Tag: data

As financial institutions and other organizations scramble to formulate crisis response plans, it’s important to consider the power of data and analytics. Jim Bander, PhD, Experian’s Analytics and Optimization Market Lead discusses the ways that data, analytics and models can help during a crisis. Check out what he had to say: What implications does the global pandemic have on financial institutions’ analytical needs? JB: COVID-19 is a humanitarian crisis, one that parallels Hurricanes Sandy and Katrina and other natural disasters but which far exceeds their magnitude. It is difficult to predict the impact as huge parts of the global economy have shut down. Another dimension of this disaster is the financial impact: in the US alone, more than 17 million people applied for unemployment in the first 6 weeks of the COVID-19 crisis. That compares to 15 million people in 18 months during the Great Recession. Data and analytics are more important than ever as financial institutions formulate their responses to this crisis. Those institutions need to focus on three key things: safety, soundness, and compliance. Safety: Financial institutions are taking immediate action to mitigate safety risks for their employees and their customers. Soundness: Organizations need to mitigate credit and fraud risk and to evaluate capital and liquidity. Some executives may need a better understanding of how their bank’s stress scenarios were calculated in the past to understand how they must be updated for the future. Important analytic functions include performing portfolio monitoring and benchmarking—quantifying the effects not only of consumer distress, but also of low interest rates. Compliance: Understanding and meeting complex regulatory and compliance requirements is crucial at this time. Companies have to adapt to new credit reporting guidelines. CECL requirements have been relaxed but lenders should assess the effects of COVID, and not only during their annual stress tests. As more consumers seek credit, from an analytics perspective, what considerations should financial institutions make during this time? JB: During this volatile time, analytics will help financial institutions: Identify financially stressed consumers with early warning indicators Predict future consumer behavior Respond quickly to changes Deliver the best treatments at the right time for individual customers given their specific situations and their specific behavior. Financial institutions should be reevaluating where their organizations have the most vulnerability and should be taking immediate action to mitigate these risks. Some important areas to keep an eye on include early warning indicators, changes in fraudulent behavior (with the increase in digital engagements), and changes in customer behavior. Banks are already offering payment flexibility, deferments, and credit reporting accommodations. If volatility continues or increases, they may need to offer debt forgiveness plans. These organizations should also be prepared to understand their own changing constraints—such as budget, staffing levels, and liquidity requirements— especially as consumers accelerate their move to digital channels. In the near future, lenders should be optimizing their operations, servicing treatments, and lending policies to meet a number of possibly conflicting objectives in the presence of changing constraints and somewhat unpredictable transaction volumes. What is the smartest next play for financial institutions? JB: I see our smartest clients doing four things: Adapting to the new normal Maintaining engagement with existing customers by refreshing data that companies have on-hand for these consumers, and obtain additional views of these customers for analytics and data-driven decisioning Reallocating operational resources and anticipating the need for increased capacity in various servicing departments in the future Improving their risk management practices What is Experian doing to help clients improve their risk management? JB: During this time, banks and other financial institutions are searching for ways to predict consumer behavior, especially during a crisis that combines aspects of a natural disaster with characteristics of a global recession. It is more important than ever to use analytics and optimization. But some of the details of the methodology is different now than during a time of economic expansion. For example, while credit scores (like FICO® and VantageScore® credit scores) will continue to rank consumers in terms of their probability to pay, those scores must be interpreted differently. Furthermore, those scores should be combined with other views of the consumer—such as trends in consumer behavior and with expanded FCRA-compliant data (data that isn’t reported to traditional credit bureaus). One way we’re helping clients improve their credit risk management is to provide them with a list of 140 consumer credit data attributes in 10 categories. With this list, companies will be able to better manage portfolio risk, to better understand consumer behavior, and to select the next best action for each consumer. Four other things we’re doing: We’re quickly updating our loss forecasting and liquidity management offerings to account for new stress scenarios. We’re helping clients review their statistical models’ performance and their customer segmentation practices, and helping to update the models that need refreshing. Our consulting team—Experian Advisory Services—has been meeting with clients virtually--helping them update, execute their crisis and downturn responses, and whiteboard new or updated tactical plans. Last but not least, we’re helping lenders and consumers defend themselves against a variety of fraud and identity theft schemes. Experian is committed to helping your organization during these uncertain times. For more resources, visit our Look Ahead 2020 Hub. Learn more Jim Bander, PhD, Analytics and Optimization Market Lead, Decision Analytics, Experian North America Jim Bander, PhD joined Experian in April 2018 and is responsible for solutions and value propositions applying analytics for financial institutions and other Experian business-to-business clients throughout North America. Jim has over 20 years of analytics, software, engineering and risk management experience across a variety of industries and disciplines. He has applied decision science to many industries including banking, transportation and the public sector. He is a consultant and frequent speaker on topics ranging from artificial intelligence and machine learning to debt management and recession readiness. Prior to joining Experian, he led the Decision Sciences team in the Risk Management department at Toyota Financial Services.

