Women and Credit 2020: How History Shaped Today’s Credit Landscape

If you're a woman with credit cards or loans in your name, it might be hard to believe that just 46 years ago, that may not have been possible.

Before the Equal Credit Opportunity Act of 1974, lenders could legally require women to have male cosigners on loans or make larger down payments on homes than men with similar credit profiles. While women can still face challenges when seeking credit today, they've come a long way in the decades since access to credit wasn't anywhere near equitable.

To commemorate International Women's Day on March 8, Experian analyzed consumer credit and debt data from Q2 2019 to understand the financial picture for women today, and how it's changed over time. We found that despite gaining full, independent access to credit relatively recently with the Equal Credit Opportunity Act, women's average FICO® ScoresΘ today are nearly identical to those of men. They also carry less debt across all categories except for student loans.

Here's what you need to know about women and money before the 1970s—and what has happened since.

Women's Credit and Finances Before the Equal Credit Opportunity Act

Women's financial subservience to men was the norm for centuries. Married women in the early U.S. were not considered legal entities independent of their husbands thanks to a principle known as coverture, a holdover from British law.

That meant husbands could take control of real estate wives brought into the marriage, and they took full ownership of all other types of property she held. (Single women had the same legal right to property as men, but the number of unmarried women in the 18th and 19th centuries was very low compared with today.) Married women also could not manage their own income, make contracts or create wills.

