What Is a Bank Statement Loan?

Quick Answer

A bank statement loan is a type of mortgage designed for those who can’t provide mortgage lenders with traditional income documents like W-2s, pay stubs or tax returns. They’re often best for self-employed individuals and business owners.

A bank statement loan is a type of mortgage that self-employed individuals and business owners can qualify for based on their cash flow. Typically, a mortgage lender will want to verify your income via tax returns or W-2s, which borrowers who aren't traditional employees won't be able to provide.

Bank statement loans come with risks. They're not considered qualified mortgages according to the Consumer Financial Protection Bureau (CFPB). That means lenders aren't required to meet certain guidelines when determining whether you're able to repay the loan, which could put you at risk of not being able to afford your payments.

Here's what you should know before choosing a bank statement loan.

What Is a Bank Statement Loan?

A bank statement loan is a type of mortgage designed for those who can't provide mortgage lenders with traditional income documents such as W-2s, pay stubs or tax returns. As a result, bank statement loans are often best for self-employed borrowers and business owners.

They're not regulated in the same way that government-backed loans such as Federal Housing Administration (FHA), Veterans Affairs (VA) or U.S. Department of Agriculture (USDA) loans are. Bank statement loans are non-qualified mortgages (non-QM), meaning they don't meet standard rules set by the CFPB. They may include features such as negative amortization (when your principal increases throughout the loan term), 40-year repayment terms and high upfront fees.

Tip: Non-QM lenders aren't required to make as strong an effort to verify your income, assets and debts, which impact your ability to repay the loan. This could lead to a mortgage that is difficult to afford, increasing the chances of foreclosure.

How Does a Bank Statement Loan Work?

To get a bank statement loan, you'll provide the lender with personal or business bank statements for the previous one to two years. You may also need to make a larger-than-usual down payment, show that you have liquid assets you can access fast and have a certain number of years of self-employment behind you.

The lender will also look at your credit score and debt-to-income ratio (DTI). Lenders may require you to have a credit score of at least 620 or 700 and a DTI of 50% or less (meaning your debt payments equal no more than 50% of your gross monthly income). Based on the information you provide, the lender will determine whether you qualify and your loan amount.

Learn more: How to Get a Mortgage When You're Self-Employed

Bank Statement Loans vs. Conventional Loans

Bank statement loans have some significant differences from conventional loans. Below are the most important to keep in mind.

| Bank Statement Loans | Conventional Loans | |

|---|---|---|

| Income verification | Lenders do not need to verify your income, assets or current debts according to the CFPB's "ability-to-repay" rule | Lenders must verify your income, assets and current debts according to the CFPB's "ability-to-repay" rule |

| Minimum credit score | Depends on the lender; often, 620 or 700 | 620 |

| Down payment | Depends on the lender; often, 10% minimum. Private mortgage insurance (PMI) is required with a down payment of less than 20%. | Typically 3% minimum. Private mortgage insurance (PMI) is required with a down payment of less than 20%. |

| Interest rates | Typically higher than conventional loans due to higher risk for lender | Depends on credit score, loan amount, down payment and other factors |

| Loan terms | Up to 40 years | Up to 30 years |

Pros and Cons of Bank Statement Loans

Bank statement loans come with both pros and cons, and how heavily each of these weigh on your decision will depend on your personal circumstances. Review the pros and cons below before moving forward.

Pros

-

Potentially strong option for the self-employed: Bank statement loans may make home ownership possible for borrowers who otherwise wouldn't qualify due to lack of tax returns or W-2s.

-

More flexibility: Since bank statement loans are non-QM loans, you may qualify without having a certain amount of liquid assets or income.

-

Longer terms: Bank statement loans offer terms of up to 40 years, which may lead to lower monthly payments than you'd get with a 30-year conventional mortgage.

Cons

-

Larger down payment required: You won't have the option to make a down payment of 3% as you would with a conventional loan. Expect to pay at least 10% down with a bank statement loan.

-

Higher interest rates: Since borrowers who aren't traditionally employed are viewed as a higher risk to the lender, you'll likely pay a higher interest rate to compensate. Longer loan terms also mean paying more in interest over the life of the loan.

-

Higher risk of falling behind on payments: The downside of not having to meet strict ability-to-repay requirements is that the lender may not adequately assess whether you can truly afford the loan.

Learn more: What Factors Do Mortgage Lenders Consider?

Should You Get a Bank Statement Loan?

Non-QM loans like bank statement loans aren't right for everyone. While the requirements are more flexible than those of conventional loans, you still need to show a history of self-employment and sufficient income. You'll typically also need a good credit score. A bank statement loan can be beneficial for the following types of borrowers:

- Entrepreneurs and business owners: Those who have started their own businesses and have at least one to two years' worth of deposits to a business account can qualify.

- Self-employed individuals: If you're an independent contractor or freelancer, you can also demonstrate eligibility with at least one year of self-employment history.

- Real estate investors: While investors don't have regular income from employment, deposits to a personal or business account over the lender's minimum timeframe can meet the requirements for a bank statement loan.