This is the second in a series of blog posts highlighting optimization, artificial intelligence, predictive analytics, and decisioning for lending operations in times of extreme uncertainty. The first post dealt with optimization under uncertainty. The word "unprecedented" gets thrown around pretty carelessly these days. When I hear that word, I think fondly of my high school history teacher. Mr. Fuller had a sign on his wall quoting the philosopher-poet George Santayana: "Those who cannot remember the past are condemned to repeat it." Some of us thought it meant we had to memorize as many facts as possible so we wouldn't have to go to summer school. The COVID-19 crisis--with not only health consequences but also accompanying economic and financial impacts--certainly breaks with all precedents. The bankers and other businesspeople I've been listening to are rightly worried that This Time is Different. While I'm sure there are history teachers who can name the last time a global disaster led to a widescale humanitarian crisis and an economic and financial downturn, I'm even more sure times have changed a lot since then. But there are plenty of recent precedents to guide business leaders and other policymakers through this crisis. Hurricanes Katrina and Sandy impacted large regions of the United States, with terrible human consequences followed by financial ones. Dozens of local disasters—floods, landslides, earthquakes—devastated smaller numbers of people in equally profound ways. The Great Recession, starting in 2008, put millions of Americans and others around the world out of work. Each of those disasters, like this one, broke with all precedents in various ways. Each of those events was in many ways a dress rehearsal, as bankers and other lenders learned to provide assistance to distressed businesses and consumers, while simultaneously planning for the inevitable changes to their balance sheets and income statements. Of course, the way we remember the past has changed. Just as most of us no longer memorize dates--we search for them on the web--businesspeople turn to their databases and use analytics to understand history. I've been following closely as the data engineers and data scientists here at Experian have worked on perhaps their most important problem ever. Using Experian's Ascend Analytical Sandbox--named last year as the Best Overall Analytics Platform, they combed through over eighteen years of anonymized historical data covering every credit report in the United States. They asked--using historical experience, wisdom, time-consuming analytics, a little artificial intelligence, and a lot of hard work--whether predicting credit performance during and after a crisis is possible. They even considered scenarios regarding what happens as creditors change the way they report consumer delinquencies to the credit bureaus. After weeks of sleepless nights, they wrote down their conclusions. I've read their analysis carefully and I’m pleased to report that it says…Drumroll, please…Yes, but. Yes, it's possible to predict consumer behavior after a disaster. But not in precisely the same way those predictions are made during a period of economic growth. For a credit risk manager to review a lending portfolio and to predict its credit losses after a crisis requires looking at more data--and looking at it a little differently--than during other periods. Yes, after each disaster, credit scores like FICO® and VantageScore® credit scores continued to rank consumers from most likely to least likely to repay debts. But the interpretation of the score changes. Technically speaking, there is a substantial shift in the odds ratio that is particularly pronounced when a score is applied to subprime consumers. To predict borrower behavior more accurately, our scientists found that it helps to look at ten additional categories of data attributes and a few additional types of mathematical models. Yes, there are attributes on the credit report that help lenders identify consumer distress, willingness, and ability to pay. But, the data engineers identified that during times like these it is especially helpful to look beyond a single point in time; trends in a consumer's payment history help understand whether that customer is changing their typical behavior. Yes, the data reported to the credit bureaus is predictive, especially over time. But when expanded FCRA data is available beyond what is traditionally reported to a bureau, that data further improves predictions. All told, the data engineers found over 140 data attributes that can help lenders and others better manage their portfolio risk, understand consumer behavior, appreciate how the market is changing, and choose their next best action. The list of attributes might be indispensable to a credit data specialist whose institution needs to weather the coming storm. Because Experian knows how important it is to learn from historical precedents, we're sharing the list at no charge with qualified risk managers. To get the latest Experian data and insights or to request the Crisis Response Attributes recommendation, visit our Look Ahead 2020 page. Learn more

With new legislation, including the Coronavirus Aid, Relief, and Economic Security (CARES) Act impacting how data furnishers will report accounts, and government relief programs offering payment flexibility, data reporting under the coronavirus (COVID-19) outbreak can be complicated. Especially when it comes to small businesses, many of which are facing sharp declines in consumer demand and an increased need for capital. As part of our recently launched Q&A perspective series, Greg Carmean, Experian’s Director of Product Management and Matt Shubert, Director of Data Science and Modelling, provided insight on how data furnishers can help support small businesses amidst the pandemic while complying with recent regulations. Check out what they had to say: Q: How can data reporters best respond to the COVID-19 global pandemic? GC: Data reporters should make every effort to continue reporting their trade experiences, as losing visibility into account performance could lead to unintended consequences. For small businesses that have been negatively affected by the pandemic, we advise that when providing forbearance, deferrals be reported as “current”, meaning they should not adversely impact the credit scores of those small business accounts. We also recommend that our data reporters stay in close contact with their legal counsel to ensure they follow CARES Act guidelines. Q: How can financial institutions help small businesses during this time? GC: The most critical thing financial institutions can do is ensure that small businesses continue to have access to the capital they need. Financial institutions can help small businesses through deferral of payments on existing loans for businesses that have been most heavily impacted by the COVID-19 crisis. Small Business Administration (SBA) lenders can also help small businesses take advantage of government relief programs, like the Payment Protection Program (PPP), available through the CARES Act that provides forgiveness on up to 75% of payroll expenses and 25% of other qualifying expenses. Q: How do financial institutions maintain data accuracy while also protecting consumers and small businesses who may be undergoing financial stress at this time? GC: Following bureau recommendations regarding data reporting will be critical to ensure that businesses are being treated fairly and that the tools lenders depend on continue to provide value. The COVID-19 crisis also provides a great opportunity for lenders to educate their small business customers on their business credit. Experian has made free business credit reports available to every business across the country to help small business owners ensure the information lenders are using in their credit decisioning is up-to-date and accurate. Q: What is the smartest next play for financial institutions? GC: Experian has several resources that lenders can leverage, including Experian’s COVID-19 Business Risk Index which identifies the industries and geographies that have been most impacted by the COVID crisis. We also have scores and alerts that can help financial institutions gain greater insights into how the pandemic may impact their portfolios, especially for accounts with the greatest immediate exposure and need. MS: To help small businesses weather the storm, financial institutions should make it simple and efficient for them to access the loans and credit they need to survive. With cash flow to help bridge the gap or resume normal operations, small businesses can be more effective in their recovery processes and more easily comply with new legislation. Finances offer the support needed to augment currently reduced cash flows and provide the stability needed to be successful when a return to a more normal business environment occurs. At Experian, we’re closely monitoring the updates around the coronavirus outbreak and its widespread impact on both consumers and businesses. We will continue to share industry-leading insights to help data furnishers navigate and successfully respond to the current environment. Learn more About Our Experts Greg Carmean, Director of Product Management, Experian Business Information Services, North America Greg has over 20 years of experience in the information industry specializing in commercial risk management services. In his current role, he is responsible for managing multiple product initiatives including Experian’s Small Business Financial Exchange (SBFE), domestic and international commercial reports and Corporate Linkage. Recently, he managed the development and launch of Experian’s Global Data Network product line, a commercial data environment that provides a single source of up to date international credit and firmographic information from Experian commercial bureaus and Tier 1 partners across the globe. Matt Shubert, Director of Data Science and Modelling, Experian Data Analytics, North America Matt leads Experian’s Commercial Data Sciences Team which consists of a combination of data scientists, data engineers and statistical model developers. The Commercial Data Science Team is responsible for the development of attributes and models in support of Experian’s BIS business unit. Matt’s 15+ years of experience leading data science and model development efforts within some of the largest global financial institutions gives our clients access to a wealth of knowledge to discover the hidden ROI within their own data.

