Latest Posts

FinCEN and email-compromise fraud sheds additional light on the threats of Email Account Compromise and Business Email Compromise.

In order to compete for consumers and to enable lender growth, creating operational efficiencies such as automated decisioning is a must. Unfortunately, somewhere along the way, automated decisioning unfairly earned a reputation for being difficult to implement, expensive and time consuming. But don’t let that discourage you from experiencing its benefits. Let’s take a look at the most popular myths about auto decisioning. Myth #1: Our system isn’t coded. If your system is already calling out for Experian credit reporting data, a very simple change in the inquiry logic will allow your system to access Decisioning as a ServiceSM. Myth #2: We don’t have enough IT resources. Decisioning is typically hosted and embedded within an existing software that most credit unions currently use – thus eliminating or minimizing the need for IT. A good system will allow configuration changes at any time by a business administrator and should not require assistance from a host of IT staff, so the demand on IT resources should decrease. Decisioning as a Service solutions are designed to be user friendly to shorten the learning curve and implementation time. Myth #3: It’s too expensive. Sure, there are highly customized products out there that come with hefty price tags, but there are also automated solutions available that suit your budget. Configuring a product to meet your needs and leaving off any extra bells and whistles that aren’t useful to your organization will help you stick to your allotted budget. Myth #4: Low ROI. Oh contraire…Clients can realize significant return-on-investment with automated decisioning by booking more accounts … 10 percent increase or more in booked accounts is typical. Even more, clients typically realize a 10 percent reduction in bad debt and manual review costs, respectively. Simply estimating the value of each of these things can help populate an ROI for the solution. Myth #5: The timeline to implement is too long. It’s true, automation can involve a lot of functions and tasks – especially if you take it on yourself. By calling out to a hosted environment, Experian’s Decisioning as a Service can take as few as six weeks to implement since it simply augments a current system and does not replace a large piece of software. Myth #6: Manual decisions give a better member experience. Actually, manual decisions are made by people with their own points of view, who have good days and bad days and let recent experiences affect new decisions. Automated decisioning returns a consistent response, every time. Regulators love this! Myth #7: We don’t use Experian data. Experian’s Decisioning as a Service is data agnostic and has the ability to call out to many third-party data sources and configure them to be used in decisioning. --- These myth busters make a great case for implementing automated decisioning in your loan origination system instead of a reason to avoid it. Learn more about Decisioning as a Service and how it can be leveraged to either augment or overhaul your current decisioning platforms.

personalized subject lines have a 27% higher unique click rate, an 11% higher CTO and more than double the transaction of other promotional mailings

Panel discussion on Reinventing Identity for the Digital Age at Electronic Signature & Records Association (ESRA) conference

Under the updated requirements for Customer Due Diligence, financial institutions must expand programs.

More lenders are turning to VantageScore® to help achieve their goals and reduce risk

For members of the U.S. military, relocating often, returning home following a lengthy deployment and living with uncertainty isn’t easy. It can take an emotional and financial toll, and many are unprepared for their economic reality after they separate from the military. As we honor those who have served our country this Veterans Day, we are highlighting some of the special financial benefits and safeguards available to help veterans. Housing Help One of the best benefits offered to service members is the Veteran’s Administration (VA) home-loan program. Loan rates are competitive, and the VA guarantees up to 25 percent of the payment on the loan, making it one of the only ways available to buy a home with no down payment and no private mortgage insurance. Debt Relief Having a VA loan qualifies military members for a Military Debt Consolidation Loan (MDCL) that can help with overcoming financial difficulties. The MDCL is similar to a debt consolidation loan: take out one loan to pay off all unsecured debts, such as credit cards, medical bills and payday loans, and make a single payment to one lender. The advantage of a MDCL? Paying a lower interest rate and closing costs than civilians and far less interest than paying the same bills with credit cards. These refinancing loans can be spread out over 10, 15 and sometimes 30 years. Education Benefits The GI Bill is arguably the best benefit for veterans and members of the armed forces. It helps service members pay for higher education for themselves and their dependents, and is one of the top reasons people enlist. Eligible service members receive up to 36 months of education benefits, based on the type of training, length of service, college fund availability and whether he or she contributed to a buy-up program while on active duty. Benefits last up to 10 years, but the time limit may be extended. Saving & Investing Money According to the Department of Defense’s annual Demographics Report, 87 percent of military families contribute to a retirement account. Service members who participated in the Thrift Savings Plan, however, are often unaware of their options after they separate from service, and many don’t realize the advantages of rolling their plans into an IRA or retirement plan of a new employer. Safeguarding Identity Everyone is a potential identity theft target, but military personnel and veterans are particularly vulnerable. Routinely reviewing a credit report is one way to detect a breach. The Attorney General's Office provides general information about what steps to take to recover from identify theft or fraud. Today is a great time to consider ways to support your veteran and active military consumers. They are deserving of our support and recognition not just today but continuously. Learn more about services for veterans and active military to understand the varying protections, and how financial institutions can best support military credit consumers and their families.

