Models & Scores

A robust segmentation analysis contains two components: first is generation of potential segments, and the second is generation of potential segments.

Experian introduces new trended attributes to help lenders better serve consumers across the credit life cycle

Trended attributes can provide significant lift in the development of segmentation strategies and custom models are used effectively across the life cycle.

The phrase swap set refers to “swapping out” a set of customer accounts and replacing them with, or “swapping in,” a set of good customer accounts.

With so much data being generated by our social media obsession, should lenders consider social media insights to assess credit risk?

APIs--Application Programming Interfaces--are the hidden backbone of our modern world which allow software programs to communicate with one another.

VantageScore found consumers rendered “unscoreable” by commonly used credit scoring models are nearly identical financial/credit behavior to scoreables

More lenders are turning to VantageScore® to help achieve their goals and reduce risk

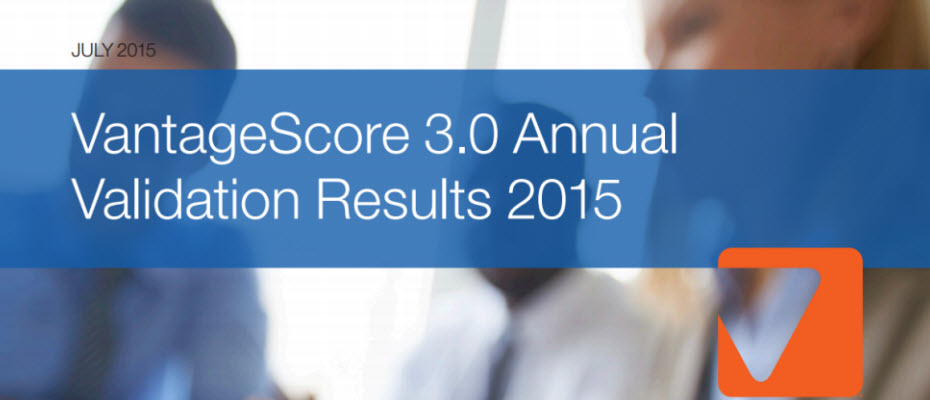

As credit behavior and economic conditions evolve, using a model that's validated regularly can give lenders greater confidence in the model’s performance.

A recent survey commissioned by VantageScore® Solutions, LLC found that among consumers who are unable to obtain credit, 27% attribute the situation to lack of a credit score. Most consumers support newer methods of calculating credit scores 49% feel that consistent rental, utility and telecommunications payments should count in determining credit scores 50% agree that competition in the credit scoring marketplace is beneficial Lenders can help solve the credit gap by using advanced risk models that can accurately score more consumers. The result is a win-win: More consumers get access to mainstream credit, and lenders gain more customers. >> Infographic: America’s Giant Credit Gap VantageScore® is a registered trademark of VantageScore Solutions, LLC.

Experian® recently released the 2015 State of Credit report, which analyzes key credit metrics across the nation.

VantageScore® models are the only credit scoring models to employ the same characteristic information and model design across the three credit bureaus.

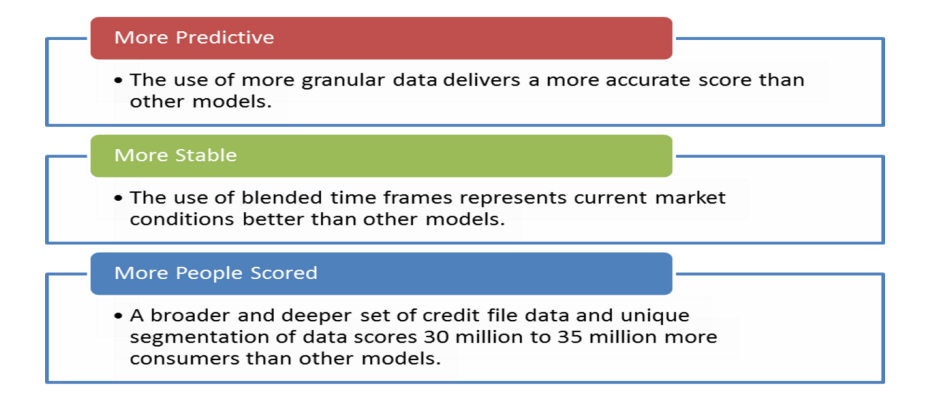

According to VantageScore® Solutions' annual validation study, VantageScore 3.0 scores 36 million incremental consumers considered unscoreable by conventional credit scoring models.

As the summer home buying season kicks into high gear, a newly released survey shows the importance of understanding credit scores and their impact on homebuyer behavior.

According to research from VantageScore® Solutions LLC, 30 to 35 million people are not scored by the most popular credit-scoring models. When measured by more modern scoring methodologies — methods that leverage the data that exists in a person's credit file better — as many as 10 million of these unscoreable consumers were found to have prime or near prime credit scores. The study reinforces the importance of using advanced credit scores in order to profitably grow portfolios while providing consumers with access to fair and equitable credit. Credit Scoring Gaps Are Leaving Millions of Consumers Behind VantageScore® is a registered trademark of VantageScore Solutions, LLC.