In uncertain times, we need to find ways to adapt to our situation. We want to help you manage through this unprecedented period.

For financial marketers, long gone are the days of branded coffee mugs, teddy bears and the occasional print ad. Financial marketers are charged with customizing messaging and offerings at a customer level, increasing conversion rates, and moving beyond digital while keeping an eye on traditional channels. Additionally, financial marketing teams are having to do it all with less; according to CMO Survey, marketing budgets have remained stagnant for the last 6 years. Accordingly, competing in today’s world requires transforming your organization to address rapidly increasing complexity while containing costs. Here are four tactics leading-edge firms are using to respond to changes in the market and better serve customers. More data, fewer problems Financial institutions ingest a mind-boggling variety of data, transaction details, transaction history, credit scores, customer preferences, etc. It can be difficult to know where to start or what to do with what is often terabytes of data. But the savviest teams are mining their unique data, along with bureau data, and other alternative and third-party data for rich decision making that drives differentiation. Getting analytical In financial institutions, advanced analytics has traditionally lived with lenders, underwriters, risk and fraud, departments, etc. But marketers too can find the value in the volume, velocity and variety of new data sources available to financial institutions. Using advanced analytics allows the most forward-thinking financial marketers to better target customers, personalize experiences, respond in near-real-time or even predict actions, and measure the impact of marketing investments. Customized quality time with customers Thanks to the likes of Google and Amazon, consumers have become accustomed to individualized interactions with firms they utilize. And this desire is just as present when it comes to their financial institution. But banks, credit unions and fintechs have been historically slow to respond. According to a recent Capgemini study, 70% of US consumers feel like their financial institution doesn’t understand their needs. The most dynamic financial marketing teams tailor quality experiences that increase consumer engagement and long-term relationships. All the channels, all the time The financial marketer’s job doesn’t stop at creating bespoke experiences for customers. Firms are also having to leverage an omnichannel approach to reach these clients, across an ever-growing number of channels and touchpoints. If that wasn’t enough, campaign cycles are shortening to match consumers changing demands and need for instant gratification—again, thanks Amazon. But the best teams determine which media or interaction resonates most effectively with clients, whether face-to-face, via an app, chatbot, or social media and have conversations across all of them seamlessly. It’s clear, financial firms must transform their approach to address increasing market complexity without increasing costs. Financial marketers are saddled with stagnant marketing budgets, proliferating media channels and shorter campaign cycles, with an expectation to continue delivering results. It’s a very tall order, especially if your financial institution is not leveraging data, analytics and insights as the differentiators they could be. CMOs and their marketing teams must invest in new technologies, strategies and data sources that best reflect the expectations of their customers. How is your bank or credit union responding to these financial marketing challenges? Watch our 2020 Credit Marketing Trends On-Demand Webinar

