World

News about Experian from all over the globe:

We are delighted to celebrate Pride Month this June, and to mark the progress we are making to support our LGBTQ+ colleagues and communities around the world. A few of our milestones this year include: The addition of trans-inclusive healthcare to our UK and U.S. employee benefit packages. Receiving a Silver Award from Stonewall for our commitment to inclusion of LGBTQ people in the workplace. The continued use of our partnerships with Mermaids, Switchboard and Terrence Higgins Trust (THT) to provide resources, offer workshops and support campaigns that raise awareness of the discrimination faced by the community worldwide. Becoming a signatory of the Brazil Corporate Forum for LGBTQA+ companies. Participating in the first diverse talent recruitment fair organised by the Colombian LGBT Chamber of Commerce. Achieving a 100% rating on the Corporate Equality Index from the Human Rights Campaign Foundation in the U.S., and being designated a Best Place to Work for LGBTQ Equality for the fourth consecutive year. Providing a process to assist trans and non-binary consumers with name changes to their Experian credit reports. Throughout the month, employee groups across our regions are hosting events that support our LGBTQ+ employees in their careers, that educate and inform allyship inside our business, and which help accelerate our ambition of delivering tools and services that create better financial health in the community. And yet, while we celebrate, we recognise that the LGBTQ+ community still faces many forms of discrimination around the world. We will continue to look for opportunities to support our Experian colleagues and customers who identify as part of the LGBTQ+ community, and to listen to those with lived experiences, so that we can better understand the role we can play in creating a better tomorrow and a stronger organisation – for everyone.

Last year, while still in the grip of the effects of the pandemic, Experian North America continued to reinforce our core purpose and People First approach through creating a workplace culture of belonging, employee wellness and personal and professional growth. It’s especially rewarding that this commitment, along with our financial planning and consumer education resources, were highlighted in this year’s Fortune 100 Best Companies to Work For award recognition. For the third year in a row, Experian North America was named to the prestigious national list that honors the “100 Best companies that adapted to massive changes in the workplace by prioritizing employee well-being, inclusion, purpose, listening and care wherever their employees are.” To determine this year’s 100 Best list, Great Place to Work®, America’s largest ongoing annual workforce study, surveyed more than 870,000 employees and gathered data from companies representing more than 6.1 million employees. The survey enables employees to share confidential feedback about their organization’s culture and the employee experience. Great Place to Work cited that “Experian has expanded benefits to include fertility, surrogacy, and adoption coverage and enhanced its higher education financial planning resources. It’s also tackling workplace equity from the very start of the hiring process with an in-house tool called Lingo that identifies gender-biased language in job descriptions.” In addition, “Experian began to hold conferences for employees to discuss their personal struggles during the pandemic. Since then, the company has continued to improve wellness initiatives, while staying committed to flexibility around employee schedules.” “At Experian we’re especially proud of our purpose-driven culture, where all our people play a role in making a positive impact in the day-to-day lives of the consumers, clients and communities we serve. This includes taking care of each other, celebrating our individual differences, and delivering on our purpose to create a better tomorrow for people everywhere,” said Jennifer Schulz, Chief Executive Officer of Experian North America. “This recognition from Fortune reflects the very best Experian offers to all those we help, and I couldn’t be prouder of our people and the work we’re doing.” At Experian, we believe bringing together unique experiences, diverse backgrounds and individual differences creates a dynamic, innovative and inspiring workplace — one reflective of the clients and communities we serve around the globe. This is why it’s such an honor to be recognized alongside other outstanding brands on the Best 100 list that prioritize their employees. This recognition continues the momentum we’ve built in recent months with other industry accolades and awards. In February, Experian North America was named a “Best Place to Work for LGBTQ Equality” for the fourth year in a row in the Human Rights Campaign Foundation’s Corporate Equality Index 2022, receiving a perfect score in the foundation’s evaluation. Last year, Experian North America was named to the Fortune Best Workplaces for Women™ 2021 among large organizations and 100 Best Large Workplaces for Millennials. In addition, we were ranked the #1 Top Workplace in 2021 by the Orange County Register for the second consecutive year.

