Telecommunications, Cable & Utilities

Telecommunications, Cable & Utilities

Utilizing a customer journey map – from acquisitions through collections

Telecommunications, Cable & UtilitiesCreating a customer journey map, and seeing it through from acquisitions to collections, can help you better define messaging and channels to best reach your audience.

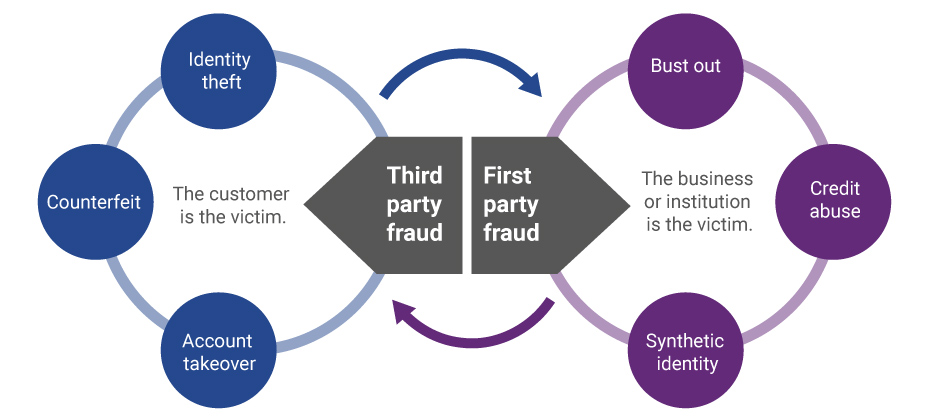

Third-party and first-party schemes are now interchangeable, and traditional fraud detection practices are less effective in fighting these evolving fraud types.

Results reveal success for virtual negotiation in collections space

Telecommunications, Cable & UtilitiesAs more collectors transition from "dialing for dollars" to digital solutions, they are seeing early results and success with virtual negotiation tools.

Putting Customer Experience at the core of your debt collection strategy

Telecommunications, Cable & UtilitiesMany clients use the same debt collection strategy they’ve used for years never considering the customer experience for the debtor

The first wave of Gen Z are coming onto the credit file. Here is a first look at how they are behaving, and what this means for businesses and finance companies.

Synthetic identity fraud is an epidemic that does more than negatively affect portfolio performance. It can hurt your reputation as a trusted organization.

Synthetic ID fraud is a growing problem driven by an online and mobile-driven market, along with an increase in data breaches and dark web sharing.

New CFPB study demonstrates the importance of moving forward with inclusion of new sources of high-quality financial data — like on-time payment data from rent, utility and telecommunications providers — into a consumer’s credit file.

Later this year, FICO will retire its Score V1, making it mandatory for those lenders still using the old software to find another solution.

The final day of Vision 2017 brought a seasoned group of speakers to discuss a wide range of topics. In just a few short hours, attendees dove into a first look at Gen Z and their use of credit, ecommerce fraud, the latest in retail, the state of small business and leadership. Move over Millennials – Gen Z is coming of credit age Experian Analytics leaders Kelley Motley and Natasha Madan gave audience members an exclusive look at how the first wave of Gen Z is handling and managing credit. Granted most of this generation is still under the age of 18, so the analysis focused on those between the ages of 18 to 20. Yes, Millennials are still the dominant generation in the credit world today, standing strong at 61 million individuals. But it’s important to note Gen Z is sized at 86 million, so as they age, they’ll be the largest generation yet. A few stats to note about those Gen Z individuals managing credit today: Their average debt is $12,679, compared to younger Millennials (21 to 27) who have $65,473 in debt and older Millennials (28 to 34) who sport $121,460. Given their young age, most of Gen Z is considered thin-file (less than 5 tradelines) Average Gen Z income is $33,000, and average debt-to-income is low at 5.7%. New bankcard balances are averaging around $1,574. As they age, acquire mortgages and vehicles, their debt and tradelines will grow. In the meantime, the speakers provided audience members a few tips. Message with authenticity. Think long-term with this group. Maintain their technological expectations. Build trust and provide financial education. State of business credit and more on the economy Moody’s Cris deRitis reiterated the U.S. economy is looking good. He quoted unemployment at 4.5%, stating “full employment is here.” Since the recession, he said we’ve added 15 million jobs, noting we lost 8 million during the recession. The great news is that the U.S. continues to add about 200,000 jobs a month, and that job growth is broad-based. Small business loans are up 10% year-to-date vs. last year. While there has been a tremendous amount of buzz around small business, he adds that most job creation has come from mid0size business (50 to 499 employees). The case for layered fraud systems Experian speaker John Sarreal shared a case study that revealed by layering on fraud products and orchestrating collaboration, a business can go from a string 75% fraud detection rate to almost 90%. Additionally, he commented that Experian is working to leverage dark web data to mine for breached identity data. More connections for financial services companies to make with mobile and social Facebook speaker Olivia Basu reinforced the need for all companies to be thinking about mobile. “Mobile is not about to happen,” she said. “Mobile is now. Mobile is everything. You look at the first half of 2017 and we’re seeing 40% of all purchases are happening on mobile devices.” Her challenge to financial services companies is to make marketing personal again, and of course leverage the right channels. Experian Sr. Director of Credit Marketing Scott Gordon commented on Experian’s ability to reach consumers accurately – whether that be through direct or digital delivery channels. A great deal of focus has been around person-based marketing vs. leveraging the cookie. -- The Vision conference was capped off with a keynote speech from legendary quarterback and Super Bowl MVP Tom Brady. He chatted about the details of this past season, and specifically the comeback Super Bowl win in February 2017. He additionally talked about leadership and what that means to creating a winning team and organization. -- Multiple keynote speeches, 65 breakout sessions, and hours of networking designed to help all attendees ready themselves for growing profits and customers, step up to digital, regulatory and fraud challenges, and capture the latest data insights. Learn more about Experian’s annual Vision conference.

