What Is a Credit Utilization Rate?

Quick Answer

Your credit utilization rate is the percentage of available credit that you’re using on your credit cards and other lines of credit. It’s based on the balances that appear in your credit report. In general, a lower utilization rate is best.

Your credit utilization ratio, sometimes called your credit utilization rate, is the amount of revolving credit you're using divided by the total amount of revolving credit you have available. It's expressed as a percentage, and it can be an important factor in your credit scores.

In general, lower utilization rates can improve your credit scores, which can in turn make it easier to secure additional credit with favorable terms. Learning what impacts your utilization rate and how to maintain a low utilization rate is an important part of managing your credit and finances.

What Factors Into Your Credit Utilization Ratio?

Credit utilization is also sometimes called revolving credit utilization because only your revolving credit accounts are included in the calculations. The specifics depend on the type of credit score, but types of revolving credit accounts include:

- Credit cards

- Credit cards you're named as an authorized user on

- Personal lines of credit

- Home equity lines of credit (HELOC)

- Closed revolving accounts with outstanding balances

The credit utilization calculation depends on the balances and credit limits from your credit report, which may be different from your current credit limits and balances.

How to Calculate Your Credit Utilization

It's important to understand how to calculate utilization rates on your own. It's also fairly straightforward.

- Find your revolving account balances and credit limits from your credit report. When considering your credit utilization, credit scoring models use the account balances and credit limits listed in your credit reports. You should do the same.

- Add up your revolving accounts' balances and credit limits. You'll use these two sums to find your overall utilization rate.

- Divide the total balance by the total credit limit and then multiply by 100 to get a percentage. The calculation only involves simple addition, division and multiplication—that's all the math involved.

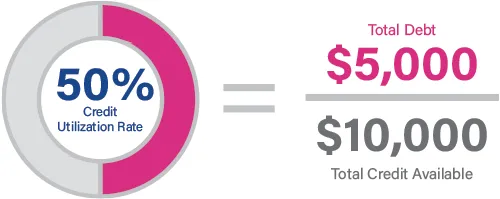

Example: Say you have two credit cards, and each one has a $5,000 credit limit. One card has a $5,000 balance and the other card has a $0 balance. Since your total available credit is $10,000 and your total balance is $5,000, your overall utilization rate is 50%.

Individual Account vs. Total Credit Utilization

Continuing with the above example, you can use the same calculation (balance divided by credit limit times 100) to find the per-card utilization. In the example above, one card has 0% utilization, and the other card has 100% utilization.

Credit scoring models may consider the highest utilization rate on a revolving account in addition to your overall utilization rate. Having a card with a very high utilization rate, such as 100%, can hurt your credit score even if your overall utilization is relatively low.

What Is a Good Credit Utilization Rate?

A good utilization rate is a low utilization rate, ideally in the single digits. The average overall credit utilization in the U.S. was 29% in the third quarter (Q3) of 2024, according to Experian data. However, when you look at the average overall credit utilization broken down by credit score group, it's clear that lower is better. Below are average credit utilization ratios by FICO® ScoreΘ.

| Score Range | Average Credit Card Utilization Ratio |

|---|---|

| Poor (300 - 579) | 80.7% |

| Fair (580 - 669) | 61.4% |

| Good (670 - 739) | 38.6% |

| Very good (740 - 799) | 15.2% |

| Exceptional (800 - 850) | 7.1% |

Source: Experian data from Q3 2024

While there's no specific point when your utilization rate goes from good to bad, 30% is the point at which it starts to have a more pronounced negative effect on your credit score. As the data above illustrates, those with the highest scores tend to have credit utilization in the low single digits.

Counterintuitively, however, a utilization rate of 0% is actually worse than 1%. That's because credit scoring models need some usage to go off of when calculating your score, and 0% utilization doesn't tell them much about your credit habits. A low utilization rate could indicate you're using your card and repaying your balances responsibly.

