Financial Access

Experian is unlocking the power of data to facilitate access to fair and affordable credit for both consumers and businesses. With our products, services and partnerships, we are working to improve financial inclusion for all. Read about our latest financial access news below:

Building a credit history takes time. Establishing a credit history early in life can help ensure you have access to affordable credit when you need it. The problem is that people tend to learn about credit and finances through trial and error. This is unfortunate because recovering from financial mistakes takes time, too. In fact, it could take years to rebound from one financial misstep. This trend is especially common for young adults who are just beginning to get their financial feet wet, and it’s one of the many reasons credit education and improving the financial health of consumers of all ages is core to our mission at Experian. As Director of Consumer Education and Advocacy, I get the opportunity to talk to a variety of students and young adults across the country on a regular basis. Millennials and Gen Z are often labeled slackers, but I don’t believe that for an instant. They experienced the financial crisis firsthand in their early years, and they really don’t want to repeat what their parents went through. Can you blame them, really? One thing we know for certain about young adults is they are very interested in learning as much as they can about money, finance and credit, and it’s our goal to be an educational resource to them. As the saying goes, you don’t know what you don’t know. We have a chance to give younger generations the information and tools to know more than previous generations did at their ages. Here are some of my favorite tried and true tips to help set young adults up for credit success: Start small and grow slowly. A secured account with a small credit limit can establish your credit history and help you start saving at the same time. Good credit and strong savings habits go hand-in-hand. You don't need a credit card with a high limit to have good credit. Use the credit you have wisely. Good credit scores are not about having a lot of credit, but rather about how you use the credit you have available. Make a small purchase each month and pay it in full. That will show you can use credit well without taking on debt. Use your cell phone to improve your credit. With Experian Boost, you can add positive telecom and utility payments to your credit history and possibly boost your credit score. In the past, failing to pay your utility or cell phone bills could hurt your credit, but paying on time didn't help. With Experian Boost, that's changed. Use technology to make managing your credit automatic. Millennials and Gen Zers are the most technologically savvy generations in our history. Use technology, such as online banking apps and credit management tools like the Experian app, to automate savings and payments, to alert you to potential fraud and to track your progress as you build your credit history. We know helping people better understand and access credit is a team effort, and we work closely with our advocacy networks to increase our impact. We recently joined the American Bankers Association to provide young adults with financial education. Leading up to Get Smart About Credit Day, we hosted a Facebook Live with Jeni Pastier, Director of Financial Education Programs for the American Bankers Association to address credit topics young adults typically don’t understand or know about at all. You can watch the full video here and find additional articles to get smarter about credit on the Ask Experian blog.

I was born and raised in Germany and had the privilege of moving to the U.S. for my undergraduate degree. When I started school, my parents made a deal with me that they would pay one-third of my tuition. I got a job at the campus library to pay another third but still was short by a third. To cover the gap, I decided to try my luck as an entrepreneur. Specifically, the dollar was very strong due to which it seemed feasible to buy a German luxury car in my native Germany, refurbish it to U.S. specs, drive it for a little while and still turn a healthy profit. In order to purchase my first car, I needed a loan. However, like most new immigrants, I was credit invisible. Meaning, the credit history I had in Germany did not come with me to the U.S. Because of this, I was forced to rely on alternative lending as traditional lenders did not have enough information to assess if I was a good credit risk. With no other options, I turned to an alternative lender and secured a high interest loan. Thankfully, I was able to maintain my payments and paid off the loan in fifteen months, that is, when I sold the car. At this time, obtaining credit from an alternative lender was not factored into a traditional credit history. This meant that even though I repaid the loan responsibly, it did not help build my U.S. credit file or my credit score when I was ready to do it all again. This experience is what fuels my passion to maintain Experian’s position as the leader in alternative credit data and improve consumer financial health. We know that a consumer’s traditional lending history for things like credit cards, personal loans, auto loans, and mortgages are a proven method to assess creditworthiness, but sometimes there isn't enough data to score all consumers. Many consumers who are excluded from the traditional credit ecosystem are in fact creditworthy, but due to an international move, divorce or simply a lack of experience with credit, they’re unscorable and or invisible to lenders. Whether you’re new to the country or just getting your financial feet wet, starting to build your credit history can be difficult. If we indeed can play a role in helping consumers live the American dream, I believe it’s our responsibility to do that. The good news is the lending market is in a pivotal state of change and I believe it’s for the better. At Experian, we can now use the responsible payments consumers make to alternative lenders as well as their rental payments, professional licensures, utility and cell phone payments, and, of course, their traditional credit history to help consumers gain access to the financial services they need. We recently announced Experian Lift™ - a new suite of credit score products that combines exclusive traditional credit, alternative credit and trended data assets to create a more holistic picture of consumer creditworthiness. We believe Experian Lift may improve access to credit for more than 40 million credit invisibles. It’s another step in our commitment to helping improve the financial health of consumers everywhere. As you may know, earlier this year, Experian launched Experian Boost – a free and first-of-its-kind financial tool that empowers consumers to add positive telecom and utility payment history directly into their Experian credit file for an opportunity to instantly increase their FICO Score. Through Experian Boost, we’re empowering consumers to play an active role in building their credit histories. And, with Experian Lift, we’re empowering lenders to identify consumers who may otherwise be excluded from the traditional credit ecosystem. Thin file or subprime consumers have typically been viewed as a fringe and stigmatized segment of society. I can speak from personal experience and say this is not the case. With more than 100 million consumers lacking access to fair and affordable credit, we know this is mainstream America and we need to continue to provide solutions. As the consumer’s bureau, our goal is to help consumers and maintain access to credit. We’re proud of our latest innovations and will continue to identify new means to help consumers gain access to the financial services they need.