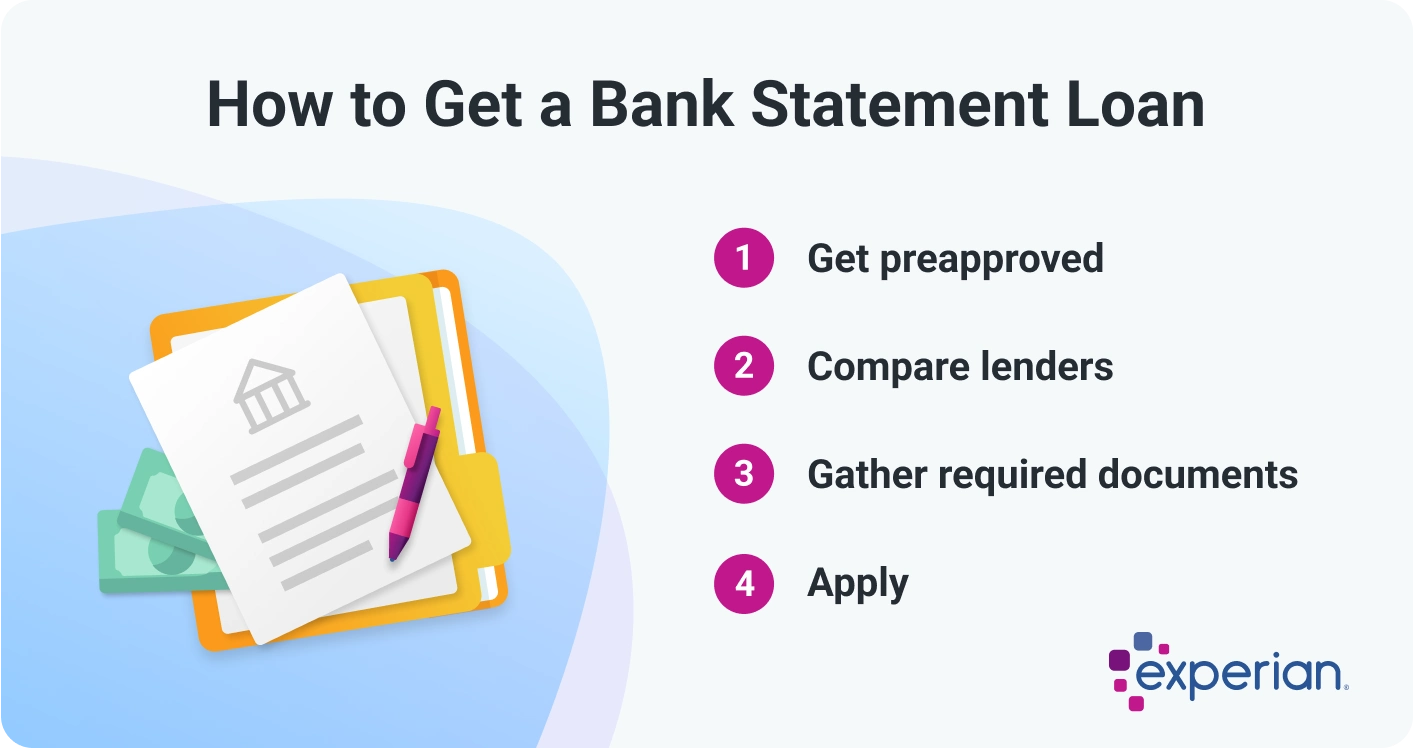

How to Get a Bank Statement Loan

The process for getting a bank statement loan will vary by lender, but includes a few steps you can expect to encounter. They include:

1. Get Preapproved

First, fill out an application for mortgage preapproval with each lender you're considering working with. You'll see if you qualify and what terms you may get. Preapproval is preliminary; your final interest rate, fees and other terms will be confirmed later in the application process.

2. Compare Lenders

Compare the terms you've been offered, including the interest rate, fees, repayment term, whether the loan comes with a balloon payment and other features. Calculate your monthly payment and determine whether it fits within your budget, making sure you can afford other costs of homeownership like repairs, insurance and property taxes.

Learn more: How to Shop for a Mortgage

3. Gather Required Documents

Once you've found a house to make an offer on, gather the documents required by your lender to verify your income, assets, debt and identity. That will give the lender the information they need to finalize your bank statement loan.

4. Apply

Submit your final mortgage application, and be ready to provide additional documentation or information if the lender requests it to approve your loan. The underwriting process can take up to two months, and in that time, you'll get a property inspection and secure homeowners insurance for the property you're buying. At closing, you'll pay an appraisal fee, origination fees and more, in addition to handing over your down payment.

Alternatives to a Bank Statement Loan

If you don't qualify for a bank statement loan, there are a few other options to look into:

- Conventional loans: You'll need income verifiable by tax returns or W-2s for a conventional loan, but you may be able to qualify for one with a lower down payment than a bank statement loan requires.

- FHA loans: If you have verifiable income from employment but a lower credit score, look into FHA loans, which have a minimum credit score of just 500.

- VA loans: Current and former service members may be candidates for VA loans, which have no down payment requirement and income requirements that vary by lender.

- Portfolio loans: This type of mortgage is one that the lender maintains as part of its own investment portfolio. They have more flexible eligibility requirements but may also come with higher interest rates than conventional loans.

Frequently Asked Questions

The Bottom Line

Bank statement loans are a worthwhile option for borrowers who are self-employed or who own businesses and feel locked out of traditional mortgages. But particularly due to their limited regulations, bank statement loans can end up being risky and costly for many. Look at your loan offers carefully and consider other types of loans, if you qualify for them, before choosing a bank statement loan.

Curious about your mortgage options?

Explore personalized solutions from multiple lenders and make informed decisions about your home financing. Leverage expert advice to see if you can save thousands of dollars.

Learn moreAbout the author

Brianna McGurran

Brianna McGurran is a freelance journalist and writing teacher based in Brooklyn, New York. Most recently, she was a staff writer and spokesperson at the personal finance website NerdWallet, where she wrote "Ask Brianna," a financial advice column syndicated by the Associated Press.

Read more from Brianna