How to File an Auto Insurance Claim in 5 Steps

Quick Answer

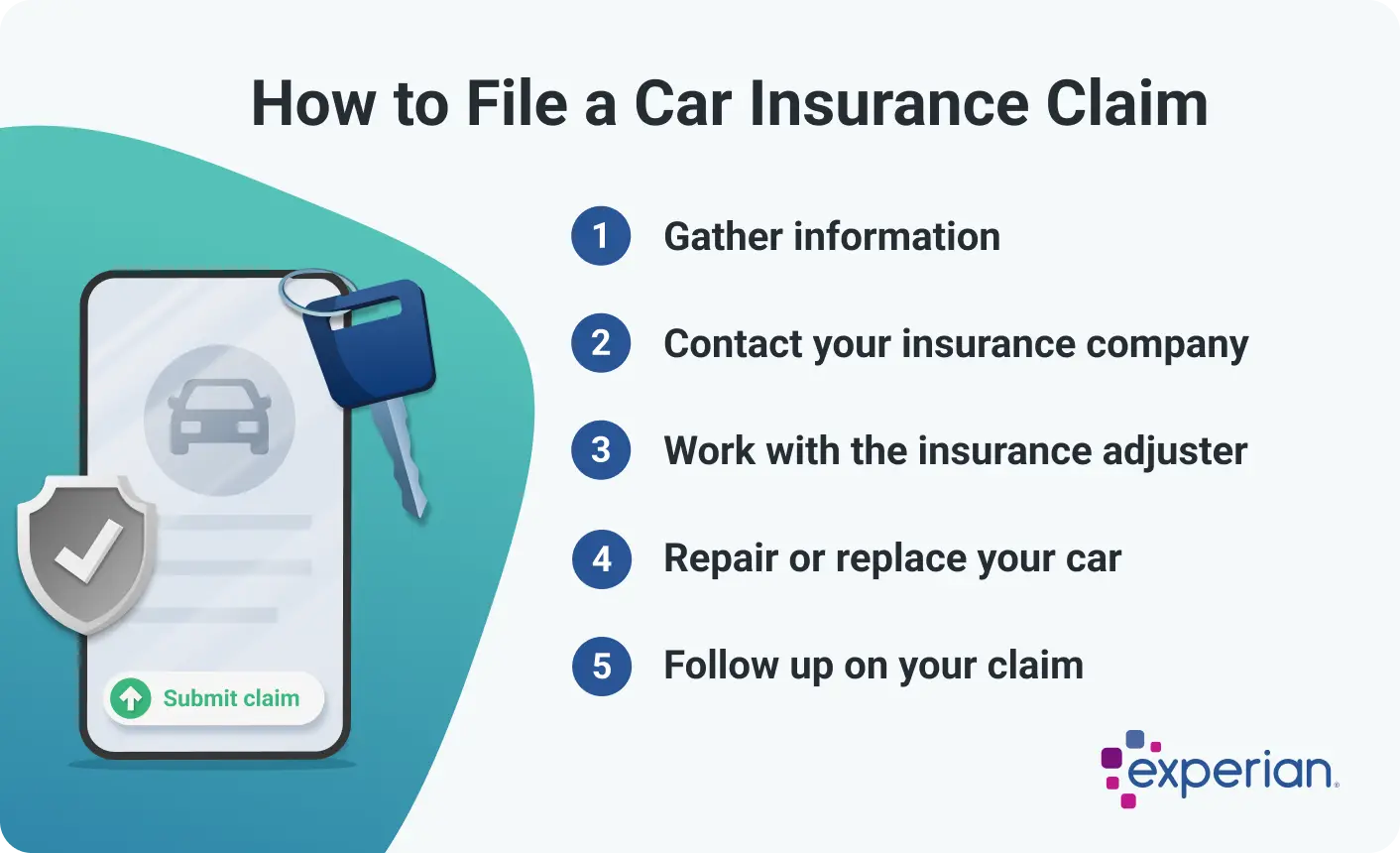

You can file an insurance claim by gathering information about the incident, contacting your insurer and working with the adjuster to repair or replace your car.

Getting in a car accident can turn your life upside down, and the road back to normalcy can be somewhat long. As a result, it's important to start the car insurance claims process quickly to ensure a smooth and prompt outcome.

To help you prepare for the experience, here's what you need to know about car insurance claims and the steps to file one.

How to File an Insurance Claim

It's crucial that you file an insurance claim as quickly as possible after a covered event. Here are some steps you can take to ensure a smooth process and avoid delays.