Do you have 20/20 vision when it comes to the readiness of your organization? How financially healthy are your customers today? They are likely facing some challenges and difficult choices. Based on a study by the Center for Financial Services Innovation (CFSI), almost half of the US adult population - that’s 112.5 million - say they do not have enough savings to cover at least three months of living expenses. With debt rising and a possible recession on the horizon, it’s crucial to have a solid strategy in place for your organization. Here are three easy steps to help you prepare: Anticipate the recession before it arrives Gathering a complete view of your customers can be difficult if you have multiple systems, which can result in subjective, costly and inefficient processes. If you don’t have a full picture of your customers, it’s hard to understand their risk, behavior and ability to pay and to determine the most effective treatment decisions. Having the right data is only the first step. Using analytics to make sense of the data helps you better understand your customers at an individual level, which will increase recovery rates and improve the customer experience. Analytics can provide early-warning indicators that identify customers most likely to miss payments, predict future behavior, and deliver the best treatment option based on a customer’s specific situation or behavior. With a deeper understanding of at-risk customers, you can apply more targeted interventions that are specific to each customer, so you can be confident your collections process is individualized, efficient and fair. The result? A cost-effective, compliant process focused on retaining valuable customers and reducing losses. What to look for: ✔ Know when customers are experiencing negative credit events ✔ View consumer credit trends that may not yet be visible on your own account base ✔ Watch for payment stress – understand the actual payment consumers are making. Is it changing? ✔ See individual trends and take action – are your customers sliding down to a lower score band? ✔ Understand how your client-base is performing within your own portfolio and with other organizations Take immediate and impactful actions around risk mitigation and staffing Every interaction with consumers needs optimizing, from target marketing through to collections and recovery. Organizations that proactively modernize their business to scale and increase effectiveness before the next economic downturn may avoid struggling to address rising delinquencies when the economy corrects itself. This may improve portfolio performance and collection capabilities — significantly increasing recoveries, containing costs and sustaining returns. Identify underperforming products and inefficient processes by staff. Consider reassessing the data used and the manual processes required for making decisions. Optimize product pricing and areas where organizations or staff could automate the decision processes. Areas to focus: ✔ Identity theft protection and account takeover awareness ✔ Improve underwriting strategy and automation ✔ Maximize profitability — drive spend, optimize approvals, line assignment and pricing ✔ Evaluate collection risk strategies and operational efficiencies Design and deploy a strategy to be organizationally and technologically ready for change Communication is key in debt recovery. Failing to contact customers via their preferred channel can cause frustration and reduce the likelihood of recovery. Your customers are looking for a convenient and discreet way to negotiate or repay debt, and if you aren’t providing one, you’re incurring higher collections costs and lower recovery rates. With developments in the digital world, consumer interactions have changed. Most people prefer to communicate via mobile or online, with little to no human interaction. Behavioral analytics help to automate and decide the next best action, so you contact the right customer at the right time through the right channel. In addition, offering a convenient, discreet way to negotiate or repay debt can result in customers who are more engaged and more likely to pay. Online and self-service portals along with AI-powered chatbots use the latest technology to provide a safe and customer-centric experience, creating less time-consuming interactions and higher customer satisfaction. Your digital collections process is more convenient and less stressful for consumers and more profitable and compliant for you. Visualize the future... ✔ Superior customer service is embraced at the end of the customer life cycle as it is in the beginning ✔ Leverage data, analytics, software, and industry expertise to drive an automated collections process with fewer manual interventions ✔ Meet the growing expectation for digital consumer self-service by providing the ability to proactively negotiate and manage debt through preferred contact channels ✔ When economy and market conditions change for the worst, have the right data, analytics, software in place and be prepared to implement relevant collections strategies to remain competitive in the market Don’t wait until the next recession hits. Our collaborative approach to problem solving ensures you have the right solution in place to solve your most complex problems and are ready for market changes. The combination of our data, analytics, fraud tools, decisioning software and consulting services will help you proactively manage your portfolio to minimize the flow of accounts into collections and modernize your collections and recovery processes. Learn More

According to Experian’s Q3 2019 State of the Automotive Finance Market report, used vehicle financing increased across all credit tiers.

The challenges facing today’s marketers seem to be mounting and they can feel more pronounced for financial institutions. From customizing messaging and offerings at an individual customer level, increasing conversion rates, moving beyond digital while keeping an eye on traditional channels, and more, financial marketers are having to modernize their approach to customer acquisition. The most forward-thinking financial firms are turning to customer acquisition engines to help them best build, test and optimize their custom channel targeting strategies faster than ever before. But what functionality is right for your company? Here are 5 capabilities you should look for in a modern customer acquisition engine. Advanced Segmentation It’s without question that targeting and segmentation are vital to a successful financial marketing strategy. Make sure you select a tool that allows for advanced segmentation, ensuring the ability to uncover lookalike groups with similar attributes or behaviors and then customize messages or offerings accordingly. With the right customer acquisition engine, you should be able to build filters for targeted segments using a range of data including demographic, past behavior, loyalty or transaction history, offer response and then repurpose these segments across future campaigns. Campaign Design With the right campaign design, your team has the ability to greatly affect customer engagement. The right customer acquisition engine will allow your team to design a specific, optimized customer journey and content for each of the segments you create. When you’re ready to apply your credit criteria to the audience to generate a pre-screen, the best tools will allow you to view the size of your list adjusted in real-time. Make sure to look for an acquisition engine that can do all of this easily with a drag and drop user experience for faster and efficient campaign design. Rapid Deployment Once you finalize your audience for each channel or offer, the clock starts ticking. From bureau processing, data aggregation, targeting and deployment, the data that many firms are currently using for prospecting can be at least 60-days. When searching for a modern customer acquisition engine, make sure you choose a tool that gives you the option to fetch the freshest data (24-48 hours) before you deploy. If you’re sending the campaign to an outside firm to execute, timing is even more important. You’ll also want a system that can encrypt and decrypt lists to send to preferred partners to execute your marketing campaign. Support Whether you have an entire marketing department at your disposal or a lean, start-up style team, you’re going to want the highest level of support when it comes to onboarding, implementation and operational success. The best customer acquisition solution for your company will have a robust onboarding and support model in place to ensure client success. Look for solutions that offer hands-on instruction, flexible online or in-person training and analytical support. The best customer acquisition tool should be able to take your data and get you up and running in less than 30 days. Data, Data and more Data Any customer acquisition engine is only as good as the data you put into it. It should, of course, be able to include your own client data. However, relying exclusively on your own data can lead to incomplete analysis, missed opportunities and reduced impact. When choosing a customer acquisition engine, pick a system that gives your company access to the most local, regional and national credit data, in addition to alternative data and commercial data assets, on top of your own data. The optimum solutions can be fueled by the analytical power of full-file, archived tradeline data, along with attributes and models for the most robust results. Be sure your data partner has accounted for opt-outs, excludes data precluded by legal or regulatory restrictions and also anonymizes data files when linking your customer data. Data accuracy is also imperative here. Choose a marketing and technology partner who is constantly monitoring and correcting discrepancies in customer files across all bureaus. The best partners will have data accuracy rates at or above 99.9%.

