Tag: identity theft

How can fintech companies ensure they’re one step ahead of fraudsters? Kathleen Peters discusses how fintechs can prepare for success in fraud prevention.

Recognizing customers is more than good service. Identify your customers to spot fraud. It’s a simple concept, but it’s not so simple to do. Consumers expect to be recognized and welcomed wherever and whenever they do business. Here's more insights on recognition and fraud.

Cybersecurity has become one of the most significant issues impacting international security and political and economic stability. Our new report, Data Breach Industry Forecast 2018, outlines 5 predictions for the data breach industry in the coming year.

Traditional verification and validation parameters alone are not enough to stop identity fraud. Fortunately, there are many emerging trends and best practices for modern fraud and identity strategies:

Sophisticated criminals work hard to create convincing, verifiable personas they can use to commit fraud. Here are the 3 main ways fraudsters manufacture synthetic IDs:

Despite rising concerns about identity theft, most Americans aren’t taking basic steps to make it harder for their information to be stolen, according to a survey Experian conducted in August 2017.

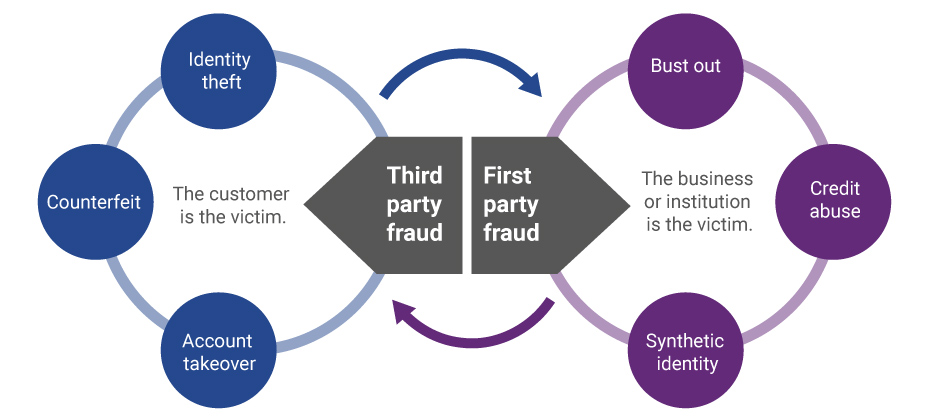

Third-party and first-party schemes are now interchangeable, and traditional fraud detection practices are less effective in fighting these evolving fraud types.

An Experian survey shows that many consumers still seriously underestimate their risk of falling victim to identity theft.

A synthetic identity epidemic is impacting all markets. Here are the three ways that synthetic identities are generally created

With the recent switch to EMV and more than 4.2 billion records exposed by data breaches last year, attackers are migrating to the CNP channel.

New research from the Pew Data Center, regarding how much Americans know about cybersecurity

Florida, Delaware, Oregon and New York were the riskiest states for e-commerce fraud

Adoption of EMV has pressured attackers to migrate fraud to the CNP channel. This is a major driver to the increase in e-commerce fraud attacks.

We’re excited to announce Family Account Management: a new feature that makes it easy to extend identity protection to family and friends.

Internet-connected devices provide endless possibilities, but they rely on technology and collected data to deliver on their promises.