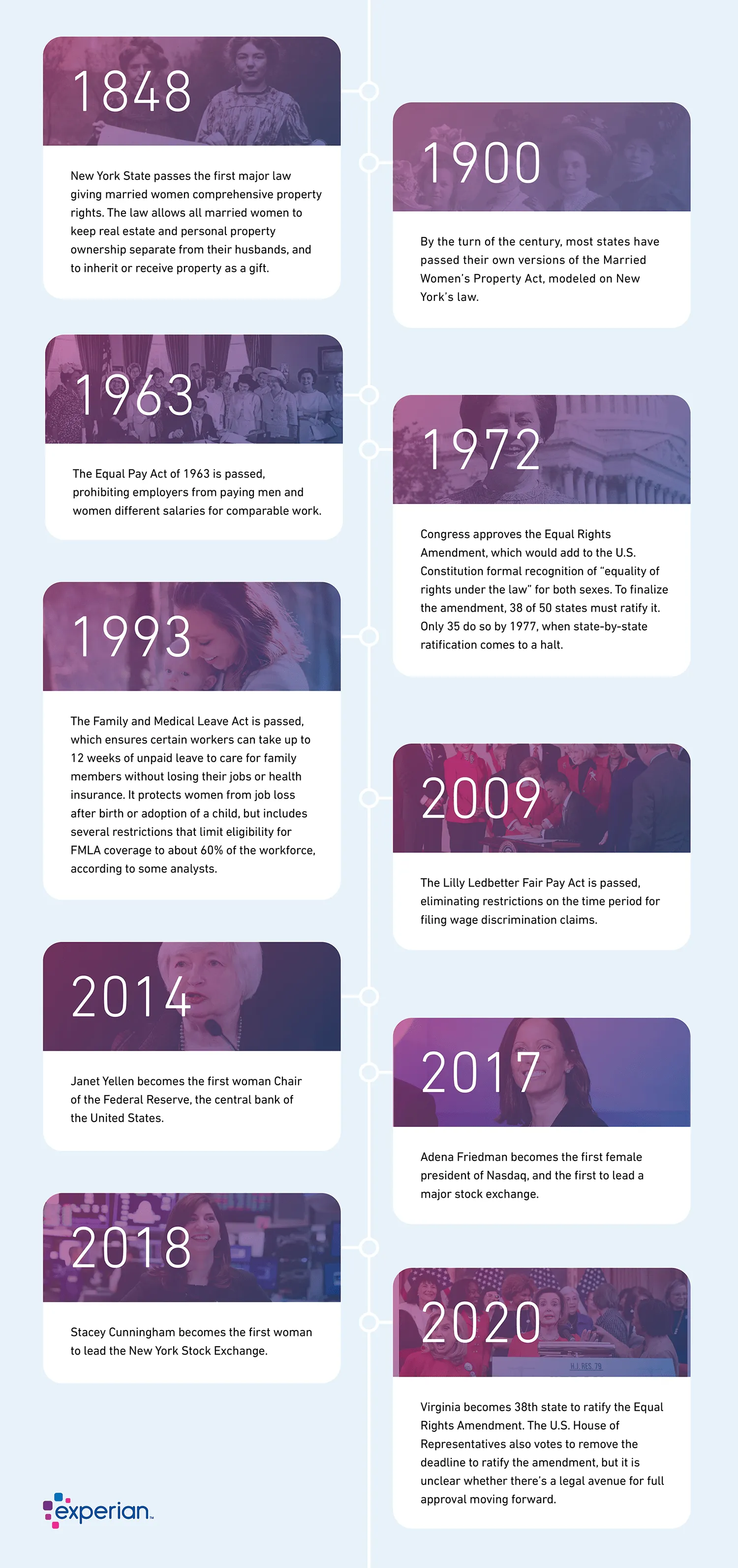

Starting in the mid-1800s, states began enacting laws chipping away at these restrictions for married women. In 1848, New York became the first to pass an extensive law allowing married women to own property, but it took decades for all American married women to gain full legal control of their property, savings and earnings. Well into the 20th century, they continued to face financial discrimination.

Married women seeking mortgages with their husbands encountered lenders who wouldn't include their full incomes in the application, and many lenders and credit card issuers required a man to cosign a woman's credit application. One argument was that a working woman's income was more likely to drop in the future if they took time away from the workforce while they cared for family members. But the process amounted to overt gender-based discrimination.

Women's Credit and Finances Today

Then the Equal Credit Opportunity Act of 1974 was signed into law, and lenders were banned from discriminating against consumers based on their sex or marital status.

Lenders could no longer require a male cosigner or otherwise treat women differently when they applied for credit, and women could not be charged higher interest rates or be required to make larger down payments than a man. But while there are consequences when the law is broken, there are still ways gender disparities and biases continue to affect women seeking credit.

For instance, because creditors use income as a primary qualification in lending decisions, women who earn less than men—or who earn no income as family caregivers—may have a harder time getting credit, or getting the most favorable terms on loans and credit cards.

Women earning little or no income can join a family member's credit account as an authorized user to help them build credit. But because authorized users are not responsible for making payments, some lenders may not weigh that account history the same as they would an account on which the consumer is a primary account holder—and that may affect the credit limits or interest rates they'd receive when applying for credit in their name.

Similarly, women who are widowed or divorced and who didn't have independent credit accounts during marriage can also face difficulties getting loans or credit cards on their own.

How Women's Credit and Finances Compare to Men's

Women's and men's average FICO® Scores are nearly identical: 705 for men and 704 for women, according to Experian data from the second quarter (Q2) of 2019. Both groups' scores have increased about 10 points since Q2 2015.

Men carry more debt than women across nearly all categories, but the differences aren't always significant. For instance, men have just $125 more in credit card debt than women on average, as of Q2 2019. But women have more open credit card accounts than men do: 4.5 compared with 3.6.

Personal loans reflect the largest statistical spread between debt balances by gender. Men have 20% more personal loan debt than women: $17,716 compared with $14,780. They also have 16.3% more auto loan debt and 9.7% more mortgage debt.

When adding up all types of debt we analyzed—credit cards, student loans, auto loans, personal loans, home equity lines of credit and mortgages—men carry $18,533, or 21.7%, more debt than women.