With the growing need for authentication and security, fintechs must manage risk with minimal impact to customer experience. When implementing tactical approaches for fraud risk strategy operations, keeping up with the pace of fraud is another critical consideration. How can fintechs be proactive about future-proofing fraud strategies to stay ahead of savvy fraudsters while maintaining customer expectations? I sat down with Chris Ryan, Senior Fraud Solutions Business Consultant with Experian Decision Analytics, to tap into some of his insights. Here’s what he had to say: How have changes in technology added to increased fraud risk for businesses operating in the online space? Technology introduces many risks in the online space. As it pertains to the fintech world, two stand out. First, the explosion in mobile technology. The same capabilities that make fintech products broadly accessible makes them vulnerable. Anyone with a mobile device can attempt to access a fintech and try their hand at committing fraud with very little risk of being caught or punished. Second, the evolution of an interconnected, digital ‘marketplace’ for stolen data. There’s an entire underground economy that’s focused on connecting the once-disparate pieces of information about a specific individual stolen from multiple, unrelated data breaches. Criminal misrepresentations are more complete and more convincing than ever before. What are the major market drivers and trends that have attributed to the increased risk of fraud? Ultimately, the major market drivers and trends that drive fraud risk for fintechs are customer convenience and growth. In terms of customer convenience, it’s a race to meet customer needs in real time, in a single online interaction, with a minimally invasive request for information. But, serving the demands of good customers opens opportunities for identity misuse. In terms of growth, the pressure to find new pockets of potential customers may lead fintechs into markets where consumer information is more limited, so naturally, there are some risks baked in. Are fintechs really more at risk for fraud? If so, how are fintechs responding to this dynamic threat? The challenge for many fintechs has been the prioritization of fraud as a risk that needs to be addressed. It’s understandable that fintech’s initial emphasis had to be the establishment of viable products that meet the needs of their customers. Obviously, without customers using a product, nothing else matters. Now that fintechs are hitting their stride in terms of attracting customers, they’re allocating more of their attention and innovative spirit to other areas, like fraud. With the right partner, it’s not hard for fintechs to protect themselves from fraud. They simply need to acquire reliable data that provides identity assurance without negatively impacting the customer experience. For example, fintechs can utilize data points that can be extracted from the communications channel, like device intelligence for example, or non-PII unique identifiers like phone and email account data. These are valuable risk indicators that can be collected and evaluated in real time without adding friction to the customer experience. What are the major fraud risks to fintechs and what are some of the strategies that Risk Managers can implement to protect their business? The trends we’ve talked about so far today have focused more on identity theft and other third-party fraud risks, but it’s equally important for fintechs to be mindful of first party fraud types where the owner of the identity is the culprit. There is no single solution, so the best strategy recommendation is to plan to be flexible. Fintechs demonstrate an incredible willingness to innovate, and they need to make sure the fraud platforms they pick are flexible enough to keep pace with their needs. From your perspective, what is the future of fraud and what should fintechs consider as they evolve their products? Fraud will continue to be a challenge whenever something of value is made available, particularly when the transaction is remote and the risk of any sort of prosecution is very low. Criminals will continue to revise their tactics to outwit the tools that fintechs are using, so the best long-term defense is flexibility. Being able to layer defenses, explore new data and analytics, and deploy flexible and dynamic strategies that allow highly tailored decisions is the best way for fintechs to protect themselves. Digital commerce and the online lending landscape will continue to grow at an increasing pace – hand-in-hand with the opportunities for fraud. To stay ahead of fraudsters, fintechs must be proactive about future-proofing their fraud strategies and toolkits. Experian can help. Our Fintech Digital Onboarding Bundle provides a solid baseline of cutting-edge fraud tools that protect fintechs against fraud in the digital space, via a seamless, low-friction customer experience. More importantly, the Fintech Digital Onboarding Bundle is delivered through Experian’s CrossCore platform—the premier platform in the industry recognized specifically for enabling the expansion of fraud tools across a wide range of Experian and third-party partner solutions. Click here to learn more or to speak with an Experian representative. Learn More About Chris Ryan: Christopher Ryan is a Senior Fraud Solutions Business Consultant. He delivers expertise that helps clients make the most from data, technology and investigative resources to combat and mitigate fraud risks across the industries that Experian serves. Ryan provides clients with strategies that reduce losses attributable to fraudulent activity. He has an impressive track record of stopping fraud in retail banking, auto lending, deposits, consumer and student lending sectors, and government identity proofing. Ryan is a subject matter expert in consumer identity verification, fraud scoring and knowledge-based authentication. His expertise is his ability to understand fraud issues and how they impact customer acquisition, customer management and collections. He routinely helps clients review workflow processes, analyze redundancies and identify opportunities for process improvements. Ryan recognizes the importance of products and services that limit fraud losses, balancing expense and the customer impact that can result from trying to prevent fraud.