Retailers are already starting to display their Christmas decorations in stores and it’s only early November. Some might think they are putting the cart ahead of the horse, but as I see this happening, I’m reminded of the quote by the New York Yankee’s Yogi Berra who famously said, “It gets late early out there.” It may never be too early to get ready for the next big thing, especially when what’s coming might set the course for years to come. As 2019 comes to an end and we prepare for the excitement and challenges of a new decade, the same can be true for all of us working in the lending and credit space, especially when it comes to how we will approach the use of alternative data in the next decade. Over the last year, alternative data has been a hot topic of discussion. In fact if you typed “alternative data and credit” into a Google search today you would get more than 200 million results. That’s a lot of conversations, but while nearly everyone seems to be talking about alternative data, we may not have a clear view of how alternative data will be used in the credit economy. How we approach the use of alternative data in the coming decade is going to be one of the most important decisions the lending industry makes. Inaction is not an option, and the time for testing new approaches is starting to run out – like Yogi said, it’s getting late early. And here’s why: millennials. We already know that millennials tend to make up a significant percentage of consumers with so-called “thin-file” credit reports. They “grew up” during the Great Recession and that has had a profound impact on their financial behavior. Unlike their parents, they tend to have only one or two credit cards, they keep a majority of their savings in cash and, in general, they distrust financial institutions. However, they currently account for more than 21 percent of discretionary spend in the U.S. economy, and that percentage is going to expand exponentially in the coming decade. The recession fundamentally changed how lending happens, resulting in more regulation and a snowball effect of other economic challenges. As a result, millennials must work harder to catch up financially and are putting off major life milestones that past generations have historically done earlier in life, such as home ownership. They more often choose to rent and, while they pay their bills, rent and other factors such as utility and phone bill payments are traditionally not calculated in credit scores, ultimately leaving this generation thin-filed or worse, credit invisible. This is not a sustainable scenario as we enter the next decade. One of the biggest market dynamics we can expect to see over the next decade is consumer control. Consumers, especially millennials, want to be in the driver’s seat of their “credit journey” and play an active role in improving their financial situations. We are seeing a greater openness to providing data, which in turn enables lenders to make more informed decisions. This change is disrupting the status quo and bringing new, innovative solutions to the table. At Experian we have been testing how advanced analytics and machine learning can help accelerate the use of alternative data in credit and lending decisions. And we continue to work to make the process of analyzing this data as simple as possible, making it available to all lenders in all verticals. To help credit invisible and thin-file consumers gain access to fair and affordable credit, we’ve also recently announced Experian Lift, a new suite of credit score products that combines exclusive traditional credit, alternative credit and trended data assets to create a more holistic picture of consumer creditworthiness that will be available to lenders in early 2020. This new Experian credit score may improve access to credit for more than 40 million credit invisibles. There are more than 100 million consumers who are restricted by the traditional scoring methods used today. Experian Lift is another step in our commitment to helping improve financial health of consumers everywhere and empowers lenders to identify consumers who may otherwise be excluded from the traditional credit ecosystem. This isn’t just a trend in the United States. Brazil is using positive data to help drive financial inclusion, as are other around the world. Like I said, it’s getting late early. Things are moving fast. Already we are seeing technology companies playing a bigger role in the push for alternative data – often powered by fintech startups. At the same time there also has been a strong uptick in tech companies entering the banking space. Have you signed up for your Apple credit card yet? It will take all of 15 seconds to apply, and that’s expected to continue over the next decade. All of this is changing how the lending and credit industry must approach decision making, while also creating real-time frictionless experiences that empower the consumer. We saw this with the launch of Experian Boost earlier this year. The results speak for themselves: hundreds of thousands of previously thin-filed consumers have seen their credit scores instantly increase. We have also empowered millions of consumers to get more control of their credit by using Experian Boost to contribute new, positive phone, cable and utility payment histories. Through Experian Boost, we’re empowering consumers to play an active role in building their credit histories. And, with Experian Lift, we’re empowering lenders to identify consumers who may otherwise be excluded from the traditional credit ecosystem. That’s game changing. Disruptions like Experian Boost and newly announced Experian Lift are going to define the coming decade in credit and lending. Our industry needs to be ready because while it may seem early, it’s actually getting late.