In just a few short hours, Vision attendees immersed themselves into the depths of the economy, risk models, specialty finance data, credit invisibles, student loan data, online marketplace lending and more. The morning kicked off with one of the most respected and trusted macroeconomists in the U.S., Diane Swonk. With a rap sheet filled with advising central banks and multinational companies, Swonk treated a packed house to a look back on what has transpired in the U.S. economy since the Great Recession, as well as launching into current state and speculating on the months ahead. She described the past decade not as “lost, but rather lagging.” She went onto to say this past year was transitional, and while markets slowed slightly during the months leading up the U.S. presidential election, good things are happening: We’ve finally broken out of the 2% wage rut Recruiting on college campuses has picked up The labor force is growing Debt-to-income levels have returned to where they were prerecession and Investment is coming back. “I believe we’ll see growth over 2% this year,” said Swonk. Still, change is underway. She commented on how the way U.S. consumer spending is changing, and of course we’re seeing a restructuring in the retail space. While JC Penney announces store closings, you simultaneously see Amazon moving from “click to brick,” dabbling in the opening of some actual storefronts. Globally, she said the economy is the strongest it has been in eight years. She closed by noting there is a great deal of political change and unrest in the world today, but says, “Never underestimate our abilities when we tap our human capital.” -- More than 100 attendees filled a room to hear about the current trends and the future of online lending with featured guests from Oliver Wyman, Marlette Funding and Lending USA. While speakers commented on the “hiccup” in the space last year with some layoffs and mergers, volume has continued to double every year for the past several years with roughly $40 billion in cumulative originations today. Panelists discussed the use of alternative data to decision, channel bias, the importance of partnerships and how the market will see fewer and fewer players offering just one product specialty. “It is expensive to acquire customers, so you don’t just want to have one product to sell, but rather a range,” said Sharat Shankar of Lending USA. -- The numbers in the student lending universe are astounding. In a session focused on the U.S. student loan market, new Experian data reveals there is $1.49 billion in total student loan outstandings. In fact, total outstandings have grown 21% over the past four years, while the number of trades have only grown 4%. Costs are skyrocketing. The average balance per trade has grown 17% over the past four years. “We don’t ration education in this country,” said Joe DePaulo of College Ave. Student Loans. “We give everyone access to liquidity when it comes to federal student loans – and it’s not like that in other countries.” While DePaulo notes the access is great, offering many students the opportunity to obtain higher education, he says the problem is with disclosures. Guardians are often the individuals filling out the FAFSA, but the students inherit the loans. Students, he says, rarely understand how much their monthly payment will ultimately be after graduation. For every $10,000 in student loans, he says that will generally equate to a $100 monthly payment. -- Tomorrow, Vision attendees will be treated to more breakout sessions and a concluding keynote with legendary quarterback Tom Brady.

