Featured

Featured

Early in my career, I gained a lot of knowledge about credit. But when I moved to the United States from Brazil, establishing credit was a challenge. I worked part-time in a credit card company call center during college. I come from a humble family, and through helping customers, I learned the ins and outs about credit and money management. But all the solid credit history I built up in my home country didn’t transfer to the U.S. When I immigrated, I had to pay upfront for everything from utilities to a cellphone and it made me feel at a disadvantage. Thanks to Experian Boost®i, our feature that allows you to build credit without debt, and responsible management of debt, my FICO® Scoreii quickly rose to reflect my true creditworthiness. But I’ll never forget how it felt to be invisible when it came to the credit system. Being seen is the first step to equitable access to financial tools. Now that Experian conveniently offers Experian credit reports in Spanish onlineiii, consumers who prefer to access information in Spanish will be able to directly comprehend their credit profile so they can feel empowered. Understanding your credit report is a critical component for your ability to make informed decisions about your finances. As the executive sponsor of our Juntos Employee Resource Group (ERG) and someone who was new to credit in the U.S., I know first-hand that being seen is the first step in a journey towards financial wellness. To help you be informed, Experian also has a Spanish-language credit e-book and articles at the Ask Experian blog. Learn more about my financial health journey and my colleague's through #ExperianStories. i Results will vary. Not all payments are boost-eligible. Some users may not receive an improved score or approval odds. Not all lenders use Experian credit files, and not all lenders use scores impacted by Experian Boost®. Learn more. ii Credit score calculated based on FICO® Score 8 model. Your lender or insurer may use a different FICO® Score than FICO® Score 8, or another type of credit score altogether. Learn more. iii Only Experian credit reports are available in Spanish. All other services associated with an Experian membership are available in English only. English fluency is required for full access to Experian’s products.

Ball pits, a video game and a neon-pink house might not be what typically comes to mind when you think of our mission of financial inclusion. But that’s some of the ways Experian spent its summer sharing resources and information to empower underserved communities. FINANCIAL INCLUSION AND INNOVATION The mild weather ushered-in summer early in the City of Brotherly Love, where we joined the Allen Iverson Roundball Classic to launch B.A.L.L. (Be A Legacy Leader) for Life. It was our second year as the exclusive financial literacy partner. In partnership with the National Urban League, we introduced this program to the athletes and their families participating in the all-star weekend. We also created a gamified app that enables users to shoot hoops using gesture controls as they learn about credit and financial tools. Experian’s partnership with UnidosUS includes support for its Financial Empowerment Network (FEN), a program, which offers free, individualized, culturally-relevant support to Latino families. Our colleagues shared credit education resources and their journeys to financial health at the national conference. We are… financially fierce! As a proud sustaining Titanium partner of Out & Equal, we brought The House of Experian to this year’s Workplace Summit. Hundreds visited the eye-catching attraction to learn about financial and credit tools. We also led engaging conversations about money matters for the trans community and dove deep into the financial wellness of LGBTQ+ consumers and entrepreneurs. To learn more about the gaps and needs of the community, we’ve launched a financial wellness survey in partnership with Out & Equal. COMMUNITY ADVOCACY The mental health and wellness of our teammates is a priority for Experian, and it was a big topic of panel discussions at the Disability:IN Annual Conference. Empowering Asian American and Pacific Islander (AAPI) professionals is the focus of the annual Ascend Leadership Convention. This year’s theme was “I Ascend,” encouraging participants to share how they navigate and succeed in their careers. At Essence Fest’s National Urban League Women’s Empowerment Luncheon, Victoria Crain, Experian’s vice president of global compliance and governance and co-executive sponsor of our Black Professionals Employee Resource Group, shared keynote remarks about courage and legacy. EMPOWERING THE NEXT GENERATION Building paths towards generational wealth took center stage at the National Urban League Annual Conference. We led a conversation with multigenerational influencers and financial experts on money matters from personal and entrepreneurial lenses, and brought the B.A.L.L. for Life experience to the community. Our support for entrepreneurship extends to the Women of Color and Capital, where we were a returning sponsor and joined a discussion about financial solutions for small business owners. HomeFree-USA closed out our summer by honoring Experian with the 2023 Trailblazer Award and the 2023 CFA Partner of the Year Award. Our innovative program, launched in 2022 in partnership with the Center for Advancement (CFA), trained 250 scholars from Historically Black Colleges and Universities to become knowledge ambassadors about credit, and share what they’ve learned in the program with peers and family. Through events like these, we aim to normalize conversations about credit and make it easier for consumers to access the tools they need for their financial wellness. We are already looking forward to Summer 2024. To learn more about how Experian supports diverse communities, check out www.experian.com/deievents.

