Customer Targeting & Segmentation

Many marketing budgets were already small prior to the global pandemic, so coming out of it, to say every marketing dollar counts is an understatement.

Here's a brief FCRA-related compliance overview to refresh your memory on various FCRA requirements when requesting and using consumer credit reports.

Amid the fallout of COVID-19, I often find myself thinking about the impact the pandemic has had and will have on businesses in the coming months—particularly those within the automotive industry. The impact has reached all facets of the industry, leaving dealerships to take unprecedented action. Some have temporarily closed, while many have shifted business priorities to focus on maintenance and repair. Like everyone, we in the automotive industry are concerned about the health and safety of our family, friends and communities. Much like the rest of small business owners, those that oversee dealerships are also concerned about the wellbeing of their work families. The automotive industry is a pillar of our economy, and dealerships are staples within our local communities. Experian has an unwavering commitment to help the industry navigate these uncertain times and address challenges as they arise. The pandemic has impacted groups of people differently and at different times. It’s important for those within the automotive industry to understand how consumer sentiment and priorities will shift over the coming months, in order to address their most pressing needs. As such, Experian launched a daily survey of the general population to gain insight into shifting consumer sentiment as a result of the pandemic. The survey reveals how consumers are dealing with the outbreak across key industries, including automotive. As of May 4, 2020, only 20 percent of Americans plan on buying a new car, truck, van or motorcycle within the next few months, and of those, only 50 percent plan to continue the purchase as planned. 26 percent plan to delay the purchase a few months. While car shopping may not be a priority for most in the coming months, there are consumers who will need to replace their vehicle sooner rather than later—perhaps their lease is set to expire, or they’ve experienced car trouble. In these instances, it’s important for dealers to be able to connect with these consumers to help them understand the options available to them. With this urgency in mind, Experian is providing dealers with complimentary access to nationwide and local automotive market trends. The information will be updated weekly to help dealers gain insight into current sales trends and website traffic, better understand in-market car shoppers and identify the most effective communications channels. For instance, during the week of April 27, dealer website traffic was down 11 percent from the same time last year. That said, web site traffic has picked back up over the past few weeks.. With the short- and long-term impacts of the pandemic largely unknown, dealerships must adapt quickly. Consumers' vehicle needs will shift based on circumstance, and it’s important for dealers to continually assess the market. We are all adapting to our new environment, and will need to collaborate to find ways to combat the fallout—it’s a difficult time for many, including dealers. The automotive market will recover, and Experian is committed to helping the automotive industry navigate the recovery and ensure car shoppers can find vehicles that meet their needs. To view the Automotive Trends & Marketing Insights and sign up to receive your complimentary local market trends, click here. To view the Consumer Sentiment Index, click here.

Download our case study to learn how home equity lender, Spring EQ, leveraged Experian Boost to help applicants qualify for better loan rates and terms.

Experian experts provided insight on how data furnishers can help support small businesses amidst the pandemic while complying with recent regulations.

Historically, economic hardships have directly impacted loan performance. Are you prepared to navigate and successfully respond to the current environment?

Learn the benefits of leveraging alternative credit data to better assess risk at the onset of the loan decisioning process. Read more.

At Experian, we are here to help consumers understand how the credit reporting system and personal finance overall will move forward during the pandemic.

We are excited to announce that Experian has been selected as a Fintech Breakthrough Awards winner in the Consumer Lending Innovation category.

If you're looking for a competitive edge in 2020, Vision is your ticket into differentiating your organization with the latest insights and innovation.

With shrinking budgets and increased demand for customized messaging, financial marketing teams have numerous challenges. Learn how the best find success.

Exploring some of the top trends for the financial services industry going into the new decade from data and decisioning to fraud and customer experience.

According to research, only 15% of American consumers have swapped out their go-to credit card in the past year. Here's how to keep your card top of mind.

Financial firms are turning to customer acquisition engines to help them build, test and optimize custom targeting strategies faster than ever before.

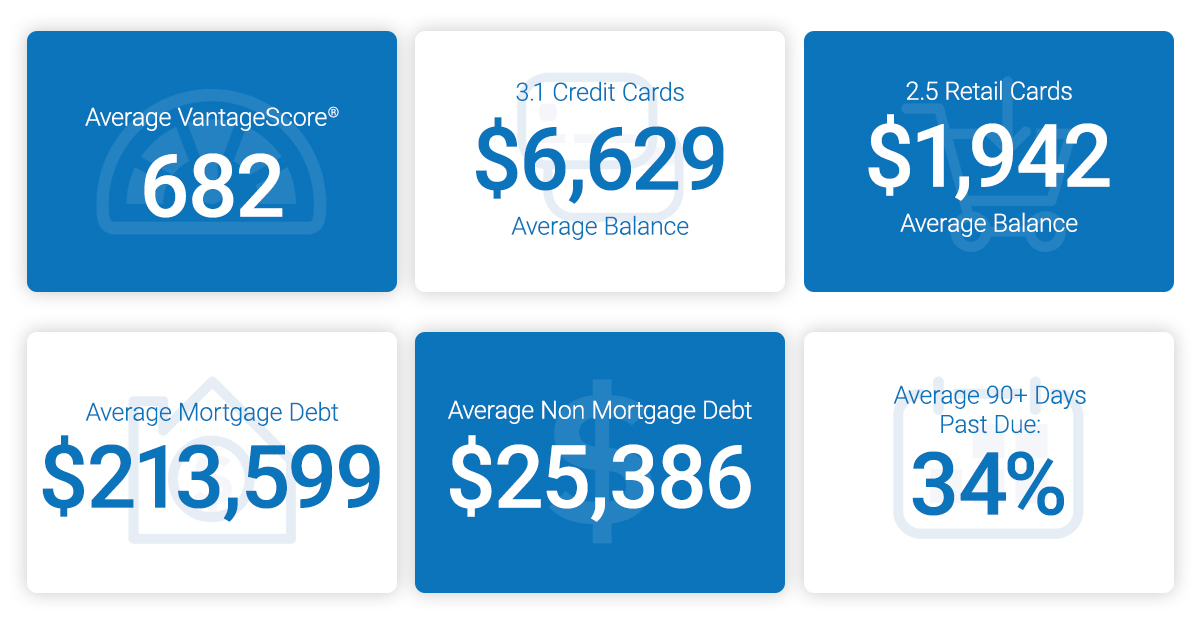

As look forward to the next decade, things are looking up. The 10th annual State of Credit Report highlights consumer credit scores and borrowing behavior.