As the holiday shopping season kicks off, it’s prime time for fraudsters to prey on consumers who are racking up rewards points as they spend. Find out how fraud trends in loyalty and rewards programs can impact your business: Are you ready to prevent fraud this holiday season? Get started today

In today’s ever-changing and hypercompetitive environment, the customer experience has taken center-stage – highlighting new expectations in the ways businesses interact with their customers. But studies show financial institutions are falling short. In fact, a recent study revealed that 94% of banking firms can’t deliver on the “personalization promise.” It’s not difficult to see why. Consumer preferences have changed, with many now preferring digital interactions. This has made it difficult for financial institutions to engage with consumers on a personal level. Nevertheless, customers expect seamless, consistent, and personalized experiences – that’s where the power of advanced analytics comes into play. It’s no secret that using advanced analytics can enable businesses to turn rich data into insights that lead to confident business decisions and strategy development. But these business tools can actually help financial institutions deliver on that promise of personalization. According to an Experian study, 90% of organizations say that embracing advanced analytics is critical to their ability to provide an excellent customer experience. By using data and analytics to anticipate and respond to customer behavior, companies can develop new and creative ways to cater to their audiences – revolutionizing the customer experience as a whole. It All Starts With Data Data is the foundation for a successful digital transformation – the lack of clean and cohesive datasets can hinder the ability to implement advanced analytic capabilities. However, 89% of organizations face challenges on how to effectively manage and consolidate their data, according to Experian’s Global Data Management Research Benchmark Report of 2019. Because consumers prefer digital interactions, companies have been able to gather a vast amount of customer data. Technology that uses advanced analytic capabilities (like machine learning and artificial intelligence) are capable of uncovering patterns in this data that may not otherwise be apparent, therefore opening doors to new avenues for companies to generate revenue. To start, companies need a strategy to access all customer data from all channels in a cohesive ecosystem – including data from their own data warehouses and a variety of different data sources. Depending on their needs, the data elements can come from a third party data provider such as: a credit bureau, alternative data, marketing data, data gathered during each customer contact, survey data and more. Once compiled, companies can achieve a more holistic and single view of their customer. With this single view, companies will be able to deliver more relevant and tailored experiences that are in-line with rising customer expectations. From Personalized Experiences to Predicting the Future The most progressive financial institutions have found that using analytics and machine learning to conquer the wide variety of customer data has made it easier to master the customer experience. With advanced analytics, these companies gain deeper insights into their customers and deliver highly relevant and beneficial offers based on the holistic views of their customers. When data is provided, technology with advanced analytic capabilities can transform this information into intelligent outputs, allowing companies to optimize and automate business processes with the customer in mind. Data, analytics and automation are the keys to delivering better customer experiences. Analytics is the process of converting data into actionable information so firms can understand their customers and take decisive action. By leveraging this business intelligence, companies can quickly adapt to consumer demand. Predictive models and forecasts, increasingly powered by machine learning, help lenders and other businesses understand risks and predict future trends and consumer responses. Prescriptive analytics help offer the right products to the right customer at the right time and price. By mastering all of these, businesses can be wherever their customers are. The Experian Advantage With insights into over 270 million customers and a wealth of traditional credit and alternative data, we’re able to drive prescriptive solutions to solve your most complex market and portfolio problems across the customer lifecycle – while reinventing and maintaining an excellent customer experience. If your company is ready for an advanced analytical transformation, Experian can help get you there. Learn More

AI, machine learning, and Big Data – these are no longer just buzzwords. The advanced analytics techniques and analytics-based tools that are available to financial institutions today are powerful but underutilized. And the 30% of banks, credit unions and fintechs successfully deploying them are driving better data-driven decisions, more positive customer experiences and stronger profitability. As the opportunities surrounding advanced analytics continue to grow, more lenders are eager to adopt these capabilities to make the most of their datasets. And it’s understandable that financial institution are excited at the possibilities and insights that advanced analytics can bring to their business. However, there are some key considerations to keep in mind as you begin this important digital transformation. Here are three things you should do as your financial institution begins its advanced analytics journey. Ensure consistent and clean data quality Companies have a plethora of data and information on their customers. The main hurdles that many organizations face is being able to turn this information into a clean and cohesive dataset and formulating an effective and long-term data management strategy. Trying to implement advanced analytic capabilities while lacking an effective data governance strategy is like building a house on a poor foundation – likely to fail. Data quality issues, such as inconsistent data, data gaps, and incomplete and duplicated data, also haunt many organizations, making it difficult to complete their analytics objectives. Ensuring that issues in data quality are managed is the key to gaining the correct insights for your business. Establish and maintain a single view of customers The power of advanced analytics can only be as strong as the data provided. Unfortunately, many companies don’t realize that advanced analytics is much more powerful when companies are able to establish a single view of their customers. Companies need to establish and maintain a single view of customers in order to begin implementing advanced analytic capabilities. According to Experian research, a single customer view is a consistent, accurate and holistic view of your organization’s customers, prospects, and their data. Having full visibility and a 360 view into your customers paves the way for companies to make personalized, relevant, timely and precise decisions. But as many companies have begun to realize, getting this single view of customers is easier said than done. Organizations need to make sure that data should always be up-to-date, unique and available in order to begin a complete digital transformation. Ensure the right resources and commitment for your advanced analytics initiative It’s important to have the top-down commitment within your organization for advanced analytics. From the C-suite down, everyone should be on the same page as to the value analytics will bring and the investment the project might require. Organizations that want to move forward with implementing advanced analytic capabilities need to make sure to set aside the right financial and human resources that will be needed for the journey. This may seem daunting, but it doesn’t have to be. A common myth is that the costs of new hardware, new hires and the costs required to maintain, configure, and set up new technology will make advanced analytics implementation far too expensive and difficult to maintain. However, many organizations don’t realize that it’s not necessary to allocate large capital expenses to implement advanced analytics. All it takes is finding the right-sized solution with configurations to fit the team size and skill level in your organization. Moreover, finding the right partner and team (whether internal or external) can be an efficient way to fill temporary skills gaps on your team. No digital transformation initiative is without its challenges. However, beginning your advanced analytics journey on the right footing can deliver unparalleled growth, profitability and opportunities. Still not sure where to begin? At Experian, we offer a wide range of solutions to help you harness the full power and potential of data and analytics. Our consultants and development teams have been a game-changer for financial institutions, helping them get more value, insight and profitability out of their data and modeling than ever before. Learn More