Simplifying healthcare for all - that seems like a tall task to accomplish considering the last two years. What we once considered simple activities in our daily lives, such as going to the store to buy groceries or getting children to school, was upended by a global pandemic. Factor in the massive changes in healthcare operations, and it is clear the system needs to continue to evolve. It also cements my belief that Experian Health’s mission is even more relevant and achievable today than it was pre-COVID 19. In fact, this aspiration of simplifying healthcare for all is top of mind for me and Experian as we go into HIMSS22, the premier healthcare conference being held in Orlando this week. The healthcare industry has undergone massive changes since the fateful announcements in early 2020. While adapting to the pandemic was a huge undertaking for many organizations at the onset, those who opted to embrace change saw the payoff as they simplified administrative tasks and created efficiencies for both providers and patients. We saw organizations eagerly adopt technology and tools to take paperwork digital, streamlining the patient intake process and improving the accuracy of the data received. Instead of phone calls, patients and providers scheduled appointments and communicated online through secure portals saving time and manpower. The use of telehealth appointments allowed providers to see more patients and do so safely. Who would not want the simplicity of carving out just a few minutes from the comfort of one’s home for a non-urgent appointment? We are proud to have been a part of this evolution helping healthcare organizations pivot in the face of such a daunting predicament. For example, through our digital front door solutions, patients were able to schedule and pre-register for appointments online avoiding extra time spent in waiting rooms. We verified hundreds of thousands of identities quickly as Americans lined up for COVID-19 testing and vaccines. Our mobile payments system served to make the financial aspects of care easier to fulfill. Providers turned to us to help recoup costs from the government and insurers for COVID-19 care with our insurance discovery solution. Experian will not stop here, and we will continue to innovate high-tech, data-driven approaches to simplify healthcare for all; I hope the industry doesn’t stop either in tackling tough operational challenges using the power of technology and data. With this in mind, I look forward to hearing about the lessons learned by the industry as well as future innovations from the participants at HIMSS22. It’s the “can’t-miss healthcare conference of the year,” and we are pleased to be a sponsor and exhibitor once again. For those attending, visit us at Booth #3059. Taking the conference playbook of a hybrid approach with both digital and in-person participation, the healthcare industry should follow suit. Let’s certainly keep valuable in-person mechanisms in place, but not forget about the last two years and the incredible progress made that moved the industry forward. At Experian, we strive to help clients operate more quickly, smoothly and efficiently across the healthcare journey. With a new mindset in the industry and the tools available to act on change from providers like Experian, simplifying healthcare for all is not just a mission but an outcome we must achieve. Tom Cox is President of Experian Health.

At Experian we pride ourselves on having a great People First culture, it’s something we are all proud of and want to protect. We do this through a dynamic, positive and inclusive working environment for all employees, with the tools and support they need to grow and develop. With that in mind, we are hosting our first ever Careers week for our employees around the world. During Careers week, 70 sessions are taking place across different time zones, with a mix of inspiring speakers, bitesize learning events and insights into new career resources and tools coming in 2022 supporting the ongoing development and learning of our people The theme for this year’s Careers week is ‘Be World Ready’. Put simply this means: Being Aware – having a good understanding about what is happening to jobs and careers in the marketplace Being Relevant – keeping your skills and experiences fresh and meaningful Being Marketable - making sure you stand out from the crowd Our employees will get the chance to hear from internal and external speakers, including experts in their fields sharing the latest thinking on career development and learning. Leaders from Experian, Google, AWS, Microsoft and many others are part of this exciting event. The whole week has been designed to give people the space to learn and reach their highest potential. To find out more about careers at Experian, visit our global careers page.

Advocating for equality isn’t just my job, it’s a personal passion of mine. In my hometown, I’ve served as part of the organizing committee that planned Chicago’s Gay Black Pride. Working with a company that has values similar to my life’s work is an honor. That’s one of the reasons why I’m excited to share that for the fourth year in a row, Experian has been named a “Best Place to Work for LGBTQ Equality" from the Human Rights Campaign Foundation. Attaining a 100% rating from the Human Rights Campaign Foundation’s Corporate Equality Index is reflective of the work we’re doing to end discrimination against LGBTQ+ people and bring about fairness and equality for all. Our PRIDE employee resource group organizes programs year-round that raise awareness of issues including transgender rights, encouraging intersectionality with our other employee resource groups, and leading partnerships with organizations such as the Trevor Project and Out and Equal. It’s critical that these efforts within our organization extend to how we serve our communities externally. As an example, yesterday, we shared the process we now offer to help transgender and non-binary consumers update their name on their Experian credit report without impacting their credit history. Earning a perfect score by the nation’s largest LGBTQ+ civil rights organization is a tribute to our coworkers and company leadership, and continues to serve as an inspiration to follow our mission. This year, we will continue our efforts as we focus on credit education and awareness for those who are credit invisible within the LGBTQ+ community. Fostering and nurturing a culture of inclusion is part of our greater purpose. We are proud the HRC has recognized our work so far, and we look forward to what’s to come. For more information about Experian’s commitment to equity and diversity, visit experian.com/diversity