So many insights and learnings to report after the first full day of 2017 Vision sessions. From the musings shared by tech engineer and pioneer Steve Wozniak, to a panel of technology thought leaders, to countless breakout sessions on a wide array of business topics … here’s a look at our top 10 from the day. A mortgage process for the digital age. At last. In his opening remarks, Experian President of Credit Services Alex Lintner asked the audience to imagine a world when applying for a mortgage simply required a few clicks or swipes. Instead of being sent home to collect a hundred pieces of paper to verify employment, income and assets, a consumer could click on a link and provide a few credentials to verify everything digitally. Finally, lenders can make this a reality, and soon it will be the only way consumers expect to go through the mortgage process. The global and U.S. economies are stable. In fact, they are strong. As Experian Vice President of Analytics Michele Raneri notes, “the fundamentals and technicals look really solid across the countries.” While many were worried a year ago that Brexit would turn the economy upside down, it appears everything is good. Consumer confidence is high. The Dow Jones Index is high. The U.S. unemployment rate is at 4.7%. Home prices are up year-over-year. While there has been a great deal of change in the world – politically and beyond – the economy is holding strong. The rise of the micropreneur. This term is not officially in the dictionary … but it will be. What is it? A micropreneur is a business with 0 to 4 employees bringing in no more than $200k in annual revenue. But the real story is that numbers show microbusiness are improving on many fronts when it comes to contribution to the economy and overall performance compared to other small businesses. Keep an eye on these budding business people. Fraud is running fierce. Synthetic identity losses are estimated in the hundreds of millions annually, with 50% year-over year growth. Criminals are now trying to use credit cleaners to get tradelines removed from used Synthetic IDs. Oh, and it is essential for businesses to ready themselves for “Dark Web” threats. Experts advise to harden your defenses (and play offense) to keep pace with the criminal underground. As soon as you think you’ve protected everything, the criminals will find a gap. The cloud is cool and so are APIs. A panel of thought leaders took to the main stage to discuss the latest trends in tech. Experian Global CIO Barry Libenson said, “The cloud has changed the way we deliver services to our customers and clients, making it seamless and elastic.” Combine that with API, and the goal is to ultimately make all Experian data available to its customers. Experian President of Decision Analytics Steve Platt added, “We are enabling you to tap into what you need, when you need it.” No need to “rip and replace” all your tech. Expect more regulation – and less. A panel of regulatory experts addressed the fast-changing regulatory environment. With the new Trump administration settling in, and calls for change to Dodd-Frank and the Consumer Financial Protection Bureau (CFPB), it’s too soon to tell what will unfold in 2017. CFPB Director Richard Cordray may be making a run for governor of Ohio, so he could be transitioning out sooner than the scheduled close of his July 2018 term. The auto market continues to cruise. Experian’s auto expert, Malinda Zabritski, revealed the latest and greatest stats pertaining to the auto market. A few numbers to blow your mind … U.S. passenger cars and light trucks surpassed 17 million units for the second consecutive year Most new vehicle buyers in the U.S. are 45 years of age or older Crossover and sport utility vehicles remain popular, accounting for 40% of the market in 2016 – this is also driving up finance payments since these vehicles are more expensive. There are signs the auto market is beginning to soften, but interest rates are still low, and leasing is hot. Defining alternative data. As more in the industry discuss the need for alternative data to decision, it often gets labeled as something radical. But in reality, alternative data should be simple. Experian Sr. Director of Government Affairs Liz Oesterle defined it as “getting more financial data in the system that is predicted, validated and can be disputed.” #DeathtoPasswords – could it be a reality? It’s no secret we live in a digital world where we are increasingly relying on apps and websites to manage our lives, but let’s throw out some numbers to quantify the shift. In 2013, the average U.S. consumer had 26 online accounts. By 2015, that number increased to 118 online accounts. By 2020, the average person will have 207 online accounts. When you think about this number, and the passwords associated with these accounts, it is clear a change needs to be made to managing our lives online. Experian Vice President David Britton addressed his session, introducing the concept of creating an “ultimate consumer identity profile,” where multi-source data will be brought together to identify someone. It’s coming, and all of us managing dozens of passwords can’t wait. “The Woz.” I guess you needed to be there, but let’s just say he was honest, opinionated and notes that while he loves tech, he loves it even more when it enables us to live in the “human world.” Too much wonderful content to share, but more to come tomorrow …