It seems like artificial intelligence (AI) has been scaring the general public for years – think Terminator and SkyNet. It’s been a topic that’s all the more confounding and downright worrisome to financial institutions. But for the 30% of financial institutions that have successfully deployed AI into their operations, according to Deloitte, the results have been anything but intimidating. Not only are they seeing improved performance but also a more enhanced, positive customer experience and ultimately strong financial returns. For the 70% of financial institutions who haven’t started, are just beginning their journey or are in the middle of implementing AI into their operations, the task can be daunting. AI, machine learning, deep learning, neural networks—what do they all mean? How do they apply to you and how can they be useful to your business? It’s important to demystify the technology and explain how it can present opportunities to the financial industry as a whole. While AI seems to have only crept into mainstream culture and business vernacular in the last decade, it was first coined by John McCarthy in 1956. A researcher at Dartmouth, McCarthy thought that any aspect of learning or intelligence could be taught to a machine. Broadly, AI can be defined as a machine’s ability to perform cognitive functions we associate with humans, i.e. interacting with an environment, perceiving, learning and solving problems. Machine learning vs. AI Machine learning is not the same thing as AI. Machine learning is the application of systems or algorithms to AI to complete various tasks or solve problems. Machine learning algorithms can process data inputs and new experiences to detect patterns and learn how to make the best predictions and recommendations based on that learning, without explicit programming or directives. Moreover, the algorithms can take that learning and adapt and evolve responses and recommendations based on new inputs to improve performance over time. These algorithms provide organizations with a more efficient path to leveraging advanced analytics. Descriptive, predictive, and prescriptive analytics vary in complexity, sophistication, and their resulting capability. In simplistic terms, descriptive algorithms describe what happened, predictive algorithms anticipate what will happen, and prescriptive algorithms can provide recommendations on what to do based on set goals. The last two are the focus of machine learning initiatives used today. Machine learning components - supervised, unsupervised and reinforcement learning Machine learning can be broken down further into three main categories, in order of complexity: supervised, unsupervised and reinforcement learning. As the name might suggest, supervised learning involves human interaction, where data is loaded and defined and the relationship to inputs and outputs is defined. The algorithm is trained to find the relationship of the input data to the output variable. Once it delivers accurately, training is complete, and the algorithm is then applied to new data. In financial services, supervised learning algorithms have a litany of uses, from predicting likelihood of loan repayment to detecting customer churn. With unsupervised learning, there is no human engagement or defined output variable. The algorithm takes the input data and structures it by grouping it based on similar characteristics or behaviors, without a defined output variable. Unsupervised learning models (like K-means and hierarchical clustering) can be used to better segment or group customers by common characteristics, i.e. age, annual income or card loyalty program. Reinforcement learning allows the algorithm more autonomy in the environment. The algorithm learns to perform a task, i.e. optimizing a credit portfolio strategy, by trying to maximize available rewards. It makes decisions and receives a reward if those actions bring the machine closer to achieving the total available rewards, i.e. the highest acquisition rate in a customer category. Over time, the algorithm optimizes itself by correcting actions for the best outcomes. Even more sophisticated, deep learning is a category of machine learning that involves much more complex architecture where software-based calculators (called neurons) are layered together in a network, called a neural network. This framework allows for much broader, complex data ingestion where each layer of the neural network can learn progressively more complex elements of the data. Object classification is a classic example, where the machine ‘learns’ what a duck looks like and then is able to automatically identify and group images of ducks. As you might imagine, deep learning models have proved to be much more efficient and accurate at facial and voice recognition than traditional machine learning methods. Whether your financial institution is already seeing the returns for its AI transformation or is one of the 61% of companies investing in this data initiative in 2019, having a clear picture of what is available and how it can impact your business is imperative. How do you see AI and machine learning impacting your customer acquisition, underwriting and overall customer experience?

Last month, Kenneth Blanco, Director of the Financial Crimes Enforcement Network, warned that cybercriminals are stealing data from fintech platforms to create synthetic identities and commit fraud. These actions, in turn, are alleged to be responsible for exploiting fintech platforms’ integration with other financial institutions, putting banks and consumers at risk. According to Blanco, “by using stolen data to create fraudulent accounts on fintech platforms, cybercriminals can exploit the platforms’ integration with various financial services to initiate seemingly legitimate financial activity while creating a degree of separation from traditional fraud detection efforts.” Fintech executives were quick to respond, and while agreeing that synthetic IDs are a problem, they pushed back on the notion that cybercriminals specifically target fintech platforms. Innovation and technology have indeed opened new doors of possibility for financial institutions, however, the question remains as to whether it has also created an opportunity for criminals to implement more sophisticated fraud strategies. Currently, there appears to be little evidence pointing to an acute vulnerability of fintech firms, but one thing can be said for certain: synthetic ID fraud is the fastest-growing financial crime in the United States. Perhaps, in part, because it can be difficult to detect. Synthetic ID is a type of fraud carried out by criminals that have created fictitious identities. Truly savvy fraudsters can make these identities nearly indistinguishable from real ones. According to Kathleen Peters, Experian’s SVP, Head of Fraud and Identity, it typically takes fraudsters 12 to 18 months to create and nurture a synthetic identity before it’s ready to “bust out” – the act of building a credit history with the intent of maxing out all available credit and eventually disappearing. These types of fraud attacks are concerning to any company’s bottom line. Experian’s 2019 Global Fraud and Identity Report further details the financial impact of fraud, noting that 55% of businesses globally reported an increase in fraud-related losses over the past 12 months. Given the significant risk factor, organizations across the board need to make meaningful investments in fraud prevention strategies. In many circumstances, the pace of fraud is so fast that by the time organizations implement solutions, the shelf life may already be old. To stay ahead of fraudsters, companies must be proactive about future-proofing their fraud strategies and toolkits. And the advantage that many fintech companies have is their aptitude for being nimble and propensity for early adoption. Experian can help too. Our Synthetic Fraud Risk Level Indicator helps both fintechs and traditional financial institutions in identifying applicants likely to be associated with a synthetic identity based on a complex set of relationships and account conditions over time. This indicator is now available in our credit report, allowing organizations to reduce exposure to identity fraud through early detection. To learn more about Experian’s Synthetic Fraud Risk Level Indicator click here, or visit experian.com/fintech.