Experian is recognized as a leading security solution provider for fraud and identity solutions in order to protect customers and financial institutions

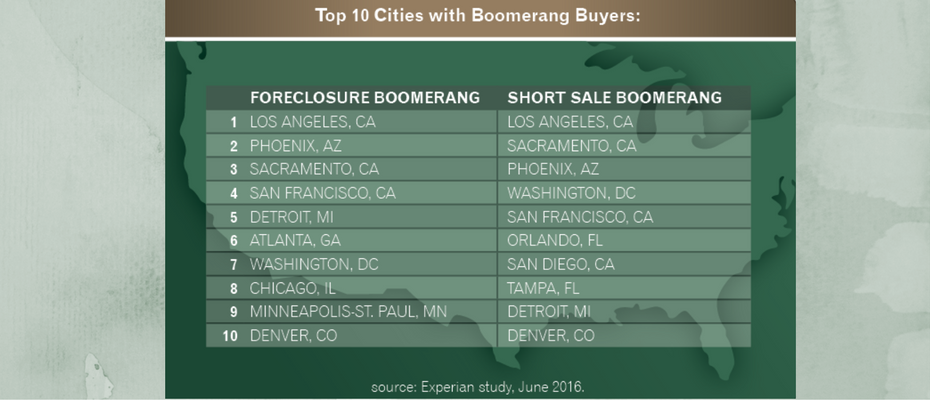

Experian analysis shows that 2.5M consumers will have a foreclosure, short sale or bankruptcy fall off their credit report between June 2016 and June 2017

The mortgage meltdown and Great Recession have translated into big shifts as it relates to financial services regulations. What's to come with a new administration coming soon?

The healthcare sector has been a hotbed of attacks due to the continued value of medical records sold on the dark web.

Experian announces partnership with U.S. Communities to help state and local public agencies prevent fraud, maximize revenue, strengthen security

$1.3 trillion. 41.1 million Americans. $31,590. These are the growing numbers associated with student loan debt in the United States: $1.3 trillion in outstanding student loans, spread across 41.1 million people, who are leaving college with an average balance of $31,590. The numbers are staggering, and for the first time student loan debt is playing a prominent role in a presidential election. For all of their differences, presidential nominees Hillary Clinton and Donald Trump seem to agree on one thing: student loan debt is a crushing burden. Both candidates have proposed solutions for student lending. Clinton’s “New College Compact” would allow borrowers to refinance their student loans at current rates available to students taking out new loans. She also wants to reduce interest rates on new student loans, and make it easier for borrowers to enroll in income-driven repayment programs that would cap monthly payments at 10 percent of discretionary income. Trump proposes giving more oversight to colleges to decide whether to grant loans to students based on their prospective major. The plan would also give private banks oversight over government-backed student loans—reversing a 2010 decision under President Obama to make the federal government the lender. Neither candidate, however, has outlined a solution for taming growing tuition costs. Tuition expenses are up 1,225 percent over the past 36 years, outpacing medical costs (634 percent rise) and the consumer price index (279 percent) over the same period, according to the Bureau of Labor Statistics. So it’s not surprising an Experian study shows the student loan rate has grown five percent in the past three years. What is surprising is the number of people and the average age of those people holding student loans. Experian found: 20 percent of people with a credit file hold a student loan that is being repaid or deferred. The average age of a consumer with a student loan is 37, with an average income of $47,200 compared to 53.8 and an average income is $44,500 for consumers without a student loan. The average age of a consumer with at least one deferred student loan is 32.7 with an average income of $32,900 compared to 38.7 and an average income of $53,200 for consumers with at least one non-deferred student loan. Candidate proposals aside, one thing is certain: student loan debt has a very real impact on the daily lives of people, many of whom have delayed buying homes, starting families, and saving for retirement. Until policymakers find a way to address bloated tuitions and student debt, it will take many longer to realize their dreams.

Reduce your TCPA compliance risk; Follow these steps when creating your dialing strategy

Businesses believe that 23% of their customer or prospect data is inaccurate.