Uncategorized

It’s one of our favorite times of year. Yes, spring is in the air, and we’re delighted to spend a few days away from the office in picturesque Scottsdale, Arizona. But what really has us excited is the opportunity to connect with a diverse network of industry leaders from across the country at our 35th annual Vision Conference. We have a full agenda, featuring sessions on advanced data analytics, market trends, fraud and identity, regulatory hot topics and more. And our theme for this year is geared toward giving participants the tools and insights they need to take control of their respective businesses to grow new markets, increase existing customer bases, reduce fraud and increase profits. In addition to 70-plus breakout session, guests will be treated to several keynote addresses: Leon Panetta, former U.S. Secretary of defense and former Director of the CIA James W. Paulsen, Chief Investment Strategist, Wells Capital Management Jay Leno, Television Host, Author and Comedian Listen to Experian North America CEO Craig Boundy’s welcome message, and start your Vision three-day event with the goal of meeting and engaging with as many old and new contacts as possible. For individuals not attending this year’s Vision, stay tuned for learnings and insights that will be shared in the coming weeks. Attendees and non-attendees alike can also follow updates on Twitter and via #vision2016.

Fraudsters combine and manipulate real consumer data with fictitious demographic information to create a “new” or “synthetic” identities.

Businesses are looking to international markets to fuel growth, but meeting regulatory requirements across the globe poses significant challenges. Changes in Anti-Money Laundering (AML) and Know Your Customer (KYC) requirements are evolving at break-neck speed. In the past few years, financial institutions and corporations have incurred billions of dollars in fines, reputation damage, and even the possibility of criminal prosecution for not enforcing adequate regulatory controls. KPMG found that 70 percent of its respondents had received a regulatory visit within the past year focused on KYC and total investment in AML had increased by an average rate of 53 percent. As large as this additional investment may seem, there may be an even bigger cost to doing regulatory compliance the right way. For many businesses the customer experience is the biggest casualty of implementing a robust KYC program. In their Vision 2016 breakout session “Know your customer, meeting commercial requirements in a global marketplace,” Greg Carmean, Experian senior product manager, will be joined by Adel Shrufi, software development manager at Amazon Transaction Risk Management Systems. They will discuss: • How to streamline compliance to optimize the client experience • How to evaluate and select the best vendors to reduce compliance costs and operational vulnerabilities • What businesses need to consider to ensure successful launches in new international markets Watch our session preview video below: We’ll look forward to seeing you as we provide a road map for growth at this year’s Vision conference.

Device emulators are devices that pretend to be another. Innovative technology used for site testing for Web developers, attackers use to wreak havoc across industries

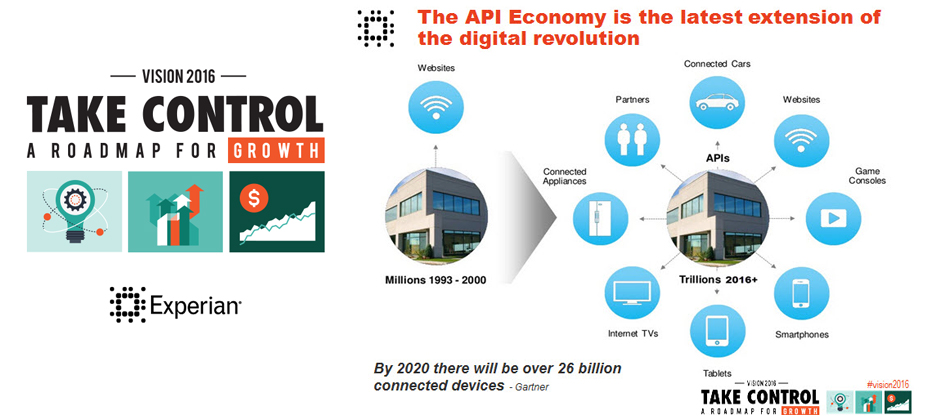

There is a revolution going on! We are in the midst of the second phase of the digital revolution and it is being fueled by API’s. API’s provide the access and mapping that allow access to and integration of the myriad of existing and new data sources available today. They do really helpful things like allow Uber to revolutionize the connection of riders to drivers as well as allow for quick, self-service credit decisions by integrating Experian data within Salesforce.com. Digital disruptors like Uber have scaled their business to massive size at breakneck speed because they can design, build and deploy solutions quickly. API’s and cloud computing play a central role in all of this. You will hear representatives from Uber share how API’s enabled the flow of Experian data through Salesforce.com enabling them to launch new business models, and enter new markets. Listen to Mike Myers as he shares a short overview of his Vision 2016 breakout session in this short video. Don’t miss this innovative Vision 2016 session! See you there.