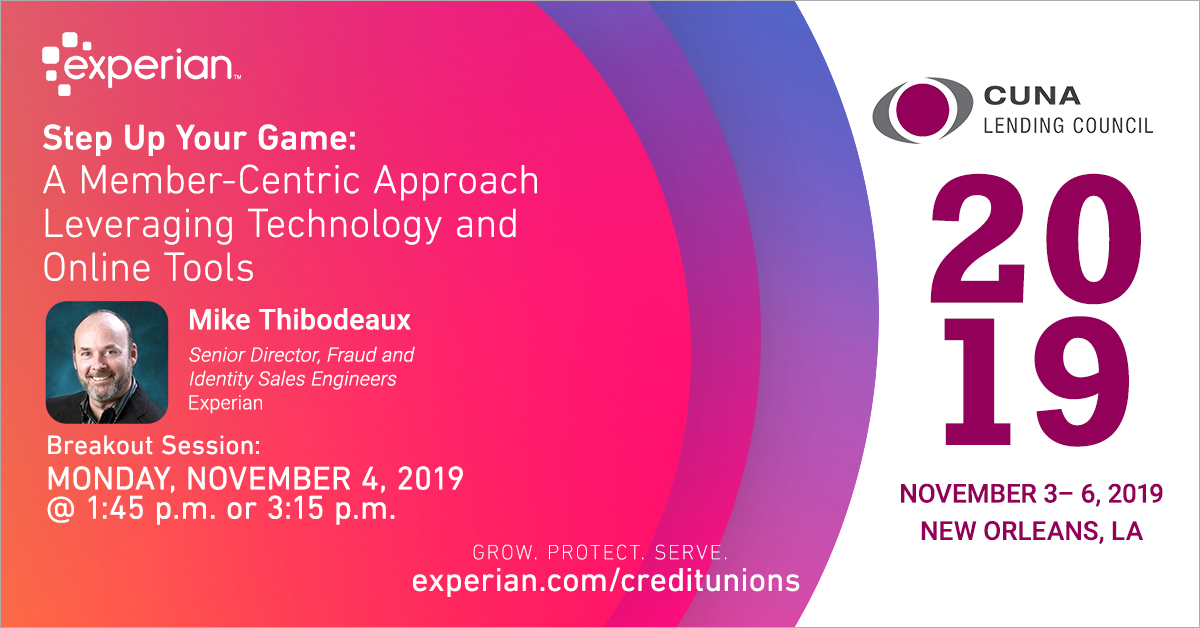

As credit unions look to grow their loan portfolios and acquire new members, improving the member experience is critical to the process and remains a primary focus. In order to compete in the lending universe, financial tools that empower and enable a positive experience are critical to meeting these requirements. That being said, an Experian study reveals that 90% of executives agree that embracing a digital transformation is critical to providing excellent experiences. In this connected, data-driven world, digital transformations are opening the door for better and greater opportunities. With data and analytics, credit unions will be able to gain data-driven insights, to identify key channels of member engagement, create complete member views and further maximize growth and lending strategies. Data-driven organizations that can anticipate their members’ needs and preferences will be able to deepen relationships and maintain relevance – gaining an edge in a highly-competitive environment. The digital revolution is happening now – and it’s time for future-focused credit unions to adapt to changing expectations. However, according to an Experian report, 39% of organizations lack the customer insight and data required to provide these member experiences. That’s where Experian comes in. Join Mike Thibodeaux, Experian’s Senior Director, Fraud and Identity Sales Engineers, for a breakout session at CUNA Lending 2019 on Monday, Nov. 4 at 1:45 p.m. or 3:15 p.m. He will take a closer look at best practices and digital tools that credit unions can use to maximize credit union membership growth, while managing and mitigating fraud. The discussion will revolve around multiple topics, critical to the member experience conversation, including: Increasing profitable loan growth Lending deeper to the underserved Levering digital services and tools for your credit union Minimizing fraud activity (specifically synthetic identity fraud) and credit losses Enhancing and maintaining positive member experiences Experian is excited to once again take part in the 2019 CUNA Lending Council Conference, an event that brings together the credit union movement’s best and brightest in lending. If you’re attending, make sure to engage and connect with our thought leaders at our booth and learn how we’re dedicated to helping credit unions of all sizes advance their decisioning and services. Our team is committed to being a trusted partner – providing solutions that enable you to further grow, protect and serve within your field of membership. Learn More