In a May 4 speech before the ACA International Conference in Washington, FCC Commissioner Michael O’Rielly criticized the FCC’s past decisions on Telephone Consumer Protection Act (TCPA) and outlined his vision on the direction that the new Commission should head to provide more certainty to businesses. Commissioner O’Rielly noted that prior decisions by the FCC and courts have “expanded the boundaries of TCPA far beyond what I believe Congress intended.” He said that the new leadership at the Commission and a new Bureau head overseeing TCPA, provides the FCC with the opportunity to “undo the misguided and harmful TCPA decisions of the past that exposed legitimate companies to massive legal liability without actually protecting consumers.” O’Rielly laid out three principles that he thought would help to frame discussions and guide the development of replacement rules. First, he said that legitimate businesses need to be able to contact consumers to communicate information that they want, need or expect to receive. This includes relief for informational calls, as well as valid telemarketing calls or texts. Second, Commissioner O’Rielly said that FCC should change the definition of an autodialer so that valid callers can operate in an efficient manner. He went on to say that if FCC develops new rules to clarify revocation of consent, it should do so in a clear and convenient way for consumers, but also does not upend standard best practices of legitimate companies. Third, O’Rielly said that the FCC should focus on actual harms and bad actors, not legitimate companies. While Commissioner O’Rielly’ s comments signal his approach to TCPA reform, it is important to note that FCC action on the issue us unlikely to happen overnight. A rule must be considered by the Commission, which will have to allow for public notice and comment. Experian will continue to monitor regulatory and legislative developments on TCPA.

It should come as no surprise that reaching consumers on past-due accounts by traditional dialing methods is increasingly ineffective. The new alternative, of course, is to leverage digital channels to reach and collect on debts. The Past: Dialing for dollars. Let’s take a walk down memory lane, shall we? The collection approach used for many years was to initially send the consumer a collection letter recapping the obligation and requesting payment, usually when an account was 30 days late. If the consumer failed to respond, a series of dialing attempts were then made, trying to reach the consumer and resolve the debt. Unfortunately, this approach has become less effective through the years due to several reasons: The use of traditional landlines continues to drop as consumers shift to cell and Voice Over Internet Protocol (VOIP) services. The cost of reaching consumers by cell is more costly since predictive dialers can’t be used without prior consent, and the obtaining and maintaining consent presents its own set of tricky challenges. Consumers simply aren’t answering their phones. If they think a bill collector is calling, they don’t pick up. It’s that simple. In fact, here is a breakdown by age group that Gallup published in 2015, highlighting the weakness of traditional phone-dialing. The Present: Hello payment portal. With the ability to get the consumer on the phone to negotiate a payment on the wane, the logical next step is to go digital and use the Internet or text messaging to reach the consumer. With 71 percent of consumers now using smartphones and virtually everyone having an Internet connection, this can be a cost-effective approach. Some companies have already implemented an electronic payment portal whereby a consumer can make a payment using his or her PC or smartphone. Usually this is prompted by a collection letter, or if permitted by consumer consent, a text message to their smartphone. The Future: Virtual negotiation. But what if the consumer wants to negotiate different terms or payment plans? What if they want to try and settle for less than the full amount? In the past – and for most companies operating today – this translates into a series of emails or letters being exchanged, or the consumer must actually speak to a debt collector on the phone. And let’s be honest, the consumer generally does not want to speak to a collector on the phone. Fortunately, there is a new technology involving a virtual negotiator approach coming into the market now. It works like this: The credit grantor or agency contacts the consumer by letter, email, or text reminding them of their debt and offering them a link to visit a website to negotiate their debt without a human being involved. The consumer logs onto the site, negotiates with the site and hopefully comes to terms with what is an acceptable payment plan and amount. In advance, the site would have been fed the terms by which the virtual negotiator would have been allowed to use. Finally, the consumer provides his payment information, receives back a recap of what he has agreed to and the process is complete. This is the future of collections, especially when you consider the younger generations rarely wanting to talk on the phone. They want to handle the majority of their matters digitally, on their own terms and at their own preferred times. The collections process can obviously be uncomfortable, but the thought is the virtual negotiator approach will make it less burdensome and more consumer-friendly. Learn more about virtual negotiation.

Our recent Webinar looked at the current state of e-commerce fraud, and what to prepare for in the coming year