Small business trade payment delinquencies can signal the beginning of business financial duress. However, sometimes these delinquencies are isolated events. Understanding the trade payment priorities of a business can lead to better business risk assessment. Experian understands commercial payment behaviors and can help clients more accurately interpret the risk of payment delinquencies for different kinds of trades. In his Vision 2016 breakout session “Which creditors get priority when businesses face a financial burden”, Sung Park, Analytics Consultant with Experian’s Decision Sciences discusses the types of trades or financial obligations that become delinquent first, and the conditions that most commonly signal overall business stress. What the audience will learn: The audience will have a better understanding of which type of trade delinquencies are likely isolated incidents and which ones are precursors of businesses facing a financial burden, and what actions can be taken proactively to mitigate risk. Don't miss your opportunity to catch these informative breakout sessions during Vision 2016.

Identity management traditionally has been made up of creating rigid verification processes that are applied to any access scenario. But the market is evolving and requiring an enhanced Identity Relationship Management strategy and framework. Simply knowing who a person is at one point in time is not enough. The need exists to identify risks associated with the entire identity profile, including devices, and the context in which consumers interact with businesses, as well as to manage those risks throughout the consumer journey. The reasoning for this evolution in identity management is threefold: size and scope, flexible credentialing and adaptable verification. First, deploying a heavy identity and credentialing process across all access scenarios is unnecessarily costly for an organization. While stringent verification is necessary to protect highly sensitive information, it may not be cost-effective to protect less-valuable data with the same means. A user shouldn’t have to go through an extensive and, in some cases, invasive form of identity verification just to access basic information. Second, high-friction verification processes can impede users from accessing services. Consumers do not want to consistently answer multiple, intrusive questions in order to access basic information. Similarly, asking for personal information that already may have been compromised elsewhere limits the effectiveness of the process and the perceived strength in the protection. Finally, an inflexible verification process for all users will detract from a successful customer relationship. It is imperative to evolve your security interactions as confidence and routines are built. Otherwise, you risk severing trust and making your organization appear detached from consumer needs and preferences. This can be used across all types of organizations — from government agencies and online retailers to financial institutions. Identity Relationship Management has three unique functions delivered across the Customer Life Cycle: Identity proofing Authentication Identity management Join me at Vision 2016 for a deeper analysis of Identity Relationship Management and how clients can benefit from these new capabilities to manage risk throughout the Customer Life Cycle. I look forward to seeing you there!

Tax return fraud occurs when an attacker uses a consumer’s stolen SSN and other information to file a tax return, often claiming a significant refund.

Loyalty fraud occurs when criminals obtain login credentials (either through breach, malware, phishing, etc.) and use your profile to purchase goods.

Large number of HELOC loans will soon be entering their HELOC end of draw period, giving lenders an opportunity for new finance options

Increased volume of fraud attempts during back to school shopping season. Is your fraud strategy prepared to handle the increased volume?

Protect consumers on summer vacation fraud. Evidence shows fraudster activity increases during the summer and identity theft becomes easier.

I have heard from a few creditors that when it comes to allocating accounts to collection agencies for recoveries creating a rule based strategy isn’t always in the cards. When clients use multiple collection agencies their ability to allocate accounts to the different agencies based on rule based strategies isn’t always available. Some have a single setting on a billing or assignment system that indicates the account is to be assigned to Collection Agency X versus Collection Agency Y, and there is no easy method to make that assignment based on a true strategy. Worse yet, it is often difficult to impossible to reassign that account from Collection Agency X to Collection Agency Y if the account status or risk level changes. This means that their use of multiple collection agencies is not as “optimized” as it could be if a scripting or rule based tool was available to the business user. Optimizing assignments means that the account is initially as well as subsequently assigned to the right agency at the right time based on its type, risk, history, balance, status and other circumstances to maximum recoveries. This approach can make a significant difference in the recovery of bad debt. Furthermore, test results or allocations should be displayed after a script has been entered. This usually provides a “what if” on collection agency assignments displaying the number or dollar value assigned if the rule was implemented. That way you know if the script is correct (ballpark allocation seems reasonable), and if the allocation to any particular agency is within policy limits by dollar amount or number of accounts. Do you believe that you are optimizating your allocations to the agencies you use? Do you have the tools you need to effectively assign each account to the right agency? Experian can help with its agency allocation and management solutions through Tallyman Agency Allocation. Learn more about our Tallyman Agency Allocation software.