One outlier is student loans: On average, women have $36,131 in student loan debt, which is $943, or 2.7%, more than what's carried by men.

| Type of Debt | Women | Men |

|---|---|---|

| Credit card balance | $6,232 | $6,357 |

| Student loan balance | $36,131 | $35,188 |

| Auto loan balance | $17,747 | $20,645 |

| Personal loan balance | $14,780 | $17,716 |

| Home equity line of credit (HELOC) balance | $42,746 | $47,017 |

| Mortgage balance | $192,368 | $211,034 |

| Total balance | $85,169 | $103,702 |

Source: Experian Q2 2019 data

Men's and women's attitudes toward debt differ, according to a 2018 American University analysis of survey data among unmarried consumers. Women were more likely to say that taking on debt is acceptable during periods of financial hardship, such as when they're between jobs. Men were more likely to say it's acceptable to incur debt to buy luxury items. That may account for some of the difference in debt loads.

So, too, might the fact that women's earnings generally lag behind men's. While women's FICO® Scores have reached parity with men, their incomes haven't. Even with additional education, the income difference in many occupations still exists.

Overall, women without bachelor's degrees earn 78 cents for every dollar men earn, according to the U.S. Census Bureau. While bachelor's degree holders earn nearly double the salaries of those without, the gender wage gap is even greater among the college-educated. Women with college degrees earn 74 cents for every dollar men earn, according to the U.S. Census Bureau.

How to Build and Keep Good Credit

Both women and men can benefit from a deep knowledge of their credit scores. Here's how to keep your score as strong as possible:

- First, get credit in your name. If you can't qualify for a credit card or loan on your own, start off as an authorized user, then apply for your own account when your score is high enough to qualify. Or start by getting a secured credit card in your name. Some secured credit card issuers may upgrade you automatically to a traditional, unsecured card after a period of on-time payments and responsible usage.

- Regularly check your credit report. The information in it determines your credit score. (You're entitled to one free credit report per week from each of the three major credit bureaus at AnnualCreditReport.com.) Double-check that the information in your credit report is accurate and up to date. If you notice any discrepancies, you can dispute the information with the credit bureaus and also contact the lender reporting the information directly so they can update their records.

- Make it a priority to pay all bills on time. The most important factor in your credit score is payment history, and even a single late or skipped credit card or student loan bill can negatively affect it. Set alerts or reminders, or even better, set up autopay so your bills are paid directly from your checking account each month.

- Limit credit utilization. After payment history, credit utilization is the next-most important contributor to your credit score. Your credit utilization ratio is the amount of revolving credit you use compared with the limit your creditors give you, and it's best to keep it under 30%, according to experts—but the lower, the better.

That means using credit cards only for purchases you can afford to pay off each month. That will help keep your accounts active and show lenders that you can successfully manage credit. - Track your credit score. There are lots of ways to monitor your credit score: Your credit card company, lender or bank might offer free access to it, or you can view your FICO® Score through Experian's free service. You'll be able to see which factors are negatively affecting it so you can address them.

Moving Forward

While women benefit from regulations banning discrimination in lending, gender disparities still exist in the financial industry. Arm yourself with mastery of credit and how it's developed so you can protect yourself, stay alert to potential bias and take advantage of hard-won victories on the road to women's full financial independence.

Through the Years

Methodology: The analysis results provided are based on an Experian-created statistically relevant aggregate sampling of our consumer credit database that may include use of the FICO® Score 8 version. Different sampling parameters may generate different findings compared with other similar analysis. Analyzed credit data did not contain personal identification information. Metro areas group counties and cities into specific geographic areas for population censuses and compilations of related statistical data.

FICO® is a registered trademark of Fair Isaac Corporation in the U.S. and other countries.

What’s on your credit report?

Stay up to date with your latest credit information—and get your FICO® Score for free.

Get your free reportNo credit card required

About the author

Brianna McGurran

Brianna McGurran is a freelance journalist and writing teacher based in Brooklyn, New York. Most recently, she was a staff writer and spokesperson at the personal finance website NerdWallet, where she wrote "Ask Brianna," a financial advice column syndicated by the Associated Press.

Read more from Brianna