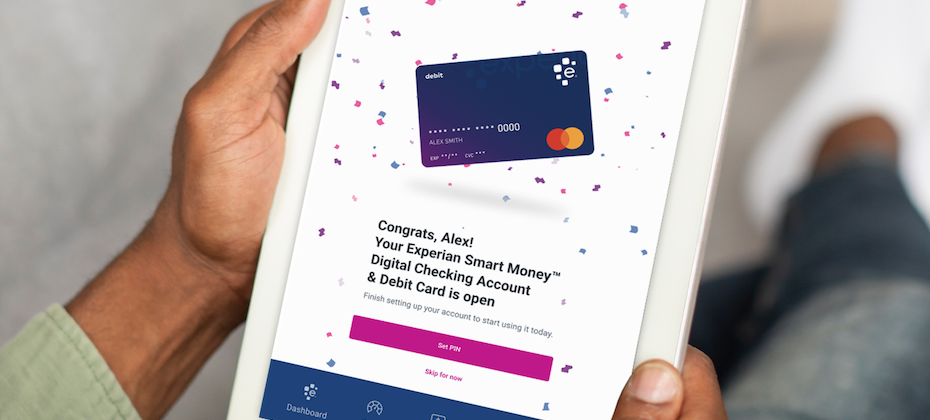

Our mission at Experian Consumer Services to achieve Financial Power for All™ drives our purpose and innovation. As part of this focus, we aim to help the more than 28 million1 consumers who are considered “credit invisible” with no or little credit history to gain fair and affordable access to credit. Continuing in our commitment to financially empower consumers, we are excited to announce today the launch of the Experian Smart Money™ Digital Checking Account & Debit Card2. What makes the Experian Smart Money Account unique is that it takes one of our most successful features ever in Experian Boost®3 to a new level of ease by embedding the feature in our new digital checking account. Experian Boost is a free game-changing feature launched in 2019 that allows consumers to contribute positive payments for eligible bills such as utilities and residential rent to their Experian® credit reports to potentially increase their credit scores. More than 14 million consumers have already connected to Experian Boost - via their existing checking account or credit card - with an average FICO® Score 84 increase of 13 points, among those who saw an increase. Now, the Experian Smart Money Account will drive efficiencies for consumers by allowing them to build credit more easily without debt and manage their day-to-day finances in one place. Helping consumers along their financial journeyWe understand that every consumer has different needs when it comes to their finances. When consumers engage with Experian, they can tap into many resources such as Experian Go™, which allows consumers to directly establish an Experian credit file for the first time and take off on their credit journey. For consumers who already have a credit profile and are looking to build their credit history and potentially increase their credit scores, they can leverage Experian Boost to contribute eligible payment history to their Experian credit file. Now with the Experian Smart Money Account, Experian is building upon these innovations and creating an even more robust credit and financial hub beneficial for various life stages. In fact, being credit visible and establishing a good credit score is essential for achieving many goals like moving into a new home, buying a car or securing employment. The positive impact we can have on consumers’ financial lives is what motivates us every day to create products and tools like the Experian Smart Money Account. Making ‘smart’ money movesWhile Experian is entering a different category of services, offering a digital checking account is a natural next step for us to help consumers reach their financial goals. The Experian Smart Money Account could most benefit consumers who are looking to build their credit profile. So, we believe our credit-building power makes this offering a positive complement to other financial products and services in the market. The Experian Smart Money™ Account accelerates, supports, and enriches consumer choice to build credit responsibly, which has a direct impact on the growth of credit-eligible populations. It benefits both consumers and broader financial institutions, and we are dedicated to playing a special role in the financial ecosystem helping consumers leverage debit and credit to their advantage. For more information about Experian Smart Money™ Account, visit www.experian.com/smartmoney. 1 Financial Inclusion and Access to Credit by Experian and Oliver Wyman, October 2021 2 The Experian Smart Money Debit Card™ is issued by Community Federal Savings Bank (CFSB), pursuant to a license from Mastercard International. Banking services provided by CFSB, Member FDIC. Experian is a Program Manager, not a bank. 3 Results will vary. Not all payments are boost-eligible. Some users may not receive an improved score or approval odds. Not all lenders use Experian credit files, and not all lenders use scores impacted by Experian Boost®. Learn more. 4 Credit score calculated based on FICO® Score 8 model. Your lender or insurer may use a different FICO® Score than FICO® Score 8, or another type of credit score altogether. Learn more.

