In this article:

There's nothing a credit repair service can legally do for you—even removing wrong information—that you can't do for yourself for little or no expense. And the cost of hiring such a company can be considerable, ranging from hundreds to thousands of dollars.

While it can be tempting to offload the work of fixing your credit to a credit repair company, it's important to know what they can and can't do—and to take steps on your own first before you consider shelling out cash to pay their fees.

What Is the Credit Repair Organizations Act?

Credit repair companies dispute negative information found on your credit reports. But in the past, some of these companies would overstate what they could do for consumers to drum up business.

The Credit Repair Organizations Act (CROA) is a federal law that became effective on April 1, 1997, in response to a number of consumers who had suffered from credit repair scams. In effect, the law ensures that credit repair service companies:

- Are prohibited from taking any payment from a consumer until they fully complete the services they promise.

- Are required to provide consumers with a written contract stating all the services to be provided as well as the terms and conditions of payment. Under the law, consumers have three days to withdraw from the contract.

- Are forbidden to ask or suggest that you mislead credit reporting companies about your credit accounts or alter your identity to change your credit history.

- Cannot knowingly make deceptive or false claims concerning the services they are capable of offering.

- Cannot ask you to sign anything that states that you are forfeiting your rights under the CROA. Any waiver that you sign cannot be enforced.

The CROA adds transparency and due diligence to the credit repair process, making it less likely that consumers will be taken advantage of. However, regulators have still found wrongdoing among credit repair companies.

The Consumer Financial Protection Bureau has sued several credit repair companies over the years for requesting prohibited upfront fees, misleading customers about their ability to fix credit and more.

Can You Pay to Have Your Credit Fixed?

If your credit file has information you feel is incorrect, credit repair companies may offer to dispute the information with the credit reporting agencies on your behalf. Credit repair companies typically charge a monthly fee for work performed in the previous month or a flat fee for each item they get removed from your reports. However, Experian does not charge consumers or require any special form to dispute information, so this is something you can do on your own at no cost.

If you're on a monthly subscription, the cost is typically around $75 per month but can vary by company. The same goes for paying a fee for each deletion, but that option typically runs $50 each or more.

That said, it's important to keep in mind that credit repair isn't a cure-all—and in many cases it crosses the line into unethical or even illegal measures by attempting to remove information that's been accurately reported to the credit bureaus. While these companies may try to dispute every piece of negative information on your reports, it's unlikely that information reported accurately by your lenders will be removed.

And again, credit repair companies can't do anything that you can't do on your own for free. As a result, it's a good idea to consider working to fix your credit first before you pay for a credit repair service to do it for you.

How to "Fix" Your Credit by Yourself

There is no quick fix for your credit. Information that is negative but accurate (such as missed payments, charge-offs or collection accounts) will remain on your credit report for seven to 10 years. However, there are steps you can take to start building a more positive credit history and improve your credit scores over time.

Check Your Credit Report

To get a better understanding of your credit picture and what lenders can see, check your credit report and learn more about how to read your Experian credit report. It's also a good idea to order your free credit score from Experian. With it, you'll receive a list of the risk factors that are most impacting your scores so you can make changes that will help your scores improve.

If you find information that is incorrect, you can file a dispute with the credit reporting agency on whose report you found it. You should also contact the lender that is reporting the incorrect information directly and ask them to correct their records.

Improve Your Payment History

Your payment history is the most important component of FICO® scoring models. Late and missed payments will reduce your credit scores, and bankruptcies and collections can cause significant damage. This negative information will remain on your credit report and impact your credit scores for seven to 10 years.

Your scores often take into account the size of your debt and the timing of your missed payments. The bigger your debt is, and the more recent your missed payments are, the worse your score will be, typically. Bringing accounts current and continuing to pay on time will almost always have a positive impact on your credit scores.

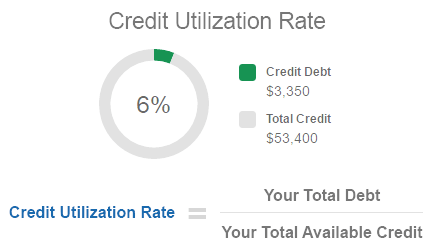

Know Your Credit Utilization Ratio

Credit scoring models usually take into account your credit utilization ratio, or rate, which is how much you owe compared with how much credit you have available.

Basically, it's the sum of all of your revolving debt (such as your credit card balances) divided by the total credit that is available to you (or the total of all your credit limits)—multiplied by 100 to get a percentage. For example, if you have $6,000 in credit card balances and $60,000 in total available credit across all of your credit card accounts, your utilization ratio is 10%.

High credit utilization can negatively impact your credit scores. Generally, it's a good idea to keep your credit utilization ratio below 30%, but there's no hard-and-fast rule—the lower it is, the better.

There are a few different ways you can reduce your credit utilization rate:

- Start paying down your account balances.

- Increase your total available credit by opening a new credit card account or requesting a credit limit increase on an existing card.

- Consolidate your credit card debt with a personal loan, which isn't included in your credit utilization rate calculation.

That said, while increasing your credit limit may seem like an appealing option, it can be a risky move. If increasing your credit limit tempts you to spend more, you could fall deeper into debt. Additionally, if you try to open a new credit card, a hard inquiry will appear on your credit report and could temporarily reduce your credit score by a few points.

Also, while consolidating your debt with a personal loan can drop your utilization rate to zero immediately, it can be tough to get approved for a loan with a reasonable interest rate if your credit score is in poor shape.

As such, paying down your balances on credit cards and other revolving credit accounts may be the best option to improve your credit utilization rate and, subsequently, your credit scores.