As a leading information services company, some of our chief priorities include protecting and ensuring the accuracy of consumer information. The integrity of our data is critical and aligns with our efforts to advocate for financial inclusion for everyone. Data accuracy is particularly relevant for the transgender and non-binary community with regard to name changes. It’s important to note that information about gender/sex, age, race, ethnicity, religion or sexual orientation is not included in credit reports or scores. However, when someone transitions, and changes their name, their credit and financial history may still be tied to their birth name, which is also referred to as their “deadname.” This can unintentionally “out” the consumer or force them to establish a new credit history. At Experian, we have a process through which those who identify as transgender and non-binary can provide legal documentation to prove their identity without the negative emotional and financial impact. You can learn more about this process here. When you affirm your identity and update your name, Experian will also suppress your deadname so it does not appear on your Experian credit report. Taking these steps only changes your name on your Experian credit reports, and you may need to inquire about the process with other credit bureaus. Fair access to credit tools is part of our mission, as is providing these services with dignity and respect. At Experian, this is our purpose, advocating for all communities and people. This is financial inclusion.

In 2021, Experian announced that United for Financial Health programme would be launching in two EMEA markets - Italy and South Africa. Today we are pleased to bring you more news of our plans in South Africa. Our partnership with the National Small Business Chamber is focused on supporting Small and Medium-sized Enterprises (SMEs) to improve their financial fitness. As a result of the pandemic, many small businesses are under enormous strain in the current environment. As the backbone of the South African economy, any challenges faced among these enterprises may have far-reaching implications on the number of unemployed people. Our campaign with the NSBC aims to support SMEs to stay in business and become more resilient to economic disruptions as they continue to be a driving force of inclusive economic growth and job creation in the country. Many SMEs are harming their chances of gaining access to credit, getting better deals from suppliers, and securing additional funding to help grow their business due to a lack of awareness and understanding of their business credit profile. Working alongside the NSBC, we aim to educate, encourage and assist SMEs to become creditworthy. The programme aims to provide tangible ways to help improve financial health, help SMEs overcome the financial difficulties that have resulted from the effects of the pandemic and kick-start people on the road to recovery. Mike Anderson, the CEO of our partners the NSBC, said: “We are extremely excited to launch a ‘How to become financially fit’ campaign in partnership with Experian South Africa, one of the leading credit bureaus, where we can equip SMEs with key tips and strategies to assist them in understanding their financial and credit health. The aim is to empower them to understand the impact of both their personal and business credit profiles on their business’s reputation and ultimately their ability to access the funding required to maintain and grow their businesses.” As part of this financial education drive, we’ll support a series of webinars hosted by the NSBC, with topics ranging from how to improve both your personal and business credit profiles, managing your cash flow, understanding what credit providers are looking for as well as protecting your own business from credit risk. The webinars are open to all NSBC members and will kick off on 28 January 2022 and run until the end of March. For more information on the ‘How to get financially fit’ NSBC campaign in partnership with Experian South Africa visit www.nsbc.africa.