At Experian we recognize our teammates are central to our business success. By including people with disabilities in our workplace, we gain their unique perspectives and different approaches to problem solving. Experian is committed to supporting this community and we are delighted to be named a 2023 Best Place to Work for Disability Inclusion by the American Association of People with Disabilities and Disability:IN. For the second year in a row, we earned a score of 100 out of 100 in the Disability Equality Index (DEI), the world’s most comprehensive benchmarking tool that measures disability workplace inclusion. We continue to explore and prioritize ways to enhance our flexible work environment and engage with those who can help lead the charge most effectively. Creating a better tomorrow extends to third parties we work with and serve. We launched a pilot program called the Support Hub, which gives disabled people and those with additional support needs an easy, one-stop portal to tell organizations what they need to access essential services; it also helps organizations meet their obligations to better identify and support vulnerable customers. We’re proud to partner with National Disability Institute to support its Financial Resilience Center that provides information and resources to help people with disabilities and chronic health conditions build their financial resilience, and with National Disability Institute and Disability:IN to explore how financial service providers can better support equal access to financial opportunities. Our inclusion in the DEI for the third consecutive year honors the determination, creativity, and empathy of our colleagues with disabilities as we strive to be a great place to work. Learn more about Experian in its Power of YOU: 2023 Diversity, Equity and Inclusion Report.

Many times during the course of our last fiscal year, Experian was asked to describe its Diversity, Equity and Inclusion (DEI) “program.” We found this difficult to do. Because DEI isn’t just a “program” at Experian. It drives our mission, our partnerships, and our company culture. We’re happy to share our progress in the Power of YOU: 2023 Diversity, Equity and Inclusion Report. In this edition of our global report, you’ll see how our mission of financial inclusion is at the center of our products and services; how we support our consumers, clients and communities; and how we seek and attract the best talent across the world. Our teammates are key to progress and impact. Together, we drive innovations to meet consumers’ needs, such as Experian Go and our new auto insurance comparison shopping service in North America. The Support Hub pilot in the United Kingdom helps disabled people get easier access to essential services like banking and utilities. We’re proud of programs like Transforme-se in Brazil for people in vulnerable circumstances, which provide scholarships and training in STEM. In the first month, more than half of the participants improved their social and financial standing. Across the globe, partnerships with nonprofits and non-governmental organizations (NGOs) have impacted more than 18 million people so far. I hope you’ll enjoy reading the report to understand why our efforts around inclusion and belonging make Experian such a great place to work. You’ll also gain an appreciation for our ongoing focus on supporting the communities in which we live, work, and serve, and helping consumers achieve their life goals.

Nearly 50 million consumers have a nonexistent or limited credit history. That is a major problem in need of a world-changing idea. Experian, in its ongoing efforts to promote financial equity and inclusion, introduced a new offering last year that directly addresses this problem: Experian Go™. This free program empowers “credit invisibles” to establish their financial identity within minutes. And it has already helped tens of thousands of consumers who are new to credit establish an Experian credit report, a critical first step to things like buying a car or renting an apartment. Now Experian Go has been recognized with the prestigious Fast Company 2023 World Changing Ideas Award for the company’s use of innovative technology to promote financial inclusion. Fast Company’s World Changing Ideas Award celebrates the most impactful and innovative ideas that have the “potential to drive true change.” The award seeks to elevate finished products and brave concepts that make the world better, with the goal of honoring ingenuity and fostering innovation. Experian Go addresses a crucial need by providing individuals with no credit history with the tools necessary to participate in the financial system and better manage their credit. Experian Go’s award follows last year’s recognition of Experian Boost®, a first-of-its-kind feature designed to help consumers improve their credit profile and thrive financially, in Fast Company’s 2022 World Changing Ideas Awards. Millions of people have connected to Experian Boost to improve their FICO® Score by reporting their on-time utility, telecom/phone, rent and video streaming service payments. By giving consumers control over their credit, they can make real, substantial progress in their financial health journey by getting “credit” for paying bills on time. The innovative solution tackles inequity and exclusion from the credit economy, enabling consumers to add positive payment history directly into their Experian credit file and potentially boost their FICO® Score instantly. At Experian, we believe that technology has the power to do many things, and changing the world is one of them. Experian Go is part of our mission to help provide financial inclusion for all, and we look forward to creating more innovative products that focus on helping people.

