligible service members receive up to 36 months of education benefits, based on the type of training, length of service, college fund availability and whether he or she contributed to a buy-up program while on active duty. Benefits last up to 10 years, but the time limit may be extended. Saving & Investing Money According to the Department of Defense’s annual Demographics Report, 87 percent of military families contribute to a retirement account. Service members who participated in the Thrift Savings Plan, however, are often unaware of their options after they separate from service, and many don’t realize the advantages of rolling their plans into an IRA or retirement plan of a new employer. Safeguarding Identity Everyone is a potential identity theft target, but military personnel and veterans are particularly vulnerable. Routinely reviewing a credit report is one way to detect a breach. The Attorney General's Office provides general information about what steps to take to recover from identify theft or fraud. Today is a great time to consider ways to support your veteran and active military consumers. They are deserving of our support and recognition not just today but continuously. Learn more about services for veterans and active military to understand the varying protections, and how financial institutions can best support military credit consumers and their families.

Experian analysis shows that 2.5M consumers will have a foreclosure, short sale or bankruptcy fall off their credit report between June 2016 and June 2017

Experian announces partnership with U.S. Communities to help state and local public agencies prevent fraud, maximize revenue, strengthen security

Will they still aspire to achieve the “American Dream” of education, homeownership and raising a family? Are Millennials ready for a mortgage?

Most businesses are familiar with credit bureaus today, but myths still exist around reporting credit data. Let's examine the top three and bust them.

CNP fraud accounts for 60%-70% of card fraud in many countries & is increasing. US merchants/card issuers likely will see rise in CNP fraud w/EMV migration

Prescriptive solutions can synthesize big data, analytics, and business strategies to provide businesses an optimized workflow to reach a final decision.