Real-time alerts help consumers monitor their identity, businesses engage with customers

UncategorizedBy: Reggie Whitley After spending years working in bank fraud, one of the most difficult conversations to have with a consumer is “We can no longer successfully protect your accounts.” Identity theft is shockingly easy to commit. In most cases consumers are able to recover successfully from compromises thanks to the diligence of their financial institutions, the cooperation of retailers, and credit reporting services that assist in recovery from compromises. Problems arise when you have consumers who become attractive targets for various reasons – these could be relationships to others, high net worth, extensive products, or business ownership. These targets aren’t ‘one and done’ consumers for an identity criminal. For these consumers identity thieves will continue accessing their identities for months or even years. These consumers are often forced to migrate from banks or credit card companies because the identity crimes follow them and they become too expensive to protect. For these consumers, identity theft is a true nightmare. In the past year, fraud protection strategies and tools have emerged that will begin to reduce the risk of continued compromise these consumers face. Real time identity alerting tools have emerged to offer consumers a way to receive notification when their identities are being used, not just at a single institution, but across the financial landscape. Consumers now have the ability to receive SMS, Email, or Web notifications whenever their identity has been verified. If the consumer receives an alert on an banking account they just opened, they simply move on, no action is required. In the event that the alert is NOT something they generated, the consumer calls in, discusses with a fraud specialist and is connected to the generating bank or retailer to file a fraud report. Obviously, this service benefits any consumer who would like to monitor usage of their identity and detect fraud, but knowing first hand the horror stories extensively compromised consumers get caught in, tools like start to open a level of REAL TIME protection that hasn’t before existed. The benefit is truly across the board. Banks and retailers begin to realize savings when consumers engage them within minutes of fraud. This reduces the success of identity thieves, discouraging additional attempts. Finally, detecting this fraud reduces the extensive efforts needed to help a consumer clear up credit reports and file fraud reports. Perhaps in the near future instead of turning high risk consumers away, we can provide them with the ability to protect themselves and the industry from the nightmare situations that are still too frequent today.

The desire to return to portfolio growth is a clear trend in mature credit markets, such as the US and Canada. Historically, credit unions and banks have driven portfolio growth with aggressive out-bound marketing offers designed to attract new customers and members through loan acquisitions. These offers were typically aligned to a particular product with no strategy alignment between multiple divisions within the organization. Further, when existing customers submitted a new request for credit, they were treated the same as incoming new customers with no reference to the overall value of the existing relationship. Today, however, financial institutions are looking to create more value from existing customer relationships to drive sustained portfolio growth by increasing customer retention, loyalty and wallet share. Let’s consider this idea further. By identifying the needs of existing customers and matching them to individual credit risk and affordability, effective cross-sell strategies that link the needs of the individual to risk and affordability can ensure that portfolio growth can be achieved while simultaneously increasing customer satisfaction and promoting loyalty. The need to optimize customer touch-points and provide the best possible customer experience is paramount to future performance, as measured by market share and long-term customer profitability. By also responding rapidly to changing customer credit needs, you can further build trust, increase wallet share and profitably grow your loan portfolios. In the simplest sense, the more of your products a customer uses, the less likely the customer is to leave you for the competition. With these objectives in mind, financial organizations are turning towards the practice of setting holistic, customer-level credit lending parameters. These parameters often referred to as umbrella, or customer lending, limits. The challenges Although the benefits for enhancing existing relationships are clear, there are a number of challenges that bear to mind some important questions to consider: · How do you balance the competing objectives of portfolio loan growth while managing future losses? · How do you know how much your customer can afford? · How do you ensure that customers have access to the products they need when they need them · What is the appropriate communication method to position the offer? Few credit unions or banks have lending strategies that differentiate between new and existing customers. In the most cases, new credit requests are processed identically for both customer groups. The problem with this approach is that it fails to capture and use the power of existing customer data, which will inevitably lead to suboptimal decisions. Similarly, financial institutions frequently provide inconsistent lending messages to their clients. The following scenarios can potentially arise when institutions fail to look across all relationships to support their core lending and collections processes: 1. Customer is refused for additional credit on the facility of their choice, whilst simultaneously offered an increase in their credit line on another. 2. Customer is extended credit on a new facility whilst being seriously delinquent on another. 3. Customer receives marketing solicitation for three different products from the same institution, in the same week, through three different channels. Essentials for customer lending limits and successful cross-selling By evaluating existing customers on a periodic (monthly) basis, financial institutions can assess holistically the customer’s existing exposure, risk and affordability. By setting customer level lending limits in accordance with these parameters, core lending processes can be rendered more efficient, with superior results and enhanced customer satisfaction. This approach can be extended to consider a fast-track application process for existing relationships with high value, low risk customers. Traditionally, business processes have not identified loan applications from such individuals to provide preferential treatment. The core fundamentals of the approach necessary for the setting of holistic customer lending (umbrella) limits include: · The accurate evaluation of credit and default risk · The calculation of additional lending capacity and affordability · Appropriate product offerings for cross-sell · Operational deployment Follow my blog series over the next few months as we explore the essentials for customer lending limits and successful cross-selling.