Experian research shows more than a quarter of Black and Hispanic consumers are invisible to the credit market, compared to 16% of Asian and White consumers. This is a significant gap that all of us can improve. At our North American headquarters, a group of young scholars took the lead on finding solutions. Four teams representing Historically Black Colleges and Universities (HBCUs) visited our campus and shared their creativity and personal stories with us in the finale of the inaugural #IYKYK Hackathon. The Hackathon was the culmination of a six-month Center for Financial Advancement® Credit Academy, created in partnership with HomeFree-USA. Through live sessions with Experian credit education experts and self-paced content, more than 250 scholars from 14 HBCUs learned about credit, financial tools, and how to build generational wealth through steps like homeownership. The teams from Alabama State University, Fisk University, Morgan State University and Shaw University made it to the finals and presented their ideas for the next best credit education program for their peers. Left to right, top to bottom: Fisk University, Morgan State University, Shaw University and Alabama State University In addition to their presentations, what was also impressive was the inclusivity in participation. Just at the finals alone, these student leaders represented six countries, eight different languages, the LGBTQ+ community, different faiths, and more. The “Credit Stingers” from Alabama State University took home the prize, a $40,000 scholarship for their idea of a gamified app called “Credit Rush.” In order to overcome obstacles, students watch a video or take a quiz about credit in order to advance to higher levels. Other features of “Credit Rush” include the “Hive,” a library of credit education materials, chat, daily calendar functions and more. The “Credit Stingers” from Alabama State University took home the prize, a $40,000 scholarship for their idea of a gamified app called “Credit Rush.” Many of the student leaders are already putting what they’ve learned into practice. They shared how they’ve been able to rent their own apartments for the first time, help their recently immigrated family members establish their credit identities, and make decisions that will help them eventually buy a home. They showed immense passion. They are committed to being knowledge ambassadors, sharing information about credit with their classmates, families and friends, making their communities the true winners of this program.

Our people play a vital role in innovating new ways to better serve our customers, developing new technologies that advance inclusion and financial growth for consumers while helping other team members along the way. Our purpose-driven culture is clearly changing the game. Recognized by Fortune as one of America’s Most Innovative Companies, we’re pioneering innovations to help consumers navigate the complicated road to financial freedom. First, there’s Experian Boost™, our innovative product that allows people to improve credit scores by adding payment records to their profiles of previously untracked expenses such as utilities, mobile phone payments and streaming services. And now we’ve created a way to get rent payment histories into credit reports as well. We also changed the game with our new Experian Go™ product that enables those with no credit history to create a credit report. This program opens the front door to the financial ecosystem for millions of consumers by helping them establish their financial identity and move from credit invisible to scoreable. These products are just a few examples of how our company culture embraces change and enables us to innovate. We focus on problems that need to be solved and put the energy and resources behind developing solutions that solve them. And the industry recognition continues, which represents a validation of the culture of innovation we’ve built, with feedback coming from our employees, customers, and other industry experts. Other wins include: The 2023 BIG Innovation Awards that recognized the company for delivering innovative products, such as Experian Go™, that help consumers thrive financially Experian Boost™ was selected for Fast Company’s 2022 World Changing Ideas Awards. We were named a Great Place to Work’s Best Workplaces for Parents in 2022 and Top 30 Employer for Working Families in 2022. These are merely steps in our journey. Stay tuned for what’s next.

We’re thrilled to announce that Experian North America has been recognized as a Top Workplace by the Orange County Register for the 10th consecutive year, with an additional “Excellence Award” for our work / life flexibility. This honor is a testament to our innovative employee culture, and keeping connected, engaged and energized as a hybrid workforce. This Orange County Register award recognition is based on the results of confidential employee surveys that assess the performance of hundreds of successful companies throughout our community. We recognize that our employees are the driving force behind our decade-long achievement as a Top Workplace. Our talented team is dedicated to both their own growth and pushing us forward, and we’re grateful for all they do to make Experian such a great place to work. Employee collaboration from our hackathons and company-wide product overviews have sparked remarkable innovations, such as Experian Go and Experian Boost. These products are especially helpful to members of diverse backgrounds and low-income households. Our Mental Health First-Aiders program is another example of employees coming together to support each other. Our commitment to creating a supportive, purpose-driven culture is reflected in multiple awards from authoritative sources such as Great Places to Work. Not only was Experian listed among the "Best Workplaces for Parents," we’re also honored to be included on their list of "Best Workplaces for Millennials." Additionally, we’re passionate about giving back to the communities in which we work and live. We take pride in our company’s numerous contributions to organizations focused on the well-being of people from a diverse array of backgrounds. From creating the Experian Volunteer Leadership Network to our financial support of community organizations such as Ascend, National Urban league, HomeFree-USA and the Pathways Forward Initiative, we’re dedicated to helping people in need. We believe all these factors have led to our success as a company and a desirable place for people to build thriving careers. We’re honored that leading organizations like the Orange County Register and Great Places to Work recognize our efforts to make the world a better place. We want to make sure that we continue to innovate; that our products and services are first-best-and-only in their respective industries; and that we take very good care of our constituents.