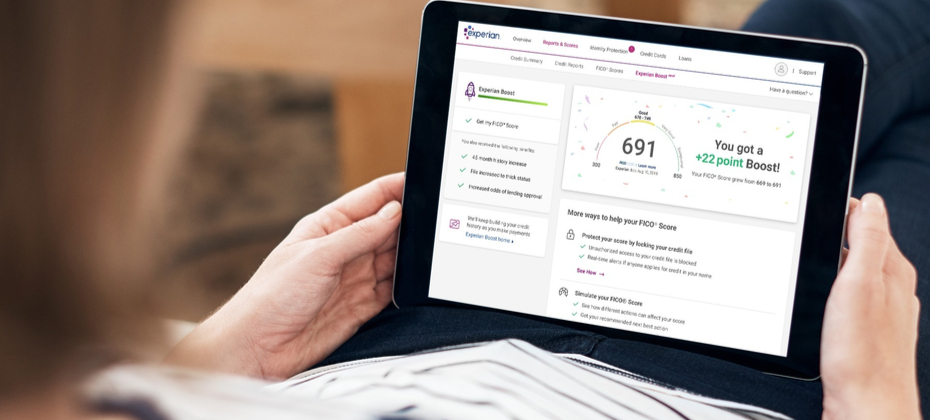

At Experian, we know a credit score is the gatekeeper to better financial opportunities, which is why we are committed to developing products and services that support consumers in their financial journey. Six months ago, we hit a major milestone in bringing this commitment to life with the launch of Experian Boost. This innovative tool gave consumers the ability to add positive telecom and utility payment history directly to their credit file for an opportunity to instantly increase their credit scores for the first time. When we launched Experian Boost, we knew there were more than 100 million Americans who didn’t have fair access to credit because of a limited credit history or a subprime score. We also knew these consumers were often forced to pay higher interest rates and fees for financial services. Today, as we look at our Experian Boost results, we know we’re helping to change that. To date, for consumers who’ve used Experian Boost, we’ve seen: More than 11 million cumulative FICO Score points boosted FICO Scores increased for 2 out of 3 users with an average increase of more than 10 points Of those who boosted their credit scores, an average of 13% moved up a credit tier and of those in the “poor” credit tier, 24% moved to a “fair” tier Approximately 90% of “thin” file consumers who improve their credit scores saw an average increase of 19 points California, Texas and Florida rank 1-2-3 in number of consumers who have boosted their scores and total points boosted To say we’re pleased with the positive feedback we’ve received about Experian Boost to date would be an understatement, but we’re not surprised. For years, lenders have been seeking new means to identify creditworthy consumers. At the same time, consumers have been asking for more control of their data and credit where credit is due. This is exactly what we’re providing with Experian Boost. We’re helping to level the playing field and reward positive behavior and it’s not going unnoticed. Members of the credit counseling and advocacy community have reached out with excitement about Experian Boost. This solution is giving many of their clients a tangible way to impact their credit scores and improve their financial lives. Improving consumer financial health is a core part of our sense of purpose and we’re just getting started. We’ll continue to enhance Experian Boost and develop new products and solutions to improve financial access to for more consumers. To find out more about the Experian Boost, please visit www.experian.com/boost.