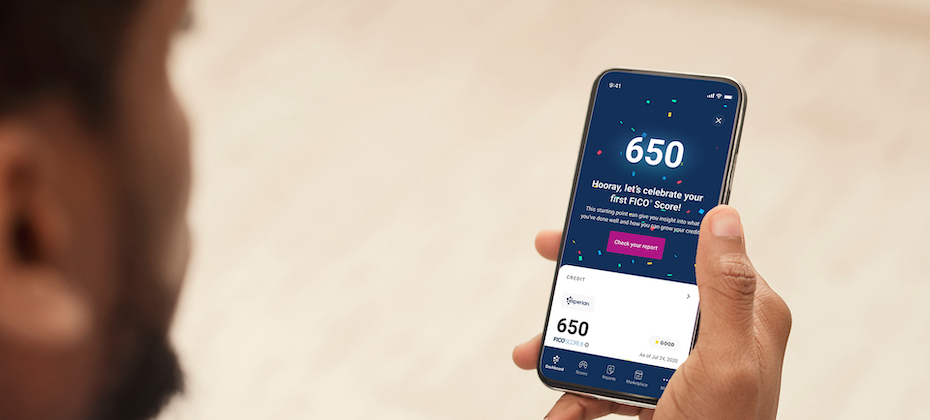

For the past several years, we’ve been on a journey to improve financial access for millions of people around the world. We’ve made it our job to help consumers get the best financial outcomes. This focus on consumers defines us and informs everything we do. In 2019, we reshaped how consumers access credit with Experian Boost™. Since then, nearly 9 million consumers have connected to the product. While we are proud of what we have and continue to accomplish with Experian Boost, we know there is more to be done to ensure more consumers can access fair and affordable credit. Improving outcomes for underserved consumers When credit is used responsibly, it can create new opportunities from getting a college degree, buying a car or home and starting or expanding a business. These are milestones that help people establish careers, build wealth and ultimately achieve greater financial freedom. Yet, there are millions of consumers who are unable to participate in the mainstream financial ecosystem today because they don’t have a financial identity. In fact, our recent research shows there are at least 28 million credit invisibles in the U.S. with an additional 21 million consumers who are unscoreable by the credit score models most used by lenders today. Without an established credit history, these consumers struggle to qualify for everything from an auto loan to a mortgage and even an apartment or employment. This problem more frequently impacts communities of color with 28 percent of all Black and 26 percent of all Hispanic consumers currently unscoreable or credit invisible. Increasing financial inclusion depends on creating opportunities for underrepresented consumers to succeed. And this starts with ensuring all consumers have a financial identity. Bringing financial power to all with Experian Go The challenge is many consumers who are not in the credit ecosystem today are unsure where to start. Today, we reached a pivotal and exciting milestone in our commitment to consumers with the launch of Experian Go™. This new program opens the front door to the financial ecosystem for millions of consumers by helping them establish their financial identity and move from credit invisible to scoreable. Within minutes, credit invisibles can have an authenticated Experian credit report, tradelines and a credit history by using Experian Boost™[1], and instant access to financial offers through Experian Go. In fact, early analysis shows 91 percent of consumers with no credit history who connect to Experian Boost, a free feature that allows users to contribute their on-time cell phone, video streaming service, internet, and utility payments directly to their Experian credit report, can become scoreable in minutes with an average starting near-prime FICO® Score of 665[2]. Throughout the experience, we’ll provide ongoing credit education and access to tools like Experian Boost™ to make it easy for consumers to learn how to use and responsibly grow their credit histories. Until now, our industry has struggled to verify the identity of credit invisibles. Over the last several years, we’ve introduced new identity verification technologies to our toolbox. With Experian Go, we’re leveraging these technologies to verify a credit invisible’s identity and get them in the front door to start building credit. No other credit bureau or organization is doing this today. During our pilot, we helped more than 15,000 consumers establish their credit history. This is a great start. Now that Experian Go has launched, I look forward to helping millions more consumers get the credit they deserve. To learn more about Experian Go, visit www.experian.com/go. [1] Results may vary. Some may not see improved scores or approval odds. Not all lenders use Experian credit files, and not all lenders use scores impacted by Experian Boost. [2] Experian analysis based on an anonymized and statistically relevant sample of consumer credit reports with only Experian Boost tradelines included and FICO® Scores. December 2021.

I’m delighted to announce that Experian has been named as a Top Employer across five countries. Our teams in the UK, Germany, Brazil, Singapore and Australia were all recognised in the 2022 awards which is a fantastic achievement. At Experian we pride ourselves on having a great People First culture, it’s something we are all proud of and want to protect. We do this by supporting a dynamic, positive and inclusive working environment for our employees wherever they are in the world. Our people are passionate about the work that we do, using data, analytics and technology to help transform lives and create a better tomorrow for people and organisations. We see our people live that purpose everyday in their work and it is wonderful to see that pride, about the role we play - supporting clients, consumers economies and society – getting recognised once again.