1. Gather Information

If you're in a collision, it's important to gather all of the information and documents that you need at the scene of the accident. Depending on the situation, that may include:

- Location, date and time of the accident

- Your policy number

- The other driver's name, phone number, insurance information and vehicle details

- Photos of the damage to your vehicle and any other vehicle or property involved

- Copy of the police report

If you've already incurred expenses, such as towing charges, make a copy of your receipts and submit them for reimbursement.

2. Contact Your Insurance Company

It generally makes sense to file a claim if you've been involved in an accident or your vehicle has sustained significant damage in a non-collision event. Some states require you to file a claim even if you weren't at fault.

However, if the cost of repairing the damage is less than your deductible, it could make sense to handle the repairs on your own.

Depending on your provider, you may be able to file a claim online, over the phone, via your insurer's mobile app or in person with an agent.

Provide as many details about the event as possible to give your insurer a full picture of what happened. The agent will tell you how to provide the documentation you've collected and give you some information about the next steps in the process. It's important to be truthful throughout the process—submitting a fraudulent claim can result in claim denial, fines, restitution or even jail time.

Learn more: What to Do After an Accident

3. Work With the Insurance Adjuster

After you submit your claim, an adjuster will be assigned to investigate. Here are some of the steps they'll take:

- Arrange an inspection of the vehicle to evaluate the damage

- Get an estimate of the cost to repair or replace the vehicle

- Analyze the police report and interview witnesses

- Help you get set up with a rental car

The adjuster will typically contact you within a few days to discuss the process and obtain additional information and documentation from you. Be sure to respond quickly to avoid potential delays.

4. Repair or Replace Your Car

If the damage isn't enough to merit totaling the vehicle, you have the right to choose the repair shop—though it can be convenient to simply go with the one your insurance provider recommends.

The repair shop will appraise the damage and submit it to your insurer for approval. Once approved, it can start on repairs. Depending on your insurer, there are two ways they may handle payment:

- Direct payment: In this case, the insurer may pay the repair shop directly, minus your deductible. You'll then pay the repair shop for the amount of your deductible.

- Reimbursement: With this option, you'll pay the repair shop and request reimbursement from the insurance company, which will account for your deductible.

If the damage is so severe that the cost to repair it exceeds the vehicle's value, the adjuster will declare the vehicle totaled, and the insurer will cut you or your lender a check based on the vehicle's value minus your deductible.

You can use whatever funds are disbursed to you to replace your car with a new one. However, if the payout is less than your loan amount, you'll need to repay the remaining balance out of pocket unless you have gap insurance.

Learn more: Total Loss Settlement Process: How Long Does It Take to Get a Check?

5. Follow Up on Your Claim

Throughout the claims process, it's important to stay on top of your insurance company and the repair shop to keep things moving.

As things kick off, ask about the timeline for repairs and stay in contact with the insurance adjuster and the repair shop to get regular updates. In some cases, the rental coverage may run out before the repairs are completed. In this case, reach out to the adjuster to discuss an extension.

If you paid a deductible but weren't at fault in the accident, you'll also want to follow up with your insurer about getting reimbursed from the other driver's insurance provider. This process is called deductible recovery.

If you were at fault in the accident, your insurance policy may also need to cover bodily injuries, damage to their vehicle and other damages. If you have insufficient coverage, however, the other driver's insurer may choose to file a civil lawsuit against you for damages.

Stop overpaying for insurance

Answer some questions about your current plan and get matched to personalized quotes.

We’ll show you offers from our top insurance carriers and help you shop for better rates in the future.

From switching your policy to canceling and requesting a partial refund on your old plan, we help you do it all.

Frequently Asked Questions

The Bottom Line

Filing an auto insurance claim requires some legwork upfront, but once you've provided all of the details and documentation, the adjuster will investigate and keep you updated. Be patient with the process, but don't be afraid to reach out if it's taking longer than promised.

If you've had a bad claims experience with your current insurance provider or it's been a while since you've shopped around for coverage, Experian's comparison tool can provide you with car insurance quotes from several insurance companies, making it easy to compare your options all in one place to ensure you're getting the best deal.

Don’t overpay for auto insurance

If you’re looking for ways to cut back on monthly costs, it could be a good idea to see if you can save on your auto insurance.

Find savingsAbout the author

Ben Luthi

Ben Luthi has worked in financial planning, banking and auto finance, and writes about all aspects of money. His work has appeared in Time, Success, USA Today, Credit Karma, NerdWallet, Wirecutter and more.

Read more from Ben