We are delighted to announce our investment in bonify, a German fintech start-up dedicated to giving consumers better insights into their creditworthiness. bonify gives its 500,000 customers easy access to their creditworthiness and financial data, offering them a number of financial management tools to help analyse and optimise their financial situation. At Experian, we believe very deeply in the power of data to help improve people’s lives. That’s why we’re so excited by bonify’s continued goal to improve its users’ financial lives, and the steps it is taking to help people in Germany understand and benefit from their financial information. We are delighted to join a number of investors in supporting the growth of this innovative start-up. Charles Butterworth, Managing Director Experian UK, Ireland and EMEA, said: "We are excited by the way bonify is helping people in Germany understand, engage with and improve their credit scores. We look forward to supporting the team as an investor and partner in their future growth.“ Founder and CEO of bonify, Dr. Gamal Moukabary, said: “Experian's investment shows that we are on the right track. It rewards our achievements and our unique value proposition. Experian is an ideal investor and partner for us to support the next growth phase. Our goal is to expand our operations into other European countries.” Manuel Silva Martínez, Partner and Head of Investments, Santander InnoVentures, added: “We are delighted to welcome Experian Ventures to bonify. Experian will add tremendous value and technical expertise to bonify’s product roadmap. We are thrilled to support bonify as we accelerate growth and help more and more people across Germany and Europe with taking control of their finances in a sound and responsible way.

For the past several years, Experian has been on a journey to help drive financial inclusion for millions of people around the world. This has required significant changes in how we operate, who we partner with, and the products and solutions we offer —and with those changes comes a renewed sense of purpose. What we do and the actions we take have the potential to improve lives. We are actively seeking out unresolved problems and creating products and technologies that will help transform the way businesses operate and consumers thrive in today’s society. But we know we can’t do it alone. That’s why over the last year, we have built out an entire team of account executives and other support staff that are fully dedicated to developing and supporting partnerships with leading fintech companies. We’ve made significant strides that will help us pave the way for the next generation of lending, while improving the financial health of more people around the world. Earlier this week, I attended the FinovateSpring conference in San Francisco to speak with fintechs and financial institutions about ways to put financial health at the center of an organization’s plans to build trust, reach new customers and ultimately grow business. We are developing platforms that are designed to play to the strengths of fintechs and disrupt the industry. In the past, we have looked at unresolved problems and asked ‘why?’ Today, with our fintech partners, we look at potential solutions to these unresolved challenges and say, ‘why not.’ As part of our concentration on fintech, Experian has made significant investments in alternative data, such as the game-changing Experian Boost platform, which was launched just two months ago and is already reshaping the way consumers gain access to credit. Since we launched Experian Boost, consumers across America have instantly increased their credit score by sharing their bill payment history for things like utilities, mobile phones and cable TV payments – payments which had never been factored into a credit score before. And, yes, this platform came to fruition as a result of a fintech partnership. We have partnered with fintechs in other powerful ways, too. Our new Ascend Analytical Sandbox – a first-of-its-kind data and analytics platform - gives companies instant access to more than 17 years of depersonalized credit data on more than 220 million U.S. consumers. This creates better opportunities for consumers by allowing our clients to provide more tailored solutions. It’s a great example of the power of analytics and we’re very proud of it. During our time at Finovate, we were able to engage in meaningful conversations with fintech leaders who were united in our goal of helping more consumers access the financial services they need. We’re more inspired than ever before to continue to build and explore strategic partnerships that will ultimately improve the lives of American consumers.