How Does Credit Utilization Affect Your Credit Scores?

Revolving credit utilization is an important scoring factor that could affect around 20% to 30% of your credit score depending on the scoring model. However, utilization rates can impact your credit scores in several ways.

- Overall and per-account utilization can affect credit scores. Your overall utilization rate and the utilization rate of the account with the highest utilization can affect your credit scores.

- Only the most recently reported numbers affect most credit scores. Many credit scoring models don't look beyond the most recently reported balances and limits in your credit reports. As a result, you might be able to quickly improve those credit scores by lowering your utilization rate.

- Newer scoring models consider trends in utilization rates. Unlike previous credit scoring models, the latest VantageScore® 4.0 and FICO 10 T models consider trended data. This can include your average utilization ratio and credit card balances over time.

The exact impact of a changing utilization rate depends on your current credit score, the type of credit score and what else is in your credit report. But, as mentioned above, a lower utilization rate is generally best for your credit scores.

How to Lower Your Credit Utilization Rates

You can lower your overall utilization rate and your individual account utilization rates by decreasing the balances and increasing the credit limits on the revolving accounts in your credit reports.

One option is to use cash or debit cards instead of credit cards for most purchases. However, assuming you want to use credit cards to receive their protections, rewards and benefits—as well as the credit benefits when used responsibly—here are a few additional ways to lower your credit utilization rates.

- Pay down credit card balances early. Credit card issuers generally report your account's balance to the credit bureaus at the end of each statement period. They send you the statement at the same time, and your bill is due several weeks later. Because of this timing, you may have a high utilization rate even if you pay your bill in full. But you may be able to lower the reported balance and resulting utilization rate by making credit card payments before the end of each statement period.

- Ask your card issuers to raise your limits. You may want to request a higher credit limit if you've had the card for a while, made your payments on time and won't run up the balance. Additionally, consider making a request after your income increases, your credit score improves or you pay off other debts. Credit limit increase requests sometimes lead to a hard inquiry, however, which might lower your credit scores a little temporarily.

- Keep your reported income updated. Credit card issuers might increase your card's credit limit when your income rises, but they won't know unless you update your annual income in your online account. You also might be able to report your household income if you started sharing finances with someone since opening your card.

- Use an installment loan to consolidate revolving debt. You might be able to use a personal loan or home equity loan to consolidate revolving debt, such as credit card and HELOC debts. In addition to lowering your utilization rates, you might benefit from a fixed interest rate and set repayment period.

- Open new lines of credit. Getting a new credit card or line of credit increases your overall available credit. Many credit cards also offer intro bonuses and other perks. However, you should avoid opening new accounts solely to increase your available credit.

- Don't close your credit cards. You may want to close credit cards that have an annual fee or if you tend to overspend. However, keeping credit cards open can help you maintain a lower utilization rate because their credit limits add to your overall available credit.

If you want to maintain a low credit utilization rate without timing your credit card payments, try to estimate how much you spend on credit cards each month. Multiply this by 10 and use that as a target for the available credit you want to have across your revolving accounts. You'll then be able to maintain your average spending while keeping your utilization rate around 10%.

Frequently Asked Questions

Check and Track Your Credit Utilization

You can access your Experian credit report for free. You can use it to calculate your current utilization rate, track your overall utilization rate over time and look at each revolving account in your credit report to see the per-account utilization. You'll also receive FICO® Score monitoring, which can alert you to significant changes in your credit.

Instantly raise your FICO® Score for free

Use Experian Boost® to get credit for the bills you already pay like utilities, mobile phone, video streaming services and now rent.

No credit card required

About the author

Louis DeNicola

Louis DeNicola is freelance personal finance and credit writer who works with Fortune 500 financial services firms, FinTech startups, and non-profits to teach people about money and credit. His clients include BlueVine, Discover, LendingTree, Money Management International, U.S News and Wirecutter.

Read more from Louis