Consider How Many Credit Accounts You Have

Scoring models consider how much you owe and across how many different accounts. If you have debt across a large number of accounts, it may be beneficial to pay off some of the accounts, if you can.

Paying down credit card debt is the goal of many who've accrued debt in the past, but even after you pay the balance down to zero, consider keeping that account open. Not only can closing it hurt scores by eliminating that available credit and increasing your credit utilization ratio, but keeping paid off accounts open can also be a plus because they're aged accounts in good (paid-off) standing. And again, you may also consider debt consolidation.

Think About Your Credit History

Credit scoring models, like those created by FICO®, often factor in the age of your oldest account and the average age of all of your accounts, rewarding individuals with longer credit histories. Before you close a credit card account, think about your credit history. It can be beneficial to leave a credit card open even if you've paid it off and don't plan on using it anymore.

Of course, if keeping accounts open and having credit available could trigger additional spending and debt, you may choose to close the accounts after all. Like fingerprints, every person has a unique financial situation, and only you know all the ins and outs of yours. Make sure you carefully evaluate your situation to figure out the approach that works best for you.

Be Wary of New Credit

Opening several credit accounts in a short period of time can cause you to appear risky to lenders and, in turn, negatively impact your credit scores. Before you take out a loan or open a new credit card account, consider the effects it could have on your credit.

Note, however, that when you're buying a car or looking around for the best mortgage rates, your inquiries may be grouped together and counted as only one inquiry for the purpose of credit scoring. In many commonly used scoring models, recent inquiries have a greater effect than older inquiries, and they only appear on your credit report for 24 months.

How Long Does It Take to Rebuild Credit?

It's hard to say with certainty how long it takes to rebuild credit because each person's credit history is different. If you've had credit difficulties in the past, how long it will take to rebound depends in part on the severity of the negative information in your credit report and how long ago it occurred. While some actions can have an almost immediate effect—such as paying down credit card balances—others may take months to make a significant positive impact.

If you're disputing information in your credit report you believe is fraudulent or inaccurate, the investigation can take up to 30 days. If the credit reporting agency finds your dispute valid, the information will be removed from your credit report, and your score will reflect that change as soon as it's calculated again.

If you're making payments or reducing your credit card balances, don't worry if your credit report isn't updated right away. Creditors only report to Experian and other credit reporting agencies on a periodic basis, usually monthly. It can take up to 30 days or more for your account statuses to be updated, depending on when in the month your creditor or lender reports their updates.

It's critical that you check your credit score regularly to keep track of your progress and make sure the right information is being reported over time. As you build a positive credit history, over time, your credit scores will likely improve, and you'll have a better chance of qualifying for favorable credit terms when you need to borrow again.

How to Get Extra Help With Your Credit and Debt

If your debt is manageable, consider consolidating it via a personal loan or balance transfer credit card.

In some cases, debt consolidation loans can provide lower interest rates and reduced monthly payments, as long as you qualify and stick to the program terms. With a balance transfer card, you can typically get an introductory 0% APR promotion, during which you can pay down the balance interest-free. Just be mindful not to continue charging on the original card once the balance is transferred.

If your debt feels overwhelming and your credit isn't good enough to get a balance transfer card or a low-interest personal loan, it may be valuable to seek out the services of a reputable credit counseling agency. Many are nonprofit, and you can typically get a consultation with personalized advice for your situation at no cost.

You can review more information on selecting the right reputable credit counselor for you from the National Foundation for Credit Counseling.

Credit counselors can also help you develop a debt management plan (DMP) with unsecured debt like credit cards. With this arrangement, you'll make your monthly debt payments to the credit counseling agency, and it will disburse the funds to your creditors. The agency may also be able to negotiate lower monthly payments and interest rates.

If the credit counselor negotiates settled amounts that mean you pay less to your creditors than was originally owed, your credit score could take a hit. In addition, your credit report may denote that accounts are paid through a DMP and were not paid as originally agreed, which may be viewed negatively by lenders. However, using a DMP may not negatively impact your credit history when you continue to make payments on time as agreed under the new terms.

Keep Track of Your Credit After You've Reached Your Goal

Once you've done the work to rebuild your credit history, you may be tempted to move on and focus on something else. While you likely won't need to focus as much on your credit score as you used to, it's still a good idea to keep an eye on it.

Monitoring your credit will help you spot any potential issues that could cause your credit score to drop again. It'll also give you a heads up if someone commits identity theft, so you can address it before it gets out of hand.

With Experian's free credit monitoring tool, you'll get access to your FICO® Score☉ powered by Experian data and also an updated copy of your Experian credit report. You'll also get real-time alerts about new inquiries and accounts, suspicious activity and changes to your personal information.

Learn More About Repairing Your Credit

- How Long Does It Take to Repair Your Credit?

The length of time it takes to rebuild your credit history depends on how serious your credit issues were and how your credit history was affected. - How Does Credit Repair Work?

Credit repair companies try to get information removed from your credit report—for a price. You can do anything they can, for free. - What Is a 609 Dispute Letter?

A 609 Dispute Letter claims to be a credit repair secret that you can purchase. Learn how you can dispute errors yourself and for free. - Can Credit Repair Companies Remove Late Payments?

Credit repair companies may promise to remove late payments—but they have no more power than you do when it comes to disputing credit report information. - How Much Does Credit Repair Cost?

Credit repair companies may charge hundreds or even thousands of dollars to try to remove items from your credit report. Here’s why it’s not worth the cost. - Can Previously Deleted Items Reappear on My Credit Reports?

Items previously deleted from your credit report could reappear in certain circumstances. Here’s why—and what you can do about it. - How to Dispute Credit Report Information

Here’s how to request corrections to information in your credit reports—a process known as a dispute.