Today marks a notable milestone in our company’s history and for consumers. Today we officially launched Experian Boost, a free tool that, for the first time, will allow millions of consumers to add positive payment history directly into their credit file for an opportunity to instantly increase their credit score. For the past several years, we have been working to develop new products and innovations that will disrupt the credit industry and help improve the financial lives of consumers. This commitment to financial inclusion has defined us and created a real sense of purpose for everyone who works here – and that purpose is realized with the launch of Experian Boost today. There are more than 100 million Americans who don't have access to credit today. A low credit score, due to a thin file or incomplete information, may force these consumers to rely on high interest credit cards and loans. The fact that many of these consumers consistently and responsibly pay cell phone and utility bills on time every month hasn’t seemed to matter. At Experian, we know that’s not right. A good credit score is a gatekeeper to better financial opportunities. We need to develop products and services that make achieving and maintaining a good score easier, not harder. As the consumer’s bureau, we want to ensure that as many people as possible can access and participate in the financial system, and we believe everyone deserves a fair shot at achieving their financial dreams. We have a fundamental mission that is shared by our colleagues around the world: to strive to be a champion for the consumer. With Experian Boost, we're bringing that mission to life and I couldn’t be prouder. Many of our colleagues at Experian worked tirelessly over the last few years to make this day a reality. To everyone who’s played a part, I offer my very heartfelt thanks. It’s truly a great day to be a part of Experian, and we know there will be a lot of great days ahead for all the consumers who will benefit from having their credit score truly reflect who they are. To find out more about the Experian Boost, please visit experian.com/boost.

Financial exclusion is a global issue with an estimated 1.7 billion adults currently ‘unbanked’ . Experian’s core mission is to help bring financial inclusion to every adult in the world. There are currently millions of ‘thin file’ consumers and SMEs in sub-Saharan Africa. These are consumers with limited information on a traditional credit bureau or have no information at all, so-called ‘invisibles’, who find themselves excluded from mainstream finance. They often face more difficulty – or higher costs - when applying for financial products or services. That’s why we are proud to announce today the launch of a ground-breaking new smartphone app, GeleZAR, in South Africa, which aims to bring more micro-entrepreneurs into the mainstream economy and ensure they get the credit score they deserve.. Using the expertise of our global innovation hubs, we have developed a unique financial education and credit scoring mobile app. GeleZAR is designed to educate entrepreneurs and individuals on how to manage their finances, budget and credit score in a fun, entertaining and digestible way. It can also advise individuals on how to maintain a good credit health and recommends remedial actions where needed. In partnership with a local South African consumer and fintech developer, Experian designed the app specifically for entry-level smartphones. We are also working with one of the largest low-cost mobile phone retailers in Africa to trial the app which has been pre-installed on a range of its entry-level smartphones.. The intention is to extend the rollout and make the app accessible for free on more than six million devices annually. Working with alternative data that an individual user consents to share on the app, GeleZAR will be able to assess an individual’s stability, build a credit profile and potentially improve their credit score. This in turn could enable them to access a broader range of financial products at more affordable interest rates. This is a great example of how Experian is innovating to find new ways to empower our customers while uplifting societies. It also fulfils our passion for financial inclusion and the accurate assessment of affordability. Experian’s cutting edge technological capabilities enable us to use the power of data to transform lives, businesses and economies for the better. Through our pioneering work in this space we hope to help consumers around the world on their credit journey. GeleZAR is just one of the ways we are delivering on our mission to build and improve the credit files of millions of people in South Africa and beyond.

Elio Vitucci, CEO of Experian MicroAnalytics, authored the op-ed Financial Empowerment for the Emerging Market Consumer in U.S. News & World Report. To date, Experian MicroAnalytics has extended over 4.9 billion credit offers to the world’s unbanked people, and nearly half of those offers were in the past year. The new emerging market consumer is becoming empowered with tools and services needed for a better quality of life and economic vitality. Experian MicroAnalytics contributes to global progress by helping those with no credit history gain access to credit and financial products for their businesses and personal needs. In regions where financial history doesn't exist, understanding creditworthiness is a challenge. While only a small minority of people in emerging markets have access to credit services, the vast majority have access to mobile services — most of them on a prepaid plan. As such, an alternate credit identity can now be established. Financial services in the emerging world are drastically underserving the potential banked population. Long-term economic growth in the emerging world hinges on access to financial services. Unlocking the new consumer's credit capability is the new financial frontier. Learn more about how Experian is empowering emerging market consumers with financial products and services to improve quality